TRUCKEE, Calif., Feb. 3, 2014 (GLOBE NEWSWIRE) -- Clear Capital®, the premium provider of data and solutions for real estate asset valuation and collateral risk assessment, today released its Home Data Index™ (HDI) Market Report with data through January 2014. Using a broad array of public and proprietary data sources, the HDI Market Report publishes the most granular home data and analysis earlier than nearly any other index provider in the industry.

- National home prices are right in line (within 2%) with inflation adjusted long-run average levels, indicating prices have normalized post-bubble and future rates of growth will look more like historical rates of growth. Home prices have typically gained between 3% and 5% a year. At our current quarterly rate of national growth (1.2%), peak prices won't be reached until the year 2021, a healthy move for the industry overall.

- In real terms, inflation adjusted home prices at the metro level show 46 out of 50 metro markets' home price levels at pre-2003 levels, with 25 out of 50 metros reporting prices below 2000 levels (See Graph 1). Because the majority of markets remain far off peak values, the peak becomes a less relevant point of reference for new investors and homebuyers. Honolulu is the only metro out of the top 50 to see home prices within peak levels, with inflation adjusted home prices resting at levels last seen in 2005. This anomaly has, in part, been driven by very unique supply and demand, a benefit of being a highly desirable tropical island.

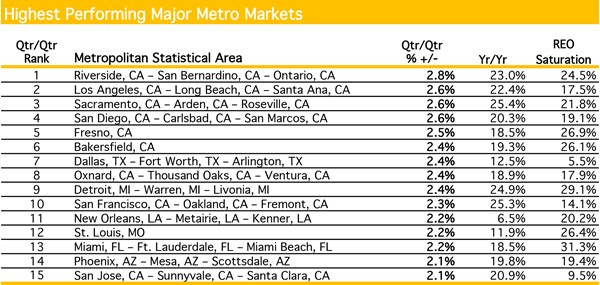

- While prices remain far off peak values, current trends continue to moderate across the country (See National Map). National yearly gains cooled to 10.8%, a trend that should continue over the next several months. Yearly gains at the metro level are moderating as well, with Sacramento now seeing the highest yearly gain at 25.4%, down from a high of 28% in October. Las Vegas has seen substantial pull back in January with yearly gains of just 21.3%, down from 32.4% in October. The market's relatively quick moderating pattern indicates it reached an unsustainable rate of growth and is now correcting back to more normal historical rates of growth.

- Contact Alanna Harter for your January 2014 file of the Top 30 MSAs or access our data on the Bloomberg Professional service by typing CLCA <GO>.

"With the majority of metro markets still so far below peak prices, it's time for conversations surrounding price trends to shift away from the 2006 peak as the point of reference, and back to current trends and forecasts," said Dr. Alex Villacorta, vice president of research and analytics at Clear Capital. "While there are certainly investors and homeowners holding real estate assets that will be underwater for seven years or more, the current housing market is positioned to behave very similar or even below historical norms, given the current economic climate. For new deals and investors without legacy assets, the new housing environment should be framed in terms of more typical, moderate rates of growth with tempered optimism for the ongoing housing recovery.

Nationally, we don't see evidence of a price bubble forming again. Double digit gains over the last year, while similar to rates of growth in the run-up to the bubble, are off a much lower price floor. Phoenix and Las Vegas, however, are showing signs of overheating. These markets skyrocketed off very low price floors as their low-tier and distressed market segments exploded with demand. Each market saw yearly gains top out around 30%, and now are seeing price gains cool substantially. Las Vegas has seen more than a 10 percentage point pull back in just three short months, even though prices remain 20.8% below 2000 levels, after adjusting for inflation. Meanwhile, Phoenix's yearly gains are down to 19.8%, with prices now 1.9% above 2000 levels after adjusting for inflation. We'll be watching these markets closely throughout the winter to see how demand holds up."

Graph 1: http://www.globenewswire.com/newsroom/prs/?pkgid=23340

National Map: http://www.globenewswire.com/newsroom/prs/?pkgid=23342

Highest Performing MSAs: http://www.globenewswire.com/newsroom/prs/?pkgid=23343

Lowest Performing MSAs: http://www.globenewswire.com/newsroom/prs/?pkgid=23339