CHICAGO, IL--(Marketwire - June 22, 2010) - A new study developed by TransUnion finds that consumers with multiple account relationships with the same lender dramatically outperform consumers who maintain only one relationship with that lender.

"Although the conventional wisdom has acknowledged the benefits of loyalty for years, this study is a major step in quantifying that benefit and giving lenders the ability to incorporate that insight into lending strategy," said Ezra Becker, the author of the study and director of consulting and strategy in TransUnion's financial services business unit. "As the economy recovers and lenders return to more active customer acquisition, our study gives clear, timely evidence of the value in lenders establishing multiple relationships with the same borrower. Our results go a long way toward easing the concerns some in the industry have voiced through the recession regarding customer concentration risk."

The TransUnion study looked at data from six super-regional financial institutions -- three banks and three credit unions -- each December from 2007 to 2009. Approximately 19 million consumers were included in each snapshot, and more than 400 million tradelines were evaluated in each time period. The study examined the correlation between the number of consumer accounts that were 30 days or more delinquent and the number of accounts the borrower held with the target lender.

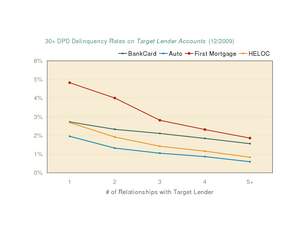

In virtually all cases, delinquency levels on first mortgages, home equity lines of credit (HELOCs), credit cards and auto loans decreased considerably as the total number of relationships the borrower had with a lender increased.

The most dramatic shifts in delinquency were seen with first mortgages. In December of 2009, the study found that borrowers with just one relationship with a given lender had a 30-day or worse delinquency rate of 4.8 percent on the mortgage with that lender. However, this delinquency level dropped 17 percent to 4.0 percent if the borrower had two relationships with the lender. That rate dropped further to 2.8 percent with three relationships, 2.3 percent with four associations, and down to 1.9 percent with five or more relationships.

On the credit card front, 30-day or worse incident delinquency declined from 2.7 percent for borrowers with one lender relationship to 2.1 percent for borrowers with three relationships, down to 1.6 percent for customers with five or more associations with the lender.

Thirty-day or worse auto loan delinquencies dropped by nearly 50 percent between borrowers with one relationship and those with three relationships, from 2.0 percent to 1.0 percent, and down further to 0.6 percent for those with five or more relationships with the lender.

"There is a clear, consistent and quantifiable increase in customer value associated with loyalty. With the constraints of the recently passed Credit CARD Act forcing lenders to find innovative ways to generate revenue, and the anticipated fierce competition for growth once the credit markets open up, it behooves financial institutions to understand how their marketing acquisition efforts and product offers to current customers impact delinquencies and write-offs throughout their operations," continued Becker. "From a consumer standpoint, this phenomenon is important because of the possible benefits that might be obtained by demonstrating loyalty to a particular financial institution. In short, credit relationships work best when both the lender and the borrower view the deal as a partnership."

An important finding of the study was that the "Loyalty Effect" was seen across the spectrum of credit risk. One might assume that customers with multiple relationships with a given lender generally have higher credit scores than customers with fewer relationships with that lender, and infer that loyalty can be captured by a traditional credit score. "Our study revealed clear decreases in delinquency as a function of relationships even when controlling for credit score, with robust results particularly in the near-prime and sub-prime segments of the population," said Becker. "The conclusion is that loyalty is not adequately captured by traditional credit scores. This is exciting news for lenders and consumers alike, as it provides an avenue for extending credit to consumers who traditionally have constrained credit access but can yield quite profitable relationships for lenders."

Another insight gained from the study is that the Loyalty Effect is generally resistant to recessionary pressures. In 2007, auto loan delinquency dropped almost 48 percent between customers with one relationship and those with three relationships with a given lender. That difference in performance declined only marginally to 46 percent by the end of 2009, after the worst recession in recent times. "Loyalty is built far more effectively in difficult times than in good times. Consumers remember and appreciate those lenders that help them overcome a short-term liquidity crisis, or extend credit when others will not. Lenders must be prudent and thorough in evaluating consumer risk before extending credit; this study suggests that a consideration of the impact on the consumer of the decision to extend or deny credit, and the effect that might have on long-term loyalty, should be a part of that evaluation."

About TransUnion

As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion has employees in more than 25 countries on five continents. www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail

Telephone (312) 972-6646