Dublin, Feb. 09, 2024 (GLOBE NEWSWIRE) -- The "Global Telehealth & Telemedicine Market by Component (Software & Services (RPM, Real-Time), Hardware (Monitors)), Delivery (On-Premise, Cloud-based), Application (Teleradiology, Telestroke, TelelCU), End-user (Provider, Payer) & Region - Forecast to 2028" report has been added to ResearchAndMarkets.com's offering.

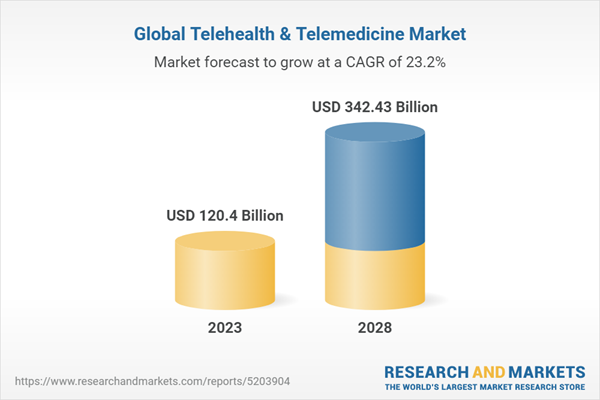

The global Telehealth and Telemedicine market is projected to reach USD 342.43 billion by 2028 from USD 120.4 billion in 2023, at a CAGR of 23.2% during the forecast period. The growth of telemedicine and telehealth is propelled by increased accessibility to healthcare services, especially in remote areas, and continuous technological advancements, such as improved connectivity and enhanced platforms, fostering better patient engagement and outcomes.

The report analyzes the Telehealth and Telemedicine Market and aims to estimate the market size and future growth potential of various market segments, based on components, mode of delivery, application, end-user, and region. The report also provides a competitive analysis of the key players operating in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Cloud-based delivery mode segment accounted for a substantial share of the Telehealth and Telemedicine market, by delivery mode in 2022

The cloud-based delivery mode is expected to account for the largest share of 78.2% of the global telehealth and telemedicine market in 2022. It is projected to grow at the highest CAGR of 28.6 % during the forecast period. Cloud-based delivery dominates the telehealth and telemedicine market due to its inherent advantages. The accessibility and scalability offered by cloud solutions enable healthcare services from virtually anywhere, bridging gaps in remote or underserved areas.

Cost efficiency is heightened through subscription-based models, making these platforms attractive for organizations with budget constraints. Robust security measures, compliance standards, and seamless interoperability make cloud environments secure repositories for sensitive patient data. Real-time collaboration, remote monitoring capabilities, and rapid deployment further enhance the effectiveness of telehealth services. Additionally, cloud platforms ensure quick updates, disaster recovery, and business continuity, collectively driving their widespread adoption in the evolving landscape of healthcare delivery.

Software and service segment accounted for a substantial share of the Telehealth and Telemedicine market, by component in 2022

Based on components, the software & services segment is expected to account for the largest share of 71.3% of the global telehealth and telemedicine market in 2022. The software and services segment holds a significant share as a component in the telehealth and telemedicine market. This prominence is driven by the crucial role that software applications and associated services play in facilitating remote healthcare delivery. Telehealth platforms rely heavily on advanced software solutions to enable virtual consultations, patient monitoring, and seamless data exchange.

Additionally, the provision of supportive services such as telemedicine consultation support, data analytics, and integration services further solidifies the importance of the software and services component. As the telehealth and telemedicine landscape continues to evolve, the software and services segment remains a cornerstone, contributing substantially to the market's growth and efficacy.

Providers segment accounted for a considerable share in the Telehealth and Telemedicine market, by end-user in 2022

In 2022, the provider segment played a significant role in the telehealth and telemedicine market, contributing to a substantial share. This prominence is attributed to This is attributed to the increased adoption of remote monitoring for chronically ill and old aged patients, advancements in telehealth monitoring devices, and the increased number of telespecialty services offered by providers.

Teleradiology segment accounted for the largest share in Telehealth and Telemedicine market by Application in 2022

In 2022, teleradiology segment emerged as the leading contributor to the Telehealth and Telemedicine market, holding the largest share. Factors such as an increase in imaging practices, an increase in teleradiology workflow adoption by healthcare providers, and the streamlining and regulation of teleradiology practices are driving the market growth. The teleradiology segment is expected to account for the largest share of 22.2% of the global telehealth and telemedicine market in 2022.

North America to witness the substantial growth rate during the forecast period

The global market is led by the United States, experiencing a noteworthy CAGR of 24.3% and reaching a valuation of US$ 289.7 billion in the forecast period. The surge is propelled by factors such as the prevalence of chronic diseases, an aging population, and cost-effective healthcare services, contributing to the growth of telehealth and telemedicine in the United States.

The market sees continuous expansion due to increased healthcare infrastructure, expenditures, and innovative technologies. Government initiatives and the active involvement of key vendors further amplify market size, marking a substantial increase from the historical CAGR of 24.3% between 2023 and 2028.

Key Attributes

| Report Attribute | Details |

| No. of Pages | 232 |

| Forecast Period | 2023-2028 |

| Estimated Market Value (USD) in 2023 | $120.4 Billion |

| Forecasted Market Value (USD) by 2028 | $342.43 Billion |

| Compound Annual Growth Rate | 23.2% |

| Regions Covered | Global |

Market Dynamics

- Drivers

- Growing Geriatric Population and Increasing Need to Expand Healthcare Access

- Rising Prevalence of Chronic Conditions and Cost-Benefits of Telehealth & Telemedicine Services

- Shortage of Skilled Healthcare Professionals

- Advancements in Telecommunication Technologies

- Increased Government Support and Favorable Reimbursement Policies

- Restraints

- Regulatory Variations Across Regions

- Increase in Fraud in Telehealth Practices

- Violation of Medical Ethics

- Opportunities

- Increased Utility of Telemedicine Against Infectious Diseases and Epidemics

- Use of Blockchain Technology in Healthcare Industry

- Increased Use of Artificial Intelligence and Big Data Analytics

- Growing Demand for Virtual Care

- Challenges

- Inability to Maintain Hygiene and Cleanliness Standards

- Behavioral Barriers, Healthcare Affordability, and Lack of Awareness

Technology Analysis

- Machine Learning

- Artificial Intelligence

- Internet of Things

- Blockchain Technology

- Cloud Computing

- Data Analytics

- Extended Reality

Pricing Analysis

- Costs Involved in Telemedicine Devices

- Average Selling Price for Telehealth & Telemedicine Devices, by Key Player

- Indicative Pricing Analysis of Telehealth & Telemedicine Devices, by Region

- Pricing Models

Companies Mentioned

- ACL Digital

- AMC Health

- American Well

- Asahi Kasei Corporation

- Boston Scientific Cardiac Diagnostics Inc.

- Cisco Systems, Inc.

- Doctor on Demand, Inc.

- Evernorth Health, Inc.

- GE Healthcare

- Global Media Group LLC

- iCliniQ

- iMedi Plus

- Iron Bow Technologies

- Koninklijke Philips N.V.

- Medtronic

- Medvivo Group Ltd.

- Medweb

- Oracle

- Resideo Life Care Solutions

- Siemens Healthineers AG

- Teladoc Health, Inc.

- Telespecialists

- VSee

- Zipnosis

For more information about this report visit https://www.researchandmarkets.com/r/lmwmvv

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment