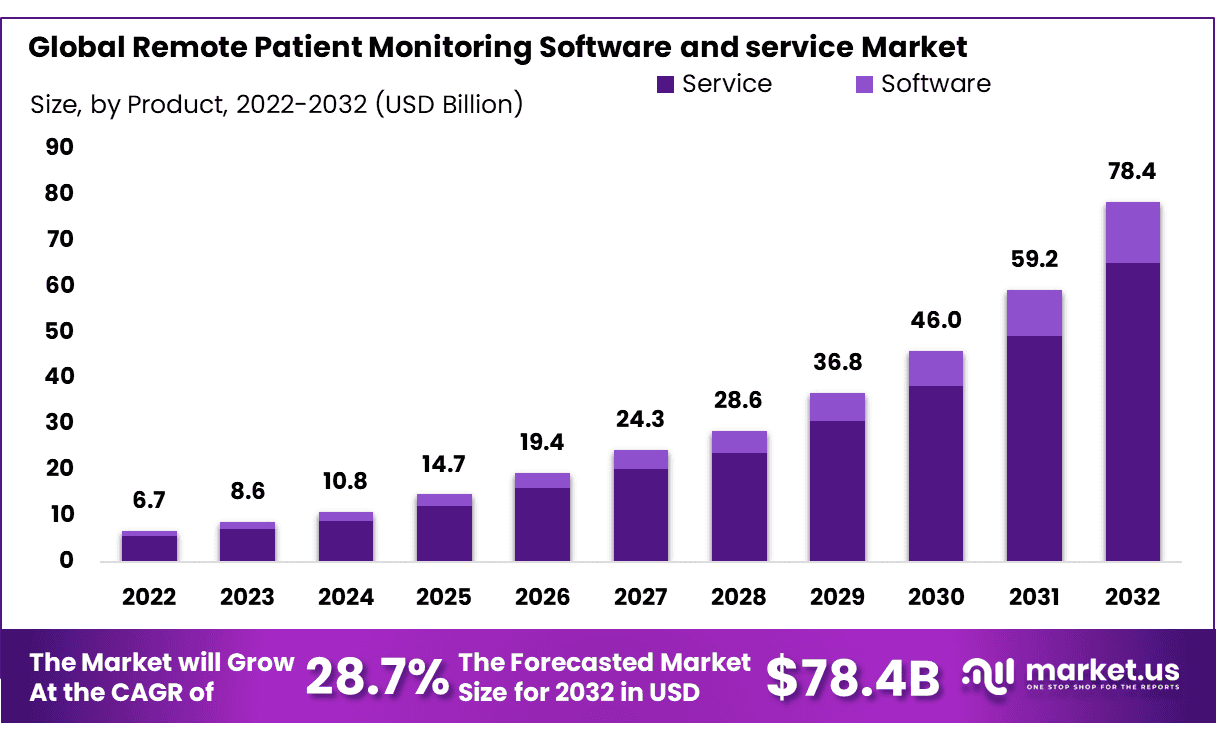

New York, Dec. 14, 2023 (GLOBE NEWSWIRE) -- According to Market.us, Global Remote Patient Monitoring (RPM) software and services Market size is expected to be worth around USD 78.4 Billion by 2032 from USD 8.6 Billion in 2023, growing at a CAGR of 28.7% during the forecast period from 2023 to 2032.

Remote Patient Monitoring (RPM) software and services play an integral part in modern healthcare by harnessing technology to observe patients outside traditional medical environments. This comprehensive solution comprises wearable devices equipped with sensors that track vital signs, mobile apps enabling patient input and communication, and sophisticated software platforms enabling healthcare professionals to access real-time health data. Key features of continuous monitoring solutions include automatic alerts for abnormal conditions, patient engagement tools, and seamless interoperability with electronic health records.

RPM has seen widespread adoption in chronic disease management, providing constant monitoring and timely intervention. Integrating RPM solutions with telehealth platforms enhances the virtual care experience, while ongoing technological developments continue to expand their capabilities. Regulations and reimbursement policies have evolved to accommodate RPM implementation, reflecting its rising importance in providing efficient healthcare to patients. To stay abreast of market reports and industry analyses, as well as explore websites of major players in this space, referring to current market reports is recommended for insight.

To understand Geography Trends, Download Sample Report Here: https://market.us/report/remote-patient-monitoring-software-and-services-market/request-sample/

Key Takeaway

- Market Size: Remote Patient Monitoring Software and Services Market size is expected to be worth around USD 78.4 Billion by 2032 from USD 8.6 Billion in 2023.

- Market Growth: The market growing at a CAGR of 28.7 % during the forecast period from 2023 to 2032.

- Product Analysis: The services category dominated the global industry and contributed to over 83.20% of the total revenue.

- Application Analysis: The market is segmented into cardiovascular diseases, cancer, diabetes, neurological disorders, and other applications.

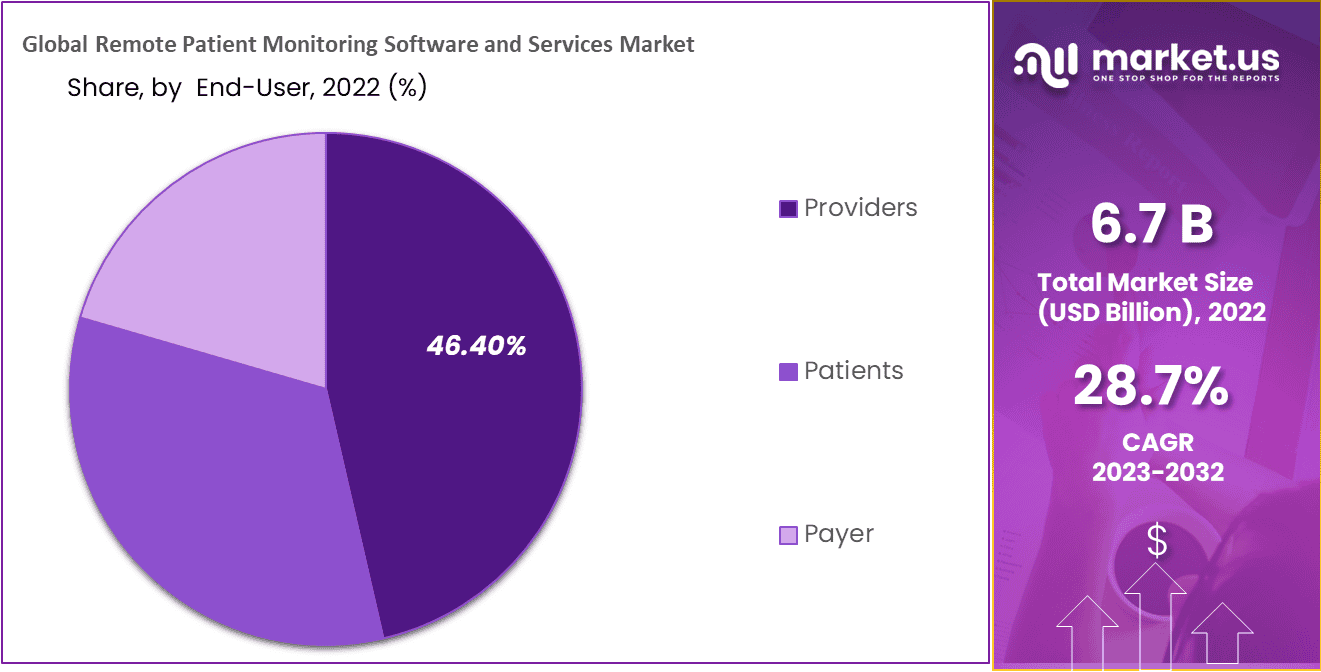

- End-Use Analysis: The provider’s segment dominated the market with a 46.40% share in 2022.

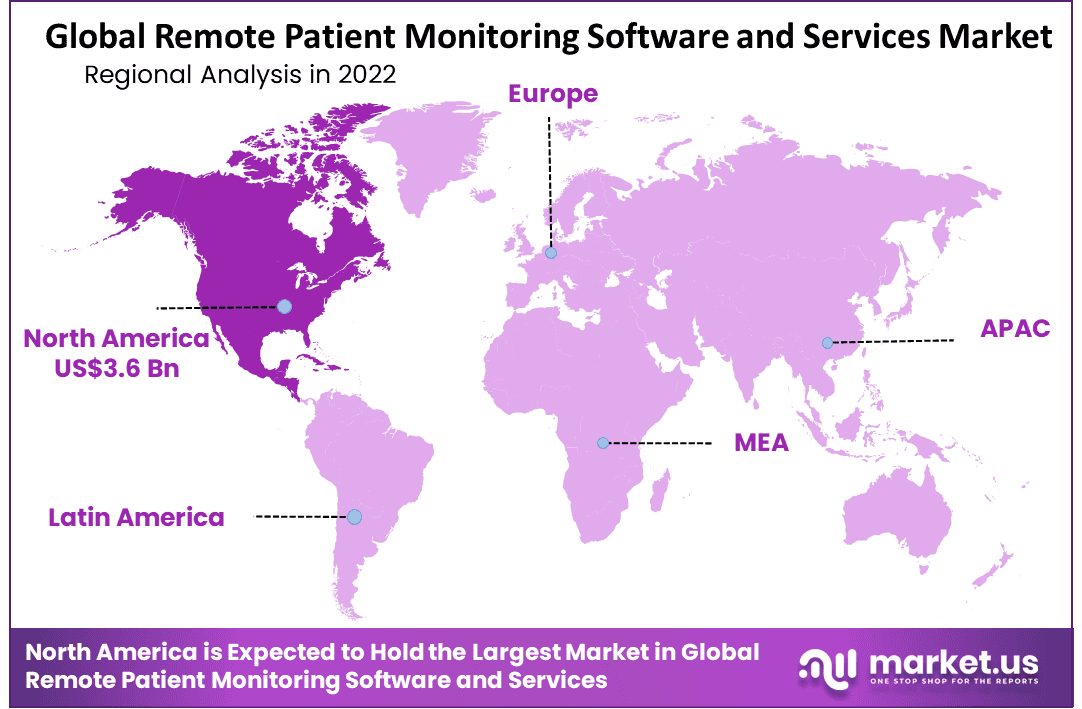

- Regional Analysis: North America held the largest market share, with 53.5%, and held USD 3.6 Billion in revenues in remote patient monitoring software & services in 2022.

- Components: RPM solutions typically include wearable devices with sensors, mobile apps for patient input and communication, and software platforms for healthcare providers to access and analyze data.

- Features: Real-time monitoring, automated alerts, patient engagement tools, and interoperability with electronic health records are key features of RPM software and services.

- Clinical Applications: RPM is particularly valuable for managing chronic diseases, allowing continuous monitoring and early intervention to improve patient outcomes.

Factors affecting the growth of the Remote Patient Monitoring (RPM) software and services Market

Various factors influence the growth of Remote Patient Monitoring (RPM) software and services Market are;

- Aging Population: With an increasing world-wide aging population comes an increase in chronic diseases and an increased need for continuous monitoring - leading to greater adoption of RPM solutions.

- Prevalence of Chronic Diseases: Ultimately RPM solutions may play a vital role in monitoring chronic diseases more efficiently. As chronic diseases such as diabetes, cardiovascular conditions, and respiratory ailments increase, monitoring must become part of everyday life for effective management.

- Technological Advancements: Constant advancements in wearable technology, sensors and data analytics enhance RPM solutions' accuracy, usability and efficiency.

- Telehealth Integration: Integrating RPM with telehealth platforms expands healthcare providers' virtual care capabilities and allows them to offer comprehensive patient care remotely.

- Patient Preference for Home-Based Care: Patients increasingly prefer home-based care over frequent trips to healthcare facilities, increasing demand for remote patient monitoring solutions that enable monitoring from within their own homes.

To understand how our report can make a difference to your business strategy, Inquire about a brochure at https://market.us/report/remote-patient-monitoring-software-and-services-market/#inquiry

Competitive Landscape

The market for remote patient monitoring software and services exhibits a fragmented landscape, marked by numerous companies operating both regionally and globally. There is fierce competition in this industry driven by newcomers entering with innovative offerings to offer new competitive pressures to existing players.

Market Key Players

- Teladoc Health, Inc.

- Medtronic Plc.

- GE Healthcare

- Siemens Healthineers AG

- Philips Healthcare

- Caretaker Medical

- OMRON Healthcare

- BioIntelliSense

- Other Key Players

Regional Analysis

In 2022, North America emerged as the dominant 53.5% and held USD 3.6 Billion in revenues in the global market, claiming the highest revenue share. The region is poised for further growth, fueled by the widespread adoption of remote patient monitoring (RPM) services and the availability of robust digital infrastructure. The initiatives taken by regional governments are expected to play a pivotal role in accelerating the utilization of RPM solutions. An illustrative example is the introduction of the Rural Remote Monitoring Patient Act by U.S. lawmakers in June 2021.

Scope of the Report

| Report Attributes | Details |

| Market Value (2023) | USD 8.6 Billion |

| Forecast Revenue 2032 | USD 78.4 Billion |

| CAGR (2023 to 2032) | 28.7% |

| North America Revenue Share | 53.5% |

| Base Year | 2023 |

| Historic Period | 2018 to 2022 |

| Forecast Year | 2023 to 2032 |

Market Drivers

The Remote Patient Monitoring (RPM) software and services market has been propelled forward by an increase in chronic diseases and an aging global population. RPM provides a proactive approach to healthcare, allowing continuous monitoring of vital signs and health parameters in real time for every patient. Technology advances, particularly those related to wearables and data analytics, drive market expansion by improving remote monitoring accuracy and efficiency.

Telehealth solutions, especially since the COVID-19 pandemic, have greatly accelerated RPM integration into larger healthcare systems, spurring market expansion. Furthermore, government initiatives and supportive regulatory frameworks contribute to this upward trajectory, creating an ideal environment for developing and adopting innovative RPM solutions.

Market Restraints

While Remote Patient Monitoring (RPM) market growth remains promising, its development can present challenges related to data security and privacy concerns. As more health data is transmitted and stored securely, safeguarding its confidentiality becomes ever more essential.

Data breaches and unauthorized access are major roadblocks to wider adoption of RPM solutions. Interoperability issues between healthcare systems and protocols may impede seamless integration, thus diminishing its efficacy. Resistance to change within traditional settings as well as cost considerations associated with RPM solutions could hinder their widespread adoption.

Market Opportunities

The Remote Patient Monitoring (RPM) market holds immense promise due to an escalating trend toward personalized and patient-centric healthcare delivery. AI and data analytics allow RPM solutions to provide more precise predictive analyses, enabling early identification of health issues and personalized care plans. Telehealth presents an enormous growth opportunity, as RPM becomes an integral component of virtual healthcare delivery.

Market players can capitalize on the increased demand for user-friendly and patient-engaging RPM solutions as global populations become more tech savvy. Additionally, ongoing R&D activities aimed at increasing interoperability between RPM systems and data security concerns provide avenues for innovation, expanding market reach and creating more robust yet widely accepted remote monitoring solutions.

Immediate Delivery Available | Buy This Premium Research Report https://market.us/purchase-report/?report_id=105725

Report Segmentation of the Remote Patient Monitoring (RPM) software and services Market

Product Type Analysis

Global market segments for services and software services. By 2022, services were the dominant force in this industry and made up over 83.20% of total revenues. This success can be attributed to the rising usage of Remote Patient Monitoring (RPM) software and services aimed at reducing hospital admissions. Notable services included within this category include emergency response systems, medication administration and data-driven patient engagement solutions.

Emergency response systems play a vital role in minimizing response times and optimizing hospital resource allocation, improving overall patient treatment outcomes and decreasing hospital admission rates. By emphasizing emergency response systems as part of RPM solutions for improved care delivery while simultaneously meeting their larger goal of decreasing admission burden, emergency response systems play an integral role.

Application Analysis

In 2022, cardiovascular diseases, cancer, diabetes, neurological disorders and other applications accounted for 56.30% of market. With an increasing incidence of chronic conditions like Alzheimer's, arthritis, hypertension and paralysis worldwide and an aging population this has resulted in an unprecedented demand for Remote Patient Monitoring (RPM) software solutions and software products. This demand is especially critical. Mobility challenges caused by arthritis and paralysis necessitate RPM services for patients, contributing to sector growth.

Diabetes monitoring services may experience the fastest expansion during this forecast period as diabetes requires ongoing remote blood glucose level monitoring that has major health consequences; partnerships between public and private entities for diabetes monitoring could further boost this segment's expansion.

End-User Insight

End-users for remote patient monitoring services include payers, patients, and providers. By 2022, providers led with 46.40% market share. Hospitals, clinics, and physicians all witnessed considerable growth due to the increasing adoption of remote patient monitoring services.

American Medical Association research showed that 53% of physicians expressed interest in using remote monitoring services by 2021, signaling an optimistic trend for the industry. Medical providers stand to gain from increased adoption; patient usage will likely see exponential growth due to its increasing use for cost reduction and communication with healthcare professionals resulting in significant expansion within this category.

Recent Developments in the Remote Patient Monitoring (RPM) software and services Market

- March 2023: Siemens Healthineers AG announced the release of their AI-powered RPM platform, which uses machine learning for real-time insights into patient data.

- August 2023: Medtronic plc announceds a strategic partnership with BioIntelliSense for exclusive US hospital and 30-day post-acute hospital to home distribution rights of BioButton multi-parameter wearable for continuous, connected monitoring.

- October 2023: Teladoc Health, Inc. announced the launch of their Respiratory Performance Monitor (RPM) program for those living with Chronic Obstructive Pulmonary Disease (COPD). This comprehensive solution includes an interactive inhaler and mobile app which allow patients to monitor symptoms and medication usage.

- November 2022: BioIntelliSense announceds a partnership with Mount Sinai Health System to implement their BioButton wearable for remote heart failure monitoring.

Get a Complete and Professional sample PDF @ https://market.us/report/remote-patient-monitoring-software-and-services-market/request-sample/

Market Segmentation

By Product Type

- Services

- Software

By Application

- Cardiovascular Diseases

- Cancer

- Diabetes

- Neurological Disorders

- Other Applications

By End-User

- Payers

- Patients

- Providers

By Geography

North America

- The US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Browse More Related Reports

- Digital Health Market Size is expected to be worth around USD 1,190.4 Billion by 2032 from USD 264.1 Billion in 2023

- AI In Medical Imaging Market size is expected to be worth around USD 14826.8 Million by 2032

- Smart Healthcare Market was valued at USD 184 billion and is expected to reach around 541 billion in 2032

- Virtual Health Service Market size is expected to be worth around USD 50.9 Billion by 2032

- Healthcare BPO Market size is expected to be worth around USD 908 billion by 2032 from USD 362 billion in 2022

- Artificial Intelligence in Drug Discovery Market was valued at USD 1.2 Billion Between 2023 and 2032

About Us:

Market.US (Powered by Prudour Pvt Ltd) specializes in in-depth market research and analysis and has been proving its mettle as a consulting and customized market research company, apart from being a much sought-after syndicated market research report-providing firm. Market.US provides customization to suit any specific or unique requirement and tailor-makes reports as per request. We go beyond boundaries to take analytics, analysis, study, and outlook to newer heights and broader horizons.

Follow Us on LinkedIn

Our Blog: