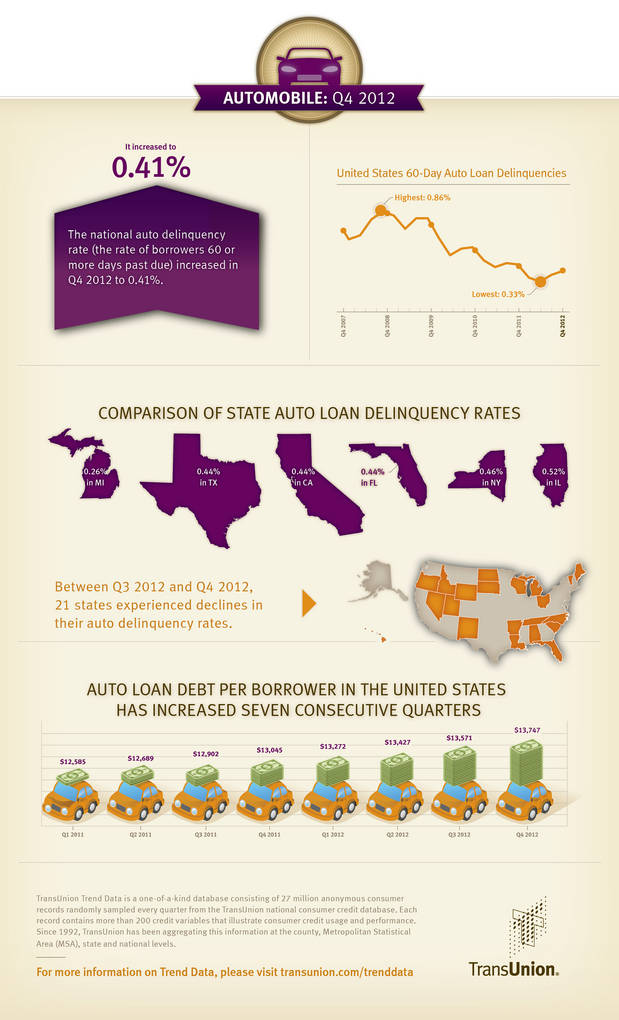

CHICAGO, IL--(Marketwire - Feb 26, 2013) - The national auto loan delinquency rate (the ratio of borrowers 60 or more days past due) continued to remain near historic low levels in the fourth quarter of 2012 ending the year at 0.41%. While the delinquency rate rose from 0.38% in Q3 2012, it has dropped five basis points from the end of 2011 when the delinquency rate was 0.46%.

Continuing a recent trend, bank auto debt per borrower rose for the seventh straight quarter, increasing 5.4% from $13,045 in Q4 2011 to $13,747 in Q4 2012.

"As expected auto loan delinquencies rose slightly in the fourth quarter, though they remain near the all-time record low set in the second quarter of 2012," said Peter Turek, automotive vice president in TransUnion's financial services business unit. "We continue to see increasing auto debt per borrower as the new and used car sales market remains relatively strong."

Between Q3 2012 and Q4 2012, more than half of states (28) experienced increases in their auto delinquency rates. However, on a year-over-year basis only 14 states experienced increases in their auto delinquency rates. On a more granular level, 52.5% of metropolitan areas saw decreases in their auto delinquency rates between Q4 2011 and Q4 2012.

TransUnion's analysis also found that auto loan originations continue to increase. Total new auto loan and lease originations in Q3 2012 grew by approximately 15.8% relative to the same period last year. Auto loan originations are analyzed one quarter in arrears, to account for the reporting lag of new accounts.

The share of non-prime, higher-risk consumers (with a VantageScore® credit score lower than 700 on a scale of 501-990) was 32.4%. This is somewhat higher than one year ago (30.6% in Q3 2011), and is significantly higher than the 27.6% observed in Q3 2010. In volume terms, the number of new accounts originated to non-prime consumers increased 20.5% in Q3 2012 compared to Q3 2011. In addition, average balances for the newly originated auto loans increased by 1.66% in Q3 2012 relative to the same period last year, from $18,028 in Q3 2011 to $18,326 in Q3 2012.

"We've been observing an increase in sub-prime borrowers in the auto loan space now for several quarters and we do expect this will eventually push the overall delinquency numbers higher," said Turek. "New loan originations are growing and that has helped the 60 day or more delinquency rate remain low, and we forecast that delinquencies will remain about the same in the first quarter, possibly even dropping slightly."

TransUnion's forecast is based on various economic assumptions, such as unemployment rates, consumer sentiment, disposable income, and interest rates. The forecast changes as the economy deviates from a conservative forecast or if there are unanticipated shocks to the economy affecting recovery.

This information is reported by TransUnion and is part of its ongoing series of quarterly analyses of credit-active U.S. consumers and how they are managing credit related to mortgages, credit cards and auto loans.

Q4 2012 Bank Auto Statistics - Delinquency Rates

| Quarter over Quarter | Q3 2012 | Q4 2012 | Pct. Change | |||

| USA | 0.38 | % | 0.41 | % | 7.89 | % |

| Year over year | Q4 2011 | Q4 2012 | Pct. Change | |||

| USA | 0.46 | % | 0.41 | % | (10.87 | %) |

| Highest Bank Auto Delinquency States | Q4 2012 | |

| Mississippi | 0.76 | % |

| Louisiana | 0.72 | % |

| West Virginia | 0.64 | % |

| Bank Auto Delinquency in Key States | Q4 2012 | |

| California | 0.44 | % |

| Florida | 0.44 | % |

| Illinois | 0.52 | % |

| Michigan | 0.26 | % |

| New York | 0.46 | % |

| Texas | 0.44 | % |

| Top 3 Year-over-Year Increases | Q4 2011 | Q4 2012 | Pct. Change | |||

| New Hampshire | 0.25 | % | 0.47 | % | 88.00 | % |

| West Virginia | 0.51 | % | 0.64 | % | 25.49 | % |

| Iowa | 0.29 | % | 0.36 | % | 24.14 | % |

Q4 2012 Bank Auto Statistics - Bank Auto Debt Per Borrower

| Quarter over Quarter | Q3 2012 | Q4 2012 | Pct. Change | |||||

| USA | $ | 13,571 | $ | 13,747 | 1.29 | % | ||

| Year over Year | Q4 2011 | Q4 2012 | Pct. Change | |||||

| USA | $ | 13,045 | $ | 13,747 | 5.38 | % | ||

| Highest Bank Auto Debt Per Borrower | Q4 2012 | |

| Texas | $ | 15,850 |

| Wyoming | $ | 15,712 |

| Louisiana | $ | 15,217 |

| Bank Auto Debt Per Borrower in Key States | Q4 2012 | |

| California | $ | 14,971 |

| Florida | $ | 14,457 |

| Illinois | $ | 13,333 |

| Michigan | $ | 12,522 |

| New York | $ | 12,748 |

| Texas | $ | 15,850 |

| Top 3 Year-over-Year Increases | Q4 2011 | Q4 2012 | Pct. Change | |||||

| New Mexico | $ | 12,838 | $ | 14,434 | 12.43 | % | ||

| Texas | $ | 14,404 | $ | 15,850 | 10.04 | % | ||

| Mississippi | $ | 13,167 | $ | 14,385 | 9.25 | % | ||

Supporting Resources/Links

TransUnion Trend Data Interactive U.S. Map

TransUnion 3Q12 Auto Statistics

TransUnion Mortgage Loan Modification Study

TransUnion Payment Hierarchy Study

TransUnion Deleveraging Analysis

TransUnion Life After Foreclosure Study

TransUnion on Twitter

TransUnion's Trend Data database

The report is part of an ongoing series of quarterly consumer lending sector analyses focusing on credit card, bank auto loan and bank auto data available on TransUnion's Web site. Information for this analysis is culled from TransUnion's Trend Data and the anonymous credit files of approximately 10 percent of credit-active U.S. consumers, providing a real-life perspective on how they are managing their credit health.

TransUnion's Trend Data, a one-of-a-kind database consisting of 27 million anonymous consumer records randomly sampled every quarter from TransUnion's national consumer credit database. Each record contains more than 200 credit variables that illustrate consumer credit usage and performance. Since 1992, TransUnion has been aggregating this information at the county, Metropolitan Statistical Area (MSA), state and national levels.

About TransUnion

As a global leader in information and risk management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering high quality data, and integrating advanced analytics and enhanced decision-making capabilities. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion reaches businesses and consumers in 33 countries around the world on five continents. www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail

Telephone 312 985 3059