TRUCKEE, CA--(Marketwire - Oct 2, 2012) - Clear Capital (www.clearcapital.com), a premium provider of data and real estate asset valuation, investment, and risk assessment, today released its Home Data Index™ (HDI) Market Report with data through September 2012. The HDI Market Report uses a broad array of public and proprietary data sources providing the most timely and relevant analysis available.

Report highlights include:

- Fiscal cliff uncertainty threatens to kill housing's momentum; consumer sentiment is key to housing market progress.

- Las Vegas is the next Phoenix with yearly home price growth of 8.0% and 9.5% forecasted over the next six months.

- National yearly home price growth of 3.6% picked up in September, with additional gains of 2.2% forecasted through winter.

"While housing continued to make progress in September, we've turned our focus to the impending fiscal cliff," said Dr. Alex Villacorta, Director of Research and Analytics at Clear Capital. "With forecasted gains of 2.2% over the next six months, the threat of the fiscal cliff could throw a wrench into the recovery.

"If the cliff is avoided, we still run the risk of damaging confidence with a resolution pushed against year-end deadlines. Confidence is key to turning the recovery's near term sprint into a marathon. The sooner businesses and consumers are reassured, the more likely they are to build, purchase, or loan on a house."

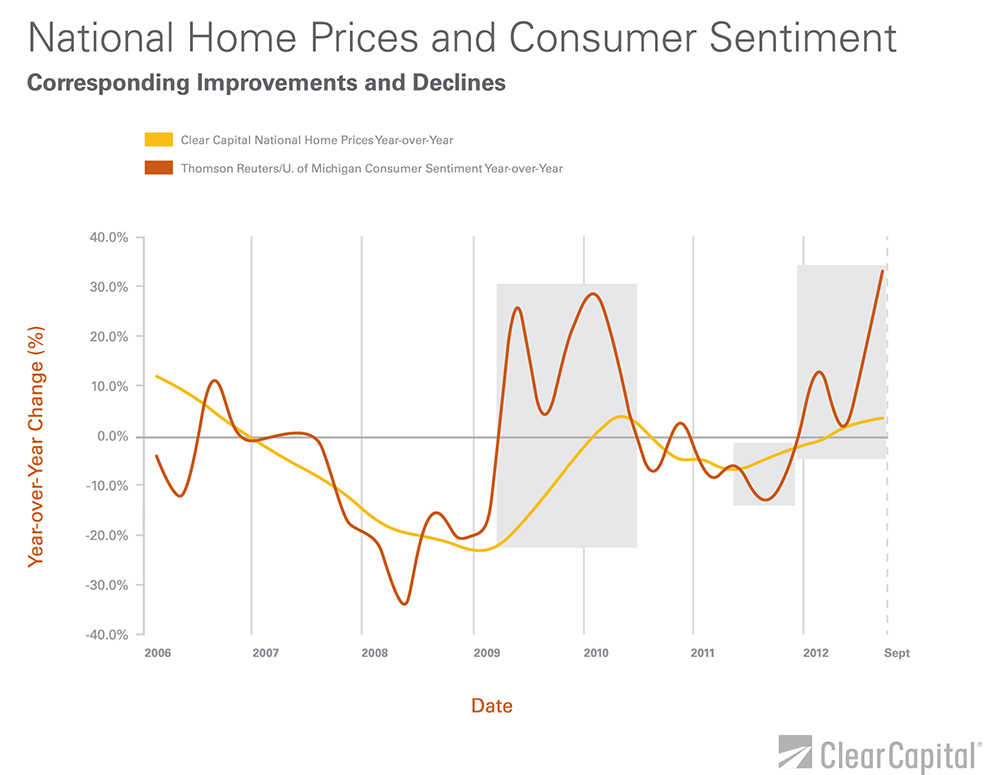

Housing and Sentiment: Threatened by Fiscal Policy, Boosted by Monetary Policy.

The good news: far more markets are improving than declining. Our forecast shows the recovery will sustain the typically slow winter, and start the spring buying season strong. As we approach the year's end, can fear from an impending fiscal cliff sway consumer confidence and discourage potential home buyers? We say yes, it can. Congress must make tough decisions before the 11th hour.

Economic uncertainty will keep buyers on the sidelines. Threatening to temper confidence is the fear Congress will not act in time to avert the looming fiscal cliff. The debt ceiling debate last year highlighted how dangerously close lawmakers are willing to come to deadlines before reaching an agreement. Consumers reacted negatively to the high level of uncertainty with a 14.3% drop in sentiment, the largest since the end of the recession. At the same time, home prices were experiencing the worst annual declines since the bottom of the market in 2009. In May 2011 the debt ceiling debate started to heat up, while home prices dropped 6.8% year-over-year. Annual home price declines persisted through 2011, hung over from the expiration of the first-time-home-buyer tax credit and the drop in consumer confidence. Prices finally saw relief in early 2012, following improvement in consumer sentiment.

Strength in consumer sentiment also corresponded with the only two housing improvements since the bottom in 2009. Between March 2009 and June 2010, consumer sentiment rebounded 32.6%. Over the same period, home prices went from seeing yearly declines of 22.7% to yearly growth of 4.0%. Similarly, between December 2011 and September 2012, consumer sentiment gained 12.0%, and home prices moved from yearly losses of 2.3% to gains of 3.6%.

Now, economic and housing improvements are priming pent up home buyer demand for a breakout. Consumer sentiment has finally rebounded from debt ceiling debate lows of last year, up 31.8%. Homebuilders are echoing consumers, with confidence at a five year high. While the Fed's recent announcement of QE3 should further boost expectations for housing, it might not be enough to overcome fear of the cliff.

Results and Forecast: Heading into uncertainty on solid ground.

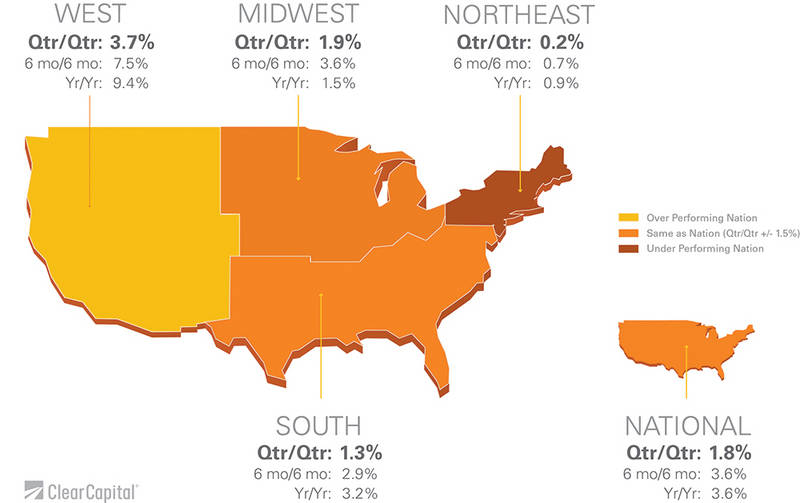

The recovery continued to unfold in September at the national and regional levels with gains across the board. 1.8% quarterly growth at the national level was driven in part by gains in the West. The West posted notable quarterly gains of 3.7%, the fifth consecutive month it's led regional gains. The Midwest and South regions had quarterly home price gains of 1.9% and 1.3%, respectively. The Northeast posted the weakest quarterly gains of 0.2%.

Yearly growth is forecasted to shake off winter's chill and continue through the first quarter of 2013. National prices closed out the third quarter 3.6% higher than the previous year. If the looming fiscal cliff is averted, the national home price forecast through Q1 2013 projects a 2.2% gain.

At the regional level, the West continued to dominate with 9.4% in yearly gains. This is the highest yearly gain the region has recorded since the second quarter in 2006. The first in, first out recovery has been driven by harder hit markets, many of which reside in the West. Forecasted gains of 5.3% over the next six months in the West are projected to drive a sustained recovery at the national level through winter.

The South and Midwest also saw yearly gains of 3.2% and 1.5%, respectively. The South should see further price advances of 1.9% through March 2013 and the Midwest 0.8%. The Northeast continued to see yearly gains soften, with prices rising just 0.9% over the previous year. Home prices in the Northeast are expected to do more of the same and remain relatively flat, growing 0.9% over the next six months.

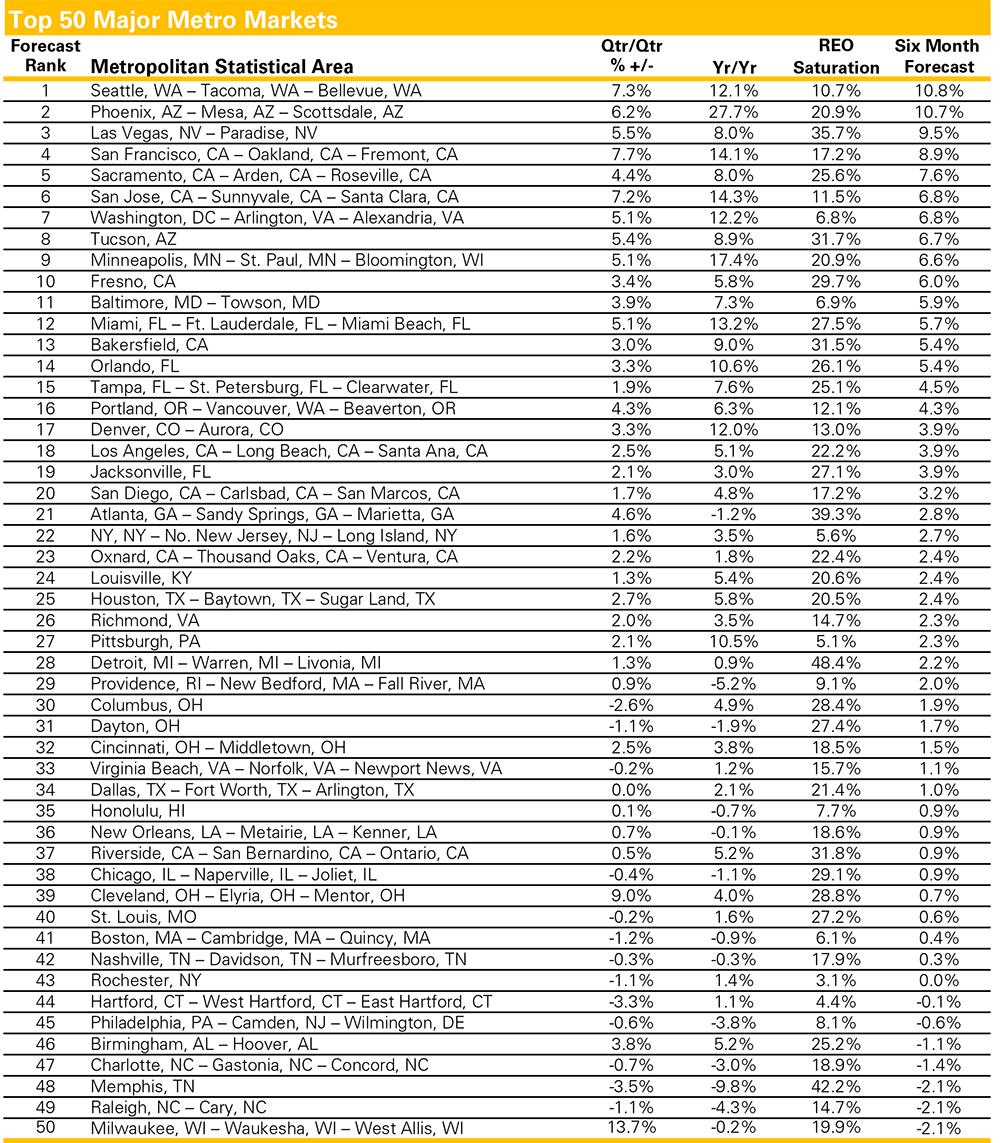

| Top 50 Major Metro Markets | ||||||||||||||

| Forecast Rank |

|

Metropolitan Statistical Area | Qtr/Qtr % +/- |

|

Yr/Yr | REO Saturation |

Six Month Forecast |

|||||||

| 1 | Seattle, WA - Tacoma, WA - Bellevue, WA | 7.3 | % | 12.1 | % | 10.7 | % | 10.8 | % | |||||

| 2 | Phoenix, AZ - Mesa, AZ - Scottsdale, AZ | 6.2 | % | 27.7 | % | 20.9 | % | 10.7 | % | |||||

| 3 | Las Vegas, NV - Paradise, NV | 5.5 | % | 8.0 | % | 35.7 | % | 9.5 | % | |||||

| 4 | San Francisco, CA - Oakland, CA - Fremont, CA | 7.7 | % | 14.1 | % | 17.2 | % | 8.9 | % | |||||

| 5 | Sacramento, CA - Arden, CA - Roseville, CA | 4.4 | % | 8.0 | % | 25.6 | % | 7.6 | % | |||||

| 6 | San Jose, CA - Sunnyvale, CA - Santa Clara, CA | 7.2 | % | 14.3 | % | 11.5 | % | 6.8 | % | |||||

| 7 | Washington, DC - Arlington, VA - Alexandria, VA | 5.1 | % | 12.2 | % | 6.8 | % | 6.8 | % | |||||

| 8 | Tucson, AZ | 5.4 | % | 8.9 | % | 31.7 | % | 6.7 | % | |||||

| 9 | Minneapolis, MN - St. Paul, MN - Bloomington, WI | 5.1 | % | 17.4 | % | 20.9 | % | 6.6 | % | |||||

| 10 | Fresno, CA | 3.4 | % | 5.8 | % | 29.7 | % | 6.0 | % | |||||

| 11 | Baltimore, MD - Towson, MD | 3.9 | % | 7.3 | % | 6.9 | % | 5.9 | % | |||||

| 12 | Miami, FL - Ft. Lauderdale, FL - Miami Beach, FL | 5.1 | % | 13.2 | % | 27.5 | % | 5.7 | % | |||||

| 13 | Bakersfield, CA | 3.0 | % | 9.0 | % | 31.5 | % | 5.4 | % | |||||

| 14 | Orlando, FL | 3.3 | % | 10.6 | % | 26.1 | % | 5.4 | % | |||||

| 15 | Tampa, FL - St. Petersburg, FL - Clearwater, FL | 1.9 | % | 7.6 | % | 25.1 | % | 4.5 | % | |||||

| 16 | Portland, OR - Vancouver, WA - Beaverton, OR | 4.3 | % | 6.3 | % | 12.1 | % | 4.3 | % | |||||

| 17 | Denver, CO - Aurora, CO | 3.3 | % | 12.0 | % | 13.0 | % | 3.9 | % | |||||

| 18 | Los Angeles, CA - Long Beach, CA - Santa Ana, CA | 2.5 | % | 5.1 | % | 22.2 | % | 3.9 | % | |||||

| 19 | Jacksonville, FL | 2.1 | % | 3.0 | % | 27.1 | % | 3.9 | % | |||||

| 20 | San Diego, CA - Carlsbad, CA - San Marcos, CA | 1.7 | % | 4.8 | % | 17.2 | % | 3.2 | % | |||||

| 21 | Atlanta, GA - Sandy Springs, GA - Marietta, GA | 4.6 | % | -1.2 | % | 39.3 | % | 2.8 | % | |||||

| 22 | NY, NY - No. New Jersey, NJ - Long Island, NY | 1.6 | % | 3.5 | % | 5.6 | % | 2.7 | % | |||||

| 23 | Oxnard, CA - Thousand Oaks, CA - Ventura, CA | 2.2 | % | 1.8 | % | 22.4 | % | 2.4 | % | |||||

| 24 | Louisville, KY | 1.3 | % | 5.4 | % | 20.6 | % | 2.4 | % | |||||

| 25 | Houston, TX - Baytown, TX - Sugar Land, TX | 2.7 | % | 5.8 | % | 20.5 | % | 2.4 | % | |||||

| 26 | Richmond, VA | 2.0 | % | 3.5 | % | 14.7 | % | 2.3 | % | |||||

| 27 | Pittsburgh, PA | 2.1 | % | 10.5 | % | 5.1 | % | 2.3 | % | |||||

| 28 | Detroit, MI - Warren, MI - Livonia, MI | 1.3 | % | 0.9 | % | 48.4 | % | 2.2 | % | |||||

| 29 | Providence, RI - New Bedford, MA - Fall River, MA | 0.9 | % | -5.2 | % | 9.1 | % | 2.0 | % | |||||

| 30 | Columbus, OH | -2.6 | % | 4.9 | % | 28.4 | % | 1.9 | % | |||||

| 31 | Dayton, OH | -1.1 | % | -1.9 | % | 27.4 | % | 1.7 | % | |||||

| 32 | Cincinnati, OH - Middletown, OH | 2.5 | % | 3.8 | % | 18.5 | % | 1.5 | % | |||||

| 33 | Virginia Beach, VA - Norfolk, VA - Newport News, VA | -0.2 | % | 1.2 | % | 15.7 | % | 1.1 | % | |||||

| 34 | Dallas, TX - Fort Worth, TX - Arlington, TX | 0.0 | % | 2.1 | % | 21.4 | % | 1.0 | % | |||||

| 35 | Honolulu, HI | 0.1 | % | -0.7 | % | 7.7 | % | 0.9 | % | |||||

| 36 | New Orleans, LA - Metairie, LA - Kenner, LA | 0.7 | % | -0.1 | % | 18.6 | % | 0.9 | % | |||||

| 37 | Riverside, CA - San Bernardino, CA - Ontario, CA | 0.5 | % | 5.2 | % | 31.8 | % | 0.9 | % | |||||

| 38 | Chicago, IL - Naperville, IL - Joliet, IL | -0.4 | % | -1.1 | % | 29.1 | % | 0.9 | % | |||||

| 39 | Cleveland, OH - Elyria, OH - Mentor, OH | 9.0 | % | 4.0 | % | 28.8 | % | 0.7 | % | |||||

| 40 | St. Louis, MO | -0.2 | % | 1.6 | % | 27.2 | % | 0.6 | % | |||||

| 41 | Boston, MA - Cambridge, MA - Quincy, MA | -1.2 | % | -0.9 | % | 6.1 | % | 0.4 | % | |||||

| 42 | Nashville, TN - Davidson, TN - Murfreesboro, TN | -0.3 | % | -0.3 | % | 17.9 | % | 0.3 | % | |||||

| 43 | Rochester, NY | -1.1 | % | 1.4 | % | 3.1 | % | 0.0 | % | |||||

| 44 | Hartford, CT - West Hartford, CT - East Hartford, CT | -3.3 | % | 1.1 | % | 4.4 | % | -0.1 | % | |||||

| 45 | Philadelphia, PA - Camden, NJ - Wilmington, DE | -0.6 | % | -3.8 | % | 8.1 | % | -0.6 | % | |||||

| 46 | Birmingham, AL - Hoover, AL | 3.8 | % | 5.2 | % | 25.2 | % | -1.1 | % | |||||

| 47 | Charlotte, NC - Gastonia, NC - Concord, NC | -0.7 | % | -3.0 | % | 18.9 | % | -1.4 | % | |||||

| 48 | Memphis, TN | -3.5 | % | -9.8 | % | 42.2 | % | -2.1 | % | |||||

| 49 | Raleigh, NC - Cary, NC | -1.1 | % | -4.3 | % | 14.7 | % | -2.1 | % | |||||

| 50 | Milwaukee, WI - Waukesha, WI - West Allis, WI | 13.7 | % | -0.2 | % | 19.9 | % | -2.1 | % | |||||

MSA Market Analysis and Forecast: Las Vegas, not just a gamble anymore.

The top 50 metro markets generally improved over the last quarter, with average price gains of 2.4%. More significant progress was made over the last year, with average growth of 4.7% for the group.

Phoenix held its ground in September as the strongest metro with 27.7% yearly growth. The metro has become a benchmark for recovering markets, with low price points on distressed sales attracting buyers. Over the next two quarters, Phoenix prices are projected to expand another 10.7%. As this low price point market continues to rise, it will eventually price out some of the current demand pool. But at this point, it continues to offer attractive potential to buyers. Should the forecast be realized, Phoenix's future median price of $174,000 would remain 33.3% below the peak of $262,000.

Meanwhile, Las Vegas is shaping up to be the next Phoenix. Yearly home price gains of 8.0% should see additional growth of 9.5% over the next six months. The market found its footing despite relatively high rates of REO saturation at 35.7%. Like Phoenix, Las Vegas is seeing gains now concentrated in the discounted price segments, and REO saturation shifted from a headwind to a tailwind.

If Las Vegas looks like the next Phoenix, Memphis looks more like the next Atlanta. Home prices in Memphis are down 48.3% from the peak, with further declines expected. Over the next six months, Memphis home prices are forecasted to fall another 2.1%. REO saturation rose by 8.6 percentage points over the year, to 42.2%. The market has yet to acclimate to the highly distressed environment. By comparison, Detroit is the only other market in the top 50 metros that has an REO saturation rate over 40.0%. With yearly declines of 9.8%, Memphis is a hard hit market that has yet to find the bottom.

The six month forecast for the top 50 metros shows all but seven should see growth over the next six months. Not surprising, two thirds of the top 15 metros are in the West. Regardless, the fiscal cliff has no geographic boundary. Even the healthiest of markets will suffer under the weight of uncertainty.

About the Clear Capital Home Data Index (HDI) Market Report

The Clear Capital HDI Market Report provides insights into market trends and other leading indices for the real estate market at the national and local levels. A critical difference in the value of the HDI Market Report is the capability of Clear Capital to provide more timely and granular reporting than other home price index providers.

The Clear Capital HDI Market Report:

- Offers the real estate industry (investors, lenders, and servicers), government agencies, and the public insight into the most recent pricing conditions, not only at the national and metropolitan level, but within local markets as well.

- Is built on the most recent information available from recorder/assessor offices, and then further enhanced by adding the company's proprietary streaming market data for the most comprehensive geographic coverage and local insights available.

- Reflects nationwide coverage of sales transactions and aggregates this comprehensive dataset at ten different geographic levels, including hundreds of metropolitan statistical areas (MSAs) and sub-ZIP code boundaries.

- Includes equally-weighted distressed bank owned sales (REOs) from around the country to give the most real world look of pricing dynamics across all sales types.

- Allows for the most current market data by providing more frequent updates with patent pending rolling quarter technology. This ensures decisions are based on the most up-to-date information available.

Clear Capital Home Data Index Methodology

- Generates the timeliest indices in patent pending rolling quarter intervals that compare the most recent four months to the previous three months. The rolling quarters have no fixed start date and can be used to generate indices as data flows in, significantly reducing the multi-month lag time experienced with other indices.

- Includes both fair market and institutional (real estate owned) transactions, giving equal weight to all market transactions and identifying price tiers at a market specific level. By giving equal weight to all transactions, the HDI is truly representative of each unique market.

- Results from an address-level cascade create an index with the most granular, statistically significant market area available.

- Provides weighted repeat sales and price-per-square-foot index models that use multiple sale types, including single-family homes, multi-family homes, and condominiums.

About Clear Capital

Clear Capital (www.clearcapital.com) is a premium provider of data and solutions for real estate asset valuation and risk assessment for large financial services companies. Our products include appraisals, broker price opinions, property condition inspections, value reconciliations, automated valuation models, quality assurance services, and home data indices. Clear Capital's combination of progressive technology, high caliber in-house staff, and a well-trained network of more than 40,000 field experts sets a new standard for accurate, up-to-date, and well documented valuation data and assessments. The Company's customers include the largest U.S. banks, investment firms, and other financial organizations.

The information contained in this report is based on sources that are deemed to be reliable; however no representation or warranty is made as to the accuracy, completeness, or fitness for any particular purpose of any information contained herein. This report is not intended as investment advice, and should not be viewed as any guarantee of value, condition, or other attribute.

Contact Information:

Media Contact:

Alanna Harter

Marketing Manager

Clear Capital

530.550.2515

alanna.harter@clearcapital.com