TRUCKEE, CA--(Marketwire - Aug 4, 2011) - Clear Capital (www.clearcapital.com) released its monthly Home Data Index™ (HDI) Market Report, with news of U.S. home price gains of 4.1 percent comparing the most recent rolling quarter to the previous one. Recent gains off the record low in home prices experienced this past winter have not been enough to change the broader housing picture, which remains down 7.9 percent since June 2010, and down 1.8 percent from June 2009.

This month's HDI Market Report provides the highest levels of current data available (through July 2011), and includes relevant analysis of how local markets perform compared to trend data at the national level. Clear Capital uses patent pending rolling quarter intervals to compare the most recent four months of home pricing data to the previous three months. We include the most current fourth month of pricing data, because it contains the most relevant and insightful information.

Report highlights include:

- Northeast markets buck trend of year-over-year price declines, with the broader New York City area, Rochester and Pittsburgh posting positive year-over-year price growth.

- All four U.S. regions (Midwest 6.3%, Northeast 5.2%, South 4.2%, West 0.7%) post quarterly gains without any tax credit stimulus for the first time since 2006.

- REO saturation rates have leveled off, but more than one-in-four home sales across the country remain distressed.

- The inverse correlation between distressed sales activity and home prices continues to depress the market.

"Building off last month's minimal quarterly gains, prices continue to correct from winter's extended declines," said Dr. Alex Villacorta, director of research and analytics at Clear Capital. "Although this is encouraging, many markets are still near, or at record lows as REO saturation remains a significant proportion of all sales activity."

Quarterly Prices Rising Across the Nation, Yearly Declines Continue

- U.S. quarter-over-quarter home prices post 4.1% gains off 2011 winter lows.

- All four regions still experiencing yearly declines. The Midwest was hit the hardest, experiencing a -13.1% price change.

- The national REO saturation rate (28.0%) continues to improve, down 5.7 percentage points from last quarter.

The gains of 4.1 percent reported in this report are improving upon last month's 0.9 percent rolling quarter uptick. This second consecutive month of price gains is encouraging because it has allowed markets to recover most of the losses experienced in the first quarter of 2011(prices still down 1.0% since January), and occurred without the aid any of the federal incentives like those provided in 2009 and 2010. The West region still lags behind the others, posting a meager 0.7 percent price change quarter over quarter.

Year-over-year home prices are mired in negative territory off last year's tax credit highs, with three out of the four regions (West, Midwest, and South) posting year-over-year price declines greater than -7.3 percent. The Northeast region continues to show the most signs of stability, posting a relatively small yearly overall decline of -2.9 percent. Led by the steady gains in the broader New York City area, Rochester, and Pittsburgh, the Northeast was also the only region to turn in a positive six month-over-six month price change (1.6%).

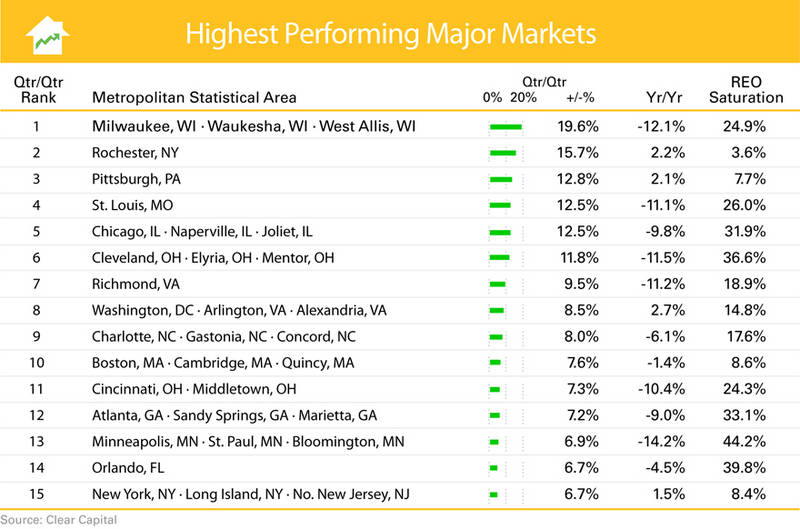

Strongest 15 Markets Show Healthy Quarterly Gains

- Springtime home buying has resulted in quarterly gains for all markets, but 11 of the 15 highest performing markets still experienced yearly declines.

- REO saturation falls to 22.7% on average in the top 15 markets.

Driven by stronger spring and early summer sales, all quarterly prices are up significantly among the highest performing markets compared to the slower winter buying season. The markets of Milwaukee, Rochester and Pittsburgh posted the strongest quarterly gains on seasonal influences.

When comparing the REO saturation of these three high performing metro markets, we find inconsistencies. Contrary to Milwaukee's strong quarterly gains, this market stands out with a relatively high REO saturation rate of 24.9 percent, and -12.1 percent price change for the year. The quarterly gains can be attributed to a large seasonal shift in REO saturation, which dropped 12.4 percentage points this rolling quarter. Further, the Milwaukee market has experienced a 43 percent decline in prices since the national peak in mid-2006, and is still looking to stabilize.

Rochester and Pittsburgh are in better positions, both in terms of current distressed activity and longer-term price performance. These two markets have historically seen higher price stability overall, which helped them avoid the speculative price run-up during the pre-2006 period. From 2000 through the national peak in mid 2006, home prices in Rochester and Pittsburgh gained 24.1 percent and 28.4 percent respectively -- one-third of the 78.9 percent gain seen at the national level during the same period. As a result, these markets have seen lower REO saturation levels that have led to these markets extended gains over the last few years. Rochester is now 7.8 percent above its 2006 mark, while Pittsburgh is up 3.1 percent.

While REO saturation as a whole continued to be significant in highest performing markets, the average saturation rate fell to 22.7 percent, a three percent decline from last month. Rochester, Pittsburgh, Boston and New York led the way, posting single digit rates of REO saturation.

High REO Saturation Continues to Slow Lowest Performing Markets

- All 15 markets maintained prices below their levels from one year ago.

- Average REO saturation rate of 33.3% in the lowest performing markets is 10.6 percent higher than those in the highest performing markets.

- Detroit's quarterly and yearly declines, and very high REO saturation rate keep it the lowest ranked market.

Elevated distressed home sale activity continues to take a toll on the lowest performing markets across the country. Despite an average decline of 3.3 percent in REO saturation from last month, the rate of 33.3 percent remains ten percentage points higher than the highest performing markets. The fallout is fully evident in the table above as not a single market posted quarter-over-quarter gains greater than two percent, and all 15 markets posted year-over-year declines.

On a more positive note, with the exception of Detroit, REO saturation decreased among all the lowest performing markets. Prices, while still down for the year, have also slowed their decline. More than half of these lowest performing markets now maintain single digit yearly declines, which reflect a modest improvement as a whole.

Overall Housing Market Defined by Distressed Sales Activities

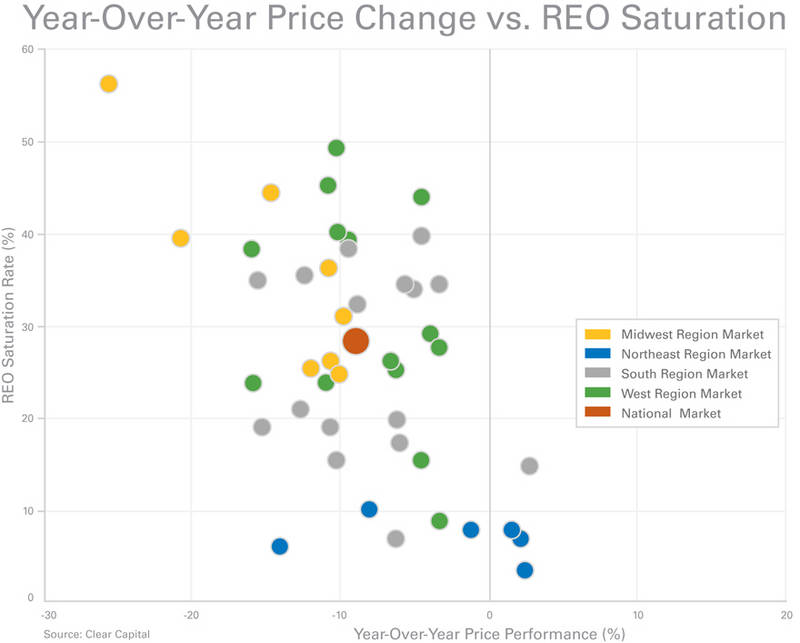

As we analyze this month's highest and lowest performing markets, we continue to see a strong correlation between REO saturation and home prices across the nation. The higher the REO saturation rate for a given market grows, the lower overall home prices fall. This negative correlation between the level of distressed sale activity and home prices has been consistent in nearly every market around the country.

Clear Capital research has shown that this relationship holds with respect to the rate at which REO saturation changes as opposed to its actual magnitude. For example, in this latest report, the Detroit market has an REO saturation rate that is 17 percentage points above Columbus's 39.1 percent. Although Columbus appears to be in better shape, over the past year both Columbus and Detroit's REO saturation rates increased by about 25 percent. While the magnitudes of the REO saturation in both markets differ considerably, the rate of growth has been very similar leading to yearly declines in both markets of roughly the same magnitude (-21.6% in Columbus and -24.3% in Detroit).

Similarly in the top performing markets we've observed the opposite side of the spectrum. Of all the highest performing major markets this month, six of them had decreases in their REO saturation over this past year. And if you look closely at those six markets (Rochester, Pittsburgh, Washington, D.C., Boston, New York, and Orlando), four returned positive yearly price changes while the other two posed the smallest yearly declines on the highest performing list.

The relationship between REO saturation and overall market prices can be best characterized by the discount that is experienced with these distressed properties. As the REO saturation rate increases, the overall market value, which includes non-distressed sales, is weighed down by REO sales used as comparables. With more bank-owned property sales taking place, fair market sellers are forced to actively compete with homes that have significant discounts applied. As this competition increases, through an increased saturation rate, overall market prices come down. Further, when you graph them together, you see a clear linear relationship between REO saturation and year-over-year price change.

When price change and REO saturation are graphed within major markets, clear evidence ties market performance to distressed sale levels. Economic fundamentals have been re-defined in this post crash marketplace to not only include the traditional measures such as employment and consumer confidence, but also the inescapable presence of distressed activity which is defining many of the markets. Here, distressed activity has formed a divide that separates markets.

About the Clear Capital Home Data Index (HDI) Market Report

The Clear Capital HDI Market Report provides insights into market trends and other leading indices for the real estate market at the national and local levels. A critical difference in the value of the HDI Market Report is the capability of Clear Capital to provide more timely and granular reporting than other home price index providers.

The Clear Capital HDI Market Report:

- Offers the real estate industry (investors, lenders and servicers), government agencies and the public insight into the most recent pricing conditions, not only at the national and metropolitan level, but within local markets as well.

- Is built on the most recent information available from recorder/assessor offices, and then further enhanced by adding the company's proprietary streaming market data for the most comprehensive geographic coverage and local insights available.

- Reflects nationwide coverage of sales transactions and aggregates this comprehensive dataset at ten different geographic levels, including hundreds of metropolitan statistical areas (MSAs) and sub-ZIP code boundaries.

- Includes equally-weighted distressed bank owned sales (REOs) from around the country to give the most real world look of pricing dynamics across all sales types.

- Allows for the most current market data by providing more frequent updates with patent-pending rolling quarter technology. This ensures decisions are based on the most up-to-date information available.

Clear Capital Home Data Index™ Methodology

- Generates the timeliest indices in patent pending rolling quarter intervals that compare the most recent four months to the previous three months. The rolling quarters can start date on any date, so the HDI can generate indices as data flows in, significantly reducing the multi-month lag time experienced with other indices.

- Includes both fair market and institutional (real estate owned) transactions, giving equal weight to all market transactions and identifying price tiers at a market specific level. By giving equal weight to all transactions the HDI is truly representative of each unique market.

- Results from an address-level cascade create an index with the most granular, statistically significant market area available.

- Provides weighted repeat sales, and price-per-square-foot index models that use multiple sale types, including single-family homes, multi-family homes and condominiums.

About Clear Capital

Clear Capital (www.clearcapital.com) is a premium provider of data and solutions for real estate asset valuation and risk assessment for large financial services companies. Our products include appraisals, broker-price opinions, property condition inspections, value reconciliations, and home data indices. Clear Capital's combination of progressive technology, high caliber in-house staff and a well-trained network of more than 40,000 field experts sets a new standard for accurate, up-to-date and well documented valuation data and assessments. The Company's customers include the largest U.S. banks, investment firms and other financial organizations.

Legend

Address Level Cascade -- Provides the most granular market data available. From the subject property, progressively steps out from the smallest market to larger markets until data density and statistical confidence are sufficient to return a market trend.

Home Data Index (HDI) -- Powerful analytics tool that provides contextual data augmenting other, human-based valuation tools. Clear Capital's multi-model approach combines address-level accuracy with the most current proprietary home pricing data available.

Metropolitan Statistical Area (MSA) -- Geographic entities defined by the U.S. Office of Management and Budget (OMB) for use by Federal statistical agencies in collecting, tabulating, and publishing Federal statistics.

Repeat Sales Model -- Weighted linear model based on repeat sales of same property over time.

Price Per Square Foot (PPSF) Model -- Median price movement of sale prices divided by square footage over a period of time -- most commonly a quarter.

Real Estate Owned (REO) Saturation -- Calculates the percentage of REOs sold as compared to all properties sold in the last rolling quarter.

Rolling Quarters -- Clear Capital uses patent pending rolling quarter intervals to compare the most recent four months of home pricing data to the previous three months. We include the most current fourth month of pricing data, because it often contains the most relevant information.

The information contained in this report is based on sources that are deemed to be reliable; however no representation or warranty is made as to the accuracy, completeness, or fitness for any particular purpose of any information contained herein. This report is not intended as investment advice, and should not be viewed as any guarantee of value, condition, or other attribute.

Contact Information:

Media Contact:

Michelle Sabolich

Atomic PR for Clear Capital

415.593.1400