Dublin, Feb. 08, 2024 (GLOBE NEWSWIRE) -- The "Asia-Pacific Heavy-Duty Autonomous Vehicle Market: Analysis and Forecast, 2023-2032" report has been added to ResearchAndMarkets.com's offering.

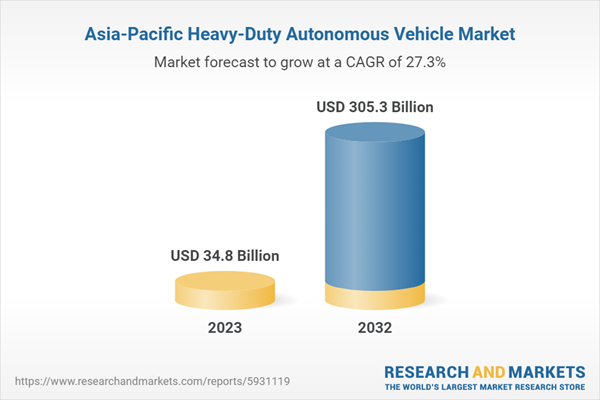

The Asia-Pacific heavy-duty autonomous vehicle market (excluding China) was valued at $34.8 billion in 2023 and is expected to reach $305.3 billion by 2032, growing at a CAGR of 27.28% during the forecast period 2023-2032

The growth of the heavy-duty autonomous vehicle market is anticipated to be fueled by an increasing desire for autonomous driving technology and the ongoing advancements and adoption of heavy-duty autonomous vehicles in public transportation for both semi-autonomous and fully autonomous applications.

The heavy-duty autonomous vehicle market in the Asia-Pacific (APAC) region is still in its nascent stages, characterized by limited commercial deployment and a relatively small number of participants. Its primary focus lies in industrial sectors like mining, construction, and logistics, where there is a notable demand for large, autonomous vehicles capable of operating in challenging environments.

Although the APAC heavy-duty autonomous vehicle market is currently smaller compared to the broader autonomous vehicle market, it is poised for rapid growth in the foreseeable future. Ongoing technological advancements and increasing recognition of the advantages of autonomous operation are driving this growth. In APAC, there is significant interest and investment from various companies vying to establish their presence in this emerging market segment.

How can this report add value to an organization?

Product/Innovation Strategy:

The leading autonomous vehicle OEMs are continuously working to manufacture and sell vehicles with higher autonomous driving capabilities, i.e., level 3 and above. The growing need for affordable and high-performing heavy-duty autonomous vehicles is one of the major factors for the growth of the heavy-duty autonomous vehicle market.

The market is more on the consolidated side at present, where heavy-duty autonomous vehicle manufacturers have been successful to a certain extent in strengthening their market position in the market, with a few autonomous vehicle OEMs and autonomous vehicle technology providers working on such solutions in-house.

However, with the rise of autonomous driving, the existing established players are expected to face stiff competition from emerging players. Moreover, partnerships and collaborations are expected to play a crucial role in strengthening market position over the coming years, with the companies focusing on bolstering their technological capabilities and gaining a dominant market share in the heavy-duty autonomous vehicle industry.

Growth/Marketing Strategy:

The APAC heavy-duty autonomous vehicle market has been growing at a rapid pace. The market offers enormous opportunities for existing and emerging market players. Some of the strategies covered in this segment are mergers and acquisitions, product launches, partnerships and collaborations, business expansions, and investments. The strategies preferred by companies to maintain and strengthen their market position primarily include partnerships, agreements, and collaborations.

Competitive Strategy:

The key players in the APAC heavy-duty autonomous vehicle market analyzed and profiled in the study include multiple vehicle type manufacturers, bus manufacturers, truck manufacturers, roboshuttle manufacturers, and autonomous vehicle technology providers that develop, maintain, and market heavy-duty autonomous vehicles.

Moreover, a detailed competitive benchmarking of the players operating in the APAC heavy-duty autonomous vehicle market has been done to help the reader understand the ways in which players stack against each other, presenting a clear market landscape. Additionally, comprehensive competitive strategies such as partnerships, agreements, and collaborations are expected to aid the reader in understanding the untapped revenue pockets in the market.

Market Segmentation:

Application

- Logistics

- Public Transportation

- Construction and Mining

- Others

Propulsion Type

- Internal Combustion Engine Vehicles

- Electric Vehicles

Vehicle Type

- Heavy Trucks

- Heavy Buses

- Roboshuttles

Level of Autonomy

- Semi-Autonomous Vehicles

- Autonomous Vehicles

Sensor Type

- LiDAR

- RADAR

- Camera

- Others

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 132 |

| Forecast Period | 2023 - 2032 |

| Estimated Market Value (USD) in 2023 | $34.8 Billion |

| Forecasted Market Value (USD) by 2032 | $305.3 Billion |

| Compound Annual Growth Rate | 27.2% |

| Regions Covered | Asia Pacific |

Key Topics Covered:

Executive Summary

Scope of the Study

1 Markets

1.1 Industry Outlook

1.1.1 Trends: Current and Future

1.1.1.1 Electrification and Automation of Commercial Vehicles

1.1.1.2 Rising Awareness about Autonomous Vehicles

1.1.2 Advance Driver Assistance System (ADAS)

1.1.2.1 Overview

1.1.2.2 ADAS Features

1.1.3 Ecosystem of Autonomous Driving

1.1.4 Supply Chain Analysis

1.1.5 Regulatory Landscape

1.1.5.1 Current Laws and Regulatory Bodies

1.1.5.2 Current Laws and Regulatory Bodies Related to Testing and Experimentation of Autonomous Vehicles (by Country)

1.1.6 Ecosystem/Ongoing Programs

1.1.6.1 Consortiums, Associations, and Regulatory Bodies

1.1.6.2 Programs by Research Institutions and Universities

1.1.7 Key Patent Mapping

1.1.7.1 Analyst View

1.1.8 Startup Landscape

1.2 Business Dynamics

1.2.1 Business Drivers

1.2.1.1 Development of Regulations for Autonomous Mobility

1.2.1.2 Rising Developments and Integration of Autonomous Buses in Public Transport

1.2.1.3 Developments of High-Tech Autonomous Solutions for Commercial Vehicles

1.2.2 Business Restraints

1.2.2.1 High Cost and Rising Price Volatility of Hardware Components

1.2.2.2 Semiconductor Shortage Effect

1.2.3 Business Strategies

1.2.3.1 Market Development

1.2.3.2 Product Development

1.2.4 Corporate Strategies

1.2.4.1 Mergers and Acquisitions

1.2.4.2 Partnerships, Collaborations, and Joint Ventures

1.2.5 Business Opportunities

1.2.5.1 Advantages Offered by Commercial Autonomous Vehicles to Logistics Industry

1.2.5.2 Emerging Adoption of Roboshuttle

1.3 Impact of COVID-19 on the Industry

2 Regions

2.1 China

2.1.1 Market

2.1.1.1 Buyer Attributes

2.1.1.2 Key Manufacturers in China

2.1.1.3 Competitive Benchmarking

2.1.1.3.1 Conventional Heavy-Duty Vehicles

2.1.1.3.2 Autonomous Heavy-Duty Vehicles

2.1.1.4 Business Challenges

2.1.1.5 Business Drivers

2.1.2 Applications

2.1.3 Products

2.2 Asia-Pacific and Japan

2.2.1 Market

2.2.1.1 Buyer Attributes

2.2.1.2 Key Manufacturers in Asia-Pacific and Japan

2.2.1.3 Competitive Benchmarking

2.2.1.3.1 Conventional Heavy-Duty Vehicles

2.2.1.3.2 Autonomous Heavy-Duty Vehicles

2.2.1.4 Business Challenges

2.2.1.5 Business Drivers

2.2.2 Applications

2.2.3 Products

2.2.4 Asia-Pacific and Japan: Country-Level Analysis

3 Markets - Competitive Benchmarking & Company Profiles

3.1 Competitive Benchmarking

3.1.1 Competitive Position Matrix

3.1.1.1 Conventional Heavy-Duty Vehicles

3.1.1.2 Autonomous Heavy-Duty Vehicles

3.2 Market Share Snapshot

3.3 Company Profiles

3.3.1 Type 1 Companies: Multiple Vehicle Type Manufacturers

3.3.1.1 Shanghai Newrizon Technology Co., Ltd.

3.3.1.1.1 Company Overview

3.3.1.1.1.1 Role of Shanghai Newrizon Technology Co., Ltd. in the Heavy-Duty Autonomous Vehicle Market

3.3.1.1.1.2 Product Portfolio

3.3.1.1.2 Business Strategies

3.3.1.1.2.1 Product Development

3.3.1.1.2.2 Market Development

3.3.1.1.3 Analyst View

3.3.2 Type 4 Companies: Roboshuttle Manufacturers

3.3.2.1 Apollo (Baidu)

3.3.2.1.1 Company Overview

3.3.2.1.1.1 Role of Apollo (Baidu) in the Heavy-Duty Autonomous Vehicle Market

3.3.2.1.1.2 Product Portfolio

3.3.2.1.2 Analyst View

4 Research Methodology

For more information about this report visit https://www.researchandmarkets.com/r/g3a6j8

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment