Dublin, Nov. 26, 2025 (GLOBE NEWSWIRE) -- The "United States Data Center Construction Market Report by Tier Type, Infrastructure, Vertical, States and Company Analysis, 2025-2033" report has been added to ResearchAndMarkets.com's offering.

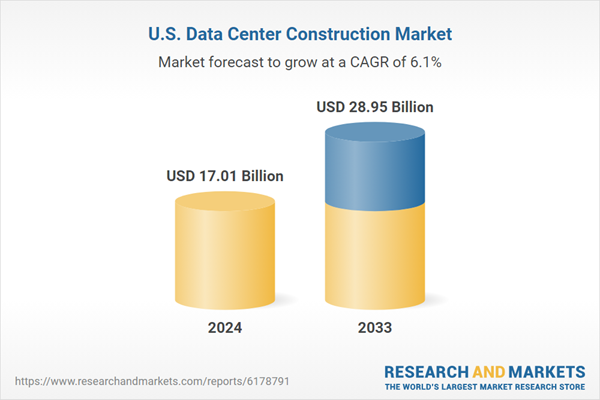

The United States Data Center Construction Market is expected to reach US$ 28.95 billion by 2033 from US$ 17.01 billion in 2024, with a CAGR of 6.09% from 2025 to 2033.

The market for building data centers is expected to grow rapidly due to factors such cloud computing, digital transformation, and rising need for sophisticated facilities that enable high-capacity, scalable, and energy-efficient IT infrastructure. The U.S. data center construction market is concentrated in regions like California, Texas, New York, and Florida, driven by strong digital infrastructure, cloud adoption, energy availability, and government support for technology investments and expansion.

The fast growth of cloud computing, big data analytics, and growing industry digitization are driving the data center construction market in the United States. Businesses and governmental organizations are constantly investing in state-of-the-art infrastructure to accommodate massive data traffic and cutting-edge technologies. The need for scalable, effective, and secure data center infrastructure is being further accelerated by the development of AI, machine learning, and the Internet of Things.

This has made it possible for engineering firms, technology companies, and construction companies to work together to provide cutting-edge facilities that satisfy changing needs. Energy efficiency and sustainability are two key areas of concentration in the US market. Operators are incorporating green building requirements, innovative cooling systems, and renewable energy sources into construction projects as a result of increased awareness of carbon footprints. Additionally, modular data center building is becoming more popular since it provides businesses expanding their operations with flexibility, quick deployment, and cost savings. These developments are turning the market into a center for creative infrastructure deployment and design.

Many important drivers are driving the market, chief among them the growing demand for digital infrastructure across industries. Trends like machine learning (ML), artificial intelligence (AI), the Internet of Things (IoT), and 5G are driving the exponential growth in data generation, which is forcing corporations and hyperscale cloud providers to increase the size of their data centers.

In order to handle their growing workloads, digital behemoths like Google Cloud, Microsoft Azure, and Amazon Web Services are constructing next-generation facilities with high power densities and effective cooling systems. For example, OpenAI, SoftBank, and Oracle formed a joint venture in January 2025 with the goal of investing $100 billion in AI infrastructure; by the conclusion of Trump's second term, the investment might grow to $500 billion. Ten enormous data centers totaling around 500,000 square feet are part of the Stargate project; one is now under construction in Abilene, Texas.

The growing use of edge computing is also fueling the expansion of the US data center building industry since it increases demand for decentralized data centers near consumers for improved performance and reduced latency. Sustainable and energy-efficient building techniques are also being promoted in new facilities by advantageous government regulations, tax breaks, and renewable energy requirements. For example, the US-based real estate company Related Companies formally unveiled a new data center development business in March 2025 with the goal of delivering gigawatts of capacity across the US and Canada. The business announced the opening and financing of Related Digital, a comprehensive platform devoted to infrastructure development and data center investment.

Key Factors Driving the United States Data Center Construction Market Growth

Increasing Cloud Dependency and Data Consumption

A favorable prognosis for the US data center construction market is being created by the rapidly increasing data demand and the growing reliance on digital infrastructure. In 2023, U.S. wireless networks sent a record 100.1 trillion megabytes of data, an 89% increase since 2021, according to CTIA's 2024 Annual Wireless Industry Survey.

This increase emphasizes how important data centers are for organizing, processing, and storing digital information. Simultaneously, scalable and sophisticated data centers that can manage enormous workloads are required due to the quick growth of cloud computing services. Demand for safe, large-capacity, and effective data center facilities nationwide is only going to increase as more and more businesses move their workloads to the cloud.

Industry Investment, Remote Work, and Sustainability Focus

A collective push for sustainable, energy-efficient data centers, fueled by environmental concerns and governmental requirements, is another factor propelling market expansion. Operators are implementing green practices, like employing renewable energy and enhanced cooling systems, in accordance with developments in the US data center construction industry. To address growing infrastructure demands, IT firms are simultaneously making significant investments in new facilities and enlarging old ones.

The market dynamics are still impacted by the move toward remote work. Sixty-eight percent of tech workers work off-site, and roughly 22 million people, or 14% of the US total, now work entirely remotely. The necessity for scalable, robust data centers that can facilitate remote teams, real-time collaboration, and continuous digital operations is highlighted by this continuous change.

Development of IoT, AI, and Technological Advancements

High-performance data centers are in high demand due to the quick development of artificial intelligence (AI), 5G connectivity, and the Internet of Things (IoT). These technologies need a strong computational infrastructure, low latency, and real-time data processing. Through Stargate, a partnership of OpenAI, SoftBank, and Oracle, President Trump unveiled a $500 billion private-sector AI infrastructure effort in January 2025. The proposal calls for the construction of 20 data centers and the creation of 100,000 jobs.

These initiatives greatly speed up market progress by reflecting the increasing demand for hyperscale data center infrastructure to serve smart devices, linked ecosystems, and intelligent applications. Additionally, widespread 5G integration boosts data transmission speeds, driving further need for modern data center capacity.

Challenges in the United States Data Center Construction Market

High Capital Investment and Operational Costs

One of the largest obstacles facing the US market is the significant financial investment needed to construct modern data centers. The expenses are high and include everything from purchasing land and constructing supplies to sophisticated cooling and security systems. The financial burden is further increased by operational costs for staffing, maintenance, and electricity. Competing with hyperscale companies who have easier access to financing presents challenges for smaller businesses and newcomers.

Profitability is also impacted by changes in building expenses, supply chain hold-ups, and growing energy expenditures. High upfront and continuing expenditures continue to be a barrier to wider expansion, even while financing options and strategic alliances help reduce risks. This obstacle frequently limits growth in smaller markets, focusing expansion on places like California and Texas that have developed financial and technology ecosystems.

Regulatory and Compliance Complexities

Strict regulatory regulations and compliance standards provide hurdles for the U.S. data center construction business. State and federal laws pertaining to data security, energy efficiency, land usage, and environmental sustainability must be followed by operators. Construction schedule delays and cost increases are frequently caused by obtaining permits and satisfying compliance deadlines. While federal regulations govern cybersecurity and data protection regimes, states like California enforce strict energy efficiency requirements.

Environmental impact studies and zoning regulations also make project execution more difficult. Data centers contain sensitive data, therefore it's important but expensive to make sure privacy laws and security standards are followed. Compliance is a big issue because of these aspects, which need for extensive planning, specialist knowledge, and cooperation with regulatory agencies. Operators must successfully handle these complications in order to guarantee dependable and legal operations throughout the various U.S. regions.

Recent Developments in U.S. Data Center Construction Market

- In June 2025, Sika revealed clever, long-lasting data center construction solutions, bolstering international investments expected to reach CHF 400 billion by 2028. With more than 1,000 data centers constructed, Sika's solutions provide end-to-end support and enhance sustainability, efficiency, and cooling while capitalizing on the growing demand for cloud computing and artificial intelligence.

- As part of its USD 100 billion AI-focused capital plan for 2025, Amazon stated in June 2025 that it would expand its data center in North Carolina by USD 10 billion. The campus, which consists of 20 buildings, will boost cloud and AI capabilities, promote STEM education and workforce training locally, and generate 500 high-skilled jobs.

- A USD 20 billion U.S. expansion aiming for 2,000MW capacity was announced by EDGNEX Data Centers by DAMAC in January 2025. Depending on demand, the investment is expected to quadruple. The project would expand DAMAC's worldwide digital infrastructure footprint while assisting hyperscalers and the expansion of AI in Sunbelt and Midwest regions.

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 200 |

| Forecast Period | 2024 - 2033 |

| Estimated Market Value (USD) in 2024 | $17.01 Billion |

| Forecasted Market Value (USD) by 2033 | $28.95 Billion |

| Compound Annual Growth Rate | 6.0% |

| Regions Covered | United States |

Company Analysis: Overviews, Key Persons, Recent Developments, SWOT Analysis, Revenue Analysis

- AECOM

- Whiting-turner Contracting Company

- Turner Construction Co.

- Jacobs Solutions Inc.

- DPR Construction

- Skanska USA

- Balfour Beatty US

- Hensel Phelps

Market Segmentations

Tier Type

- Tier 1

- Tier 2

- Tier 3

- Tier 4

Infrastructure

- IT Infrastructure

- Miscellaneous Infrastructure

- PD & Cooling Infrastructure

Vertical

- IT & Telecom

- BFSI

- Healthcare

- Government & Defense

- Energy

- Others

States

- California

- Texas

- New York

- Florida

- Illinois

- Pennsylvania

- Ohio

- Georgia

- New Jersey

- Washington

- North Carolina

- Massachusetts

- Virginia

- Michigan

- Maryland

- Colorado

- Tennessee

- Indiana

- Arizona

- Minnesota

- Wisconsin

- Missouri

- Connecticut

- South Carolina

- Oregon

- Louisiana

- Alabama

- Kentucky

- Rest of United States

For more information about this report visit https://www.researchandmarkets.com/r/tjzmaw

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment