Dublin, March 22, 2024 (GLOBE NEWSWIRE) -- The "Carbon Management Software Market by Component (Software, Services), Application (Energy, Greenhouse Gas Management, Air Quality Management, Sustainability), Industry (Manufacturing, IT and Telecom, Government Sector, Energy and Power, and Others), and Region 2024-2032" report has been added to ResearchAndMarkets.com's offering.

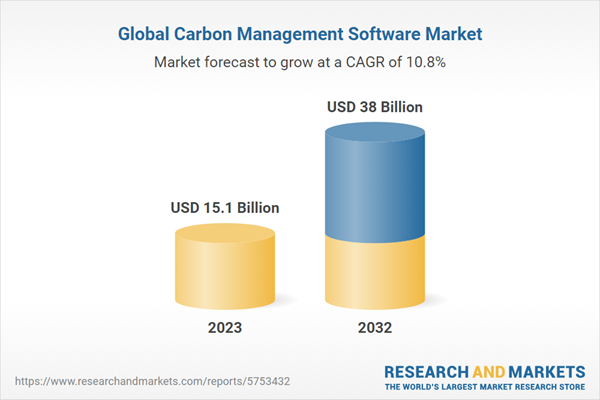

The global carbon management software market size reached US$ 15.1 billion in 2023. The market is projected to reach US$ 38 billion by 2032, exhibiting a growth rate (CAGR) of 10.82% during 2023-2032. The market is experiencing steady growth driven by increasing regulatory pressures and a growing global commitment to sustainability, the rising awareness of carbon footprints and the need for compliance with environmental regulations, and the escalating demand for transparency in sustainability efforts from stakeholders.

Increasing regulatory compliance and carbon footprint concerns

A significant driver of the global market is the growing need for regulatory compliance. Governments worldwide are imposing stringent regulations to mitigate climate change, leading to increased demand for tools that enable organizations to monitor and report their carbon emissions accurately. This software helps businesses comply with these regulations, avoid potential fines, and maintain a positive public image by demonstrating environmental responsibility. Additionally, with the rising awareness of carbon footprints, companies are increasingly adopting software to analyze, track, and report their emissions, thereby contributing to global sustainability efforts. The software's ability to provide detailed insights into carbon emissions helps businesses identify areas for improvement, thus facilitating the development of more effective strategies for carbon reduction.

Advancements in technology and integration capabilities

Technological advancements are a major factor propelling the growth of the market. Additionally, the integration of advanced technologies such as artificial intelligence (AI), machine learning, and the Internet of Things (IoT) is enhancing the capabilities of the software. These technologies enable more accurate and efficient analysis of large volumes of emission data, facilitating better decision-making for carbon reduction strategies. Furthermore, the integration of the software with existing business systems and processes has become easier, encouraging its adoption across various industries. This integration allows for seamless data flow and analysis, leading to more cohesive and comprehensive carbon management strategies. The software's ability to adapt and scale according to the business size and sector is also a key factor in its widespread adoption, as it provides customized solutions catering to specific industry needs and compliance requirements.

Corporate sustainability commitments and stakeholder pressure

The increasing focus on corporate sustainability and the pressure from stakeholders, including investors, customers, and employees, is another major driver of the market. Companies are recognizing the importance of reducing their environmental impact as part of their corporate social responsibility. This shift in corporate culture towards sustainability is leading to the adoption of the software as a tool to achieve and showcase these commitments. The software helps in monitoring and reducing emissions and in reporting these efforts transparently to stakeholders. This transparency is crucial as it builds trust and enhances the company's reputation, potentially leading to increased customer loyalty, investor confidence, and market competitiveness. In addition, employees are increasingly seeking to work for environmentally responsible companies, making carbon management a key aspect of attracting and retaining top talent.

Carbon Management Software Industry Segmentation:

The report provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2023-2032. The report has categorized the market based on component, application, and industry.

Breakup by Component:

- Software

- Services

Software accounts for the majority of the market share

The software component of the market is the largest and most significant segment. This segment encompasses various software solutions designed to monitor, analyze, and manage carbon emissions. These tools are integral for companies to accurately track their carbon footprint, ensuring compliance with environmental regulations and aiding in the development of strategies for carbon reduction. The software often incorporates advanced technologies such as AI and IoT, enhancing its efficiency and accuracy. Its scalability and adaptability to different industry needs make it a versatile tool for businesses of all sizes. Additionally, the demand for software solutions is particularly high in industries with complex operations and significant emissions, such as manufacturing, energy, and transportation.

On the other hand, the services segment of the market, while smaller than the software segment, plays a crucial role in the effective implementation and utilization of carbon management solutions. This segment includes various services such as consulting, implementation, maintenance, and support. Consulting services are essential for businesses to understand their carbon management needs and to devise effective strategies. Implementation services ensure that the software is integrated seamlessly with existing business systems, while maintenance and support services are vital for the ongoing effectiveness of the software. Moreover, the demand for these services is driven by the complexity of carbon management tasks and the need for expertise in software deployment and utilization.

Breakup by Application:

- Energy

- Greenhouse Gas Management

- Air Quality Management

- Sustainability

Energy holds the largest share in the industry

In the market, the energy segment emerges as the largest due to its critical role in carbon emissions and management. This segment primarily focuses on monitoring and reducing carbon emissions in the energy production and consumption process. With the global inclination towards renewable energy and sustainable practices, energy companies are increasingly adopting the software to optimize energy use, reduce emissions, and comply with environmental regulations. Additionally, the software aids in tracking and analyzing energy consumption patterns, identifying areas for improvement, and implementing energy-efficient practices.

On the contrary, greenhouse gas management segment is dedicated to the tracking, analysis, and management of greenhouse gas (GHG) emissions. It is critical for organizations aiming to reduce their environmental impact and comply with global GHG reduction targets. The software in this segment helps businesses accurately measure their GHG emissions, identify sources, and develop strategies to reduce these emissions. It is particularly relevant for industries with significant GHG emissions, such as manufacturing, agriculture, and transportation. The growing global emphasis on reducing GHG emissions to combat climate change is a key factor driving the demand in this segment.

Moreover, the air quality management segment focuses on monitoring and managing the impact of business activities on air quality. This segment is gaining importance due to increasing environmental concerns and stringent regulations regarding air pollutants. The software in this segment helps organizations track emissions of various air pollutants, assess their impact on air quality, and devise strategies to minimize this impact. It is crucial for industries that emit particulates and gases affecting air quality, such as chemical manufacturing, mining, and construction.

Furthermore, in the sustainability segment, it is used to support overall sustainability initiatives within organizations. This segment encompasses a broader range of activities beyond carbon and GHG emissions, including waste management, water usage, and sustainable resource utilization. The software aids in integrating sustainability goals into business operations, tracking progress, and reporting on sustainability efforts. This segment is increasingly relevant as more companies commit to comprehensive sustainability agendas, driven by stakeholder pressure and a global shift towards sustainable business practices.

Breakup by Industry:

- Manufacturing

- IT and Telecom

- Government Sector

- Energy and Power

- Others

Manufacturing represents the leading market segment

The manufacturing segment is the largest in the market, primarily due to the significant carbon emissions and energy consumption associated with manufacturing processes. In this sector, the software is crucial for monitoring and reducing emissions, optimizing energy usage, and ensuring compliance with environmental regulations. The diverse range of manufacturing industries, from automotive to chemicals, all require tailored solutions to manage their specific emission profiles. As manufacturers increasingly focus on sustainability and reducing their environmental impact, the demand for effective carbon management solutions in this segment continues to grow, driven by both regulatory pressures and corporate social responsibility initiatives.

On the other hand, in the IT and telecom segment, the software is used to monitor and manage the carbon footprint of data centers, network operations, and office environments. This sector faces unique challenges due to the high energy demands of data centers and the need for continuous operation. The software helps in optimizing energy efficiency, reducing emissions, and achieving sustainability goals. With the rapid growth of digital technologies and the increasing focus on green IT practices, this segment is seeing a growing demand for carbon management solutions.

Additionally, the government sector uses the software to meet regulatory requirements and lead by example in environmental stewardship. This segment encompasses a wide range of government operations, including municipal services, public transportation, and government buildings. The software aids in tracking and reporting emissions, setting reduction targets, and implementing policies for sustainable practices. Governments are increasingly adopting these solutions to demonstrate leadership in tackling climate change and to meet national and international environmental commitments.

Furthermore, in the energy and power segment, the software is essential for tracking emissions from energy production and distribution. This includes both renewable and non-renewable energy sources. The software is crucial for managing the carbon footprint of power plants, optimizing energy production processes, and transitioning towards cleaner energy sources. With the global shift towards renewable energy and the need to reduce emissions from fossil fuels, this segment is focusing on adopting advanced carbon management solutions to meet these challenges.

Moreover, the 'others' segment includes a variety of industries such as healthcare, retail, and transportation that are increasingly adopting the software. These industries are integrating carbon management into their operations to reduce their environmental impact, improve sustainability, and comply with the changing regulations. Each industry within this segment has unique requirements and faces different challenges in managing its carbon footprint, driving the demand for versatile and adaptable carbon management solutions.

Breakup by Region:

- North America

- Asia-Pacific

- Europe

- Latin America

- Middle East and Africa

North America leads the market, accounting for the largest carbon management software market share

North America leads the market, largely due to stringent environmental regulations and high awareness of sustainability issues in the region. The United States and Canada are at the forefront, with numerous industries adopting carbon management practices to comply with regulatory standards and corporate sustainability goals. Additionally, the presence of major market players and technological innovators in this region also contributes to its dominance. Furthermore, the increasing adoption of renewable energy sources and the shift towards greener practices in sectors such as manufacturing and transportation are driving the demand for carbon management solutions in North America.

Concurrently, the Asia-Pacific region is experiencing rapid growth in the market. This growth is driven by increasing industrialization, rising awareness of environmental issues, and the implementation of strict environmental regulations in countries such as China, India, and Japan. The region's focus on sustainable development, particularly in emerging economies, is leading to a higher adoption of carbon management solutions.

In addition, Europe is a significant market, characterized by advanced environmental policies and a strong focus on reducing carbon emissions. The European Union's commitment to the Paris Agreement and its own ambitious climate goals have led to the widespread adoption of carbon management practices across various industries. European countries are also leading in terms of technological advancements and innovations in the software, further providing a boost to the market growth in this region.

Apart from this, the Latin America region, while a smaller segment in the global market, is showing signs of growth. Factors contributing to this growth include increasing environmental awareness, government initiatives for sustainable development, and the gradual adoption of green technologies. Countries such as Brazil, Mexico, and Argentina are gradually incorporating carbon management practices in sectors such as energy, manufacturing, and transportation, which is expected to drive market growth in the region.

Moreover, the Middle East and Africa region is emerging in the market. The market growth in this region is driven by the increasing need for energy management and environmental conservation, particularly in oil-rich countries looking to diversify their economies and reduce carbon emissions. Initiatives for sustainable development and the adoption of renewable energy sources are also contributing factors.

Leading Key Players in the Carbon Management Software Industry

The key players in the market are actively engaged in various strategic activities to strengthen their market positions. These include technological innovations, collaborations with other companies, and expanding their service offerings to meet the diverse needs of different industries. Many are focusing on integrating advanced technologies such as AI, machine learning, and IoT to enhance the accuracy and efficiency of their software. Additionally, these companies are forming partnerships with governmental and non-governmental organizations to align with global sustainability goals. In addition, they are also investing in research and development to create more user-friendly and adaptable solutions, catering to the rising demands of businesses striving for sustainability. These efforts drive their growth and significantly contribute to the overall development and sophistication of the market.

Competitive Analysis

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- ENGIE Impact

- GreenStep Solutions Inc.

- Greenstone+ Ltd.

- Metrix Software Solutions (Pty) Ltd.

- Salesforce Inc.

- SAP SE

- Sphera Solutions Inc.

- Wolters Kluwer N.V.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News:

- December 11, 2023: GreenStep Solutions Inc. announced that it has joined the GreenStep EcoFund Verified Programme, marking the next phase of its commitment to sustainability.

- September 13, 2023: Salesforce Inc. revealed AI technology, the next generation of Einstein. Within the Einstein Trust Layer, Einstein Copilot and Einstein Copilot Studio will function.

- June 22, 2023: ENGIE Impact, Posco, PTTEP and Samsung amongst partners for Oman's $7 billion green hydrogen project. As part of Hydrom Phase A Round 1 request for proposals, the consortium was given the 340-square-kilometer onshore concession Z1-02 in Duqm; downstream components of the proposed hydrogen project will be constructed at the Port of Duqm.

Key Attributes

| Report Attribute | Details |

| No. of Pages | 141 |

| Forecast Period | 2023-2032 |

| Estimated Market Value (USD) in 2023 | $15.1 Billion |

| Forecasted Market Value (USD) by 2032 | $38 Billion |

| Compound Annual Growth Rate | 10.8% |

| Regions Covered | Global |

For more information about this report visit https://www.researchandmarkets.com/r/u8o081

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment