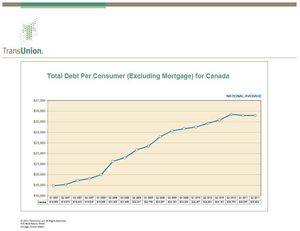

TORONTO--(Marketwire - Sep 7, 2011) - TransUnion's quarterly analysis of Canadian credit trends found that the average consumer's total debt (excluding mortgage) continued to stabilize in the second quarter, marking a potential new trend after the country experienced 26 straight quarterly increases between 2Q 2004 and 4Q 2010. Canadians' total debt declined from $25,709 to $25,597 between 4Q 2010 and 1Q 2011 and rose only $6 in the second quarter, coming in at $25,603.

"After six plus years of accruing larger credit balances, Canadians appear to be making a concerted effort to stabilize their debt load," said Thomas Higgins, TransUnion's vice president of analytics and decision services. "Though two quarters do not make a trend, the uncertain economy coupled with more conservative approaches to consumer credit use, could possibly make this a new development that takes shape in the short term."

The appearance of consumer debt stabilization comes at a time when the total active credit population in Canada declined between the first and second quarters of 2011, marking the first such quarterly drop since 1Q10. The active credit population now stands at 24.9 million consumers, approximately 230,000 fewer than in 1Q11.

Changes in total debt appear to be occurring throughout Canada. While only four provinces experienced quarterly declines in the first three months of 2011, a total of six provinces experienced drops in their total debt in the second quarter of 2011. For 2011 to date, New Brunswick (-$696 to $21,547) and Ontario (-$518 to $24,721) experienced the largest declines in total debt per person. Bucking the trend was Quebec, showing marked increases in 2011 and British Columbia showing a reversal in Q2 compared to the previous two quarters.

| Q2 2010 | Q3 2010 | Q4 2010 | Q1 2011 | Q2 2011 | ||||||

| British Columbia | $36,748 | $37,193 | $36,785 | $36,649 | $36,820 | |||||

| Alberta | $32,753 | $33,067 | $34,020 | $34,185 | $34,081 | |||||

| Ontario | $24,185 | $24,383 | $25,239 | $24,869 | $24,721 | |||||

| Quebec | $17,160 | $17,521 | $17,424 | $18,025 | $18,269 |

Consumer Debt -- Quarterly/Yearly

While total consumer debt for the first six months of 2011 remains lower than at its peak in 4Q10, it still remains 3% higher versus last year ($24,861 in 2Q10 to $25,603 in 2Q11).Other key credit statistics, include:

- Canadian average credit card borrower debt (defined as the aggregate balance on all credit cards for an individual bankcard borrower) declined 0.67% year over year and posted a typical seasonal increase of 1.4% quarter over quarter.

- Canadian lines of credit (LOC) borrower debt (defined as the aggregate balance on all LOC for an individual LOC borrower) increased 5.4% year over year and 2.8% quarter over quarter.

- Canadian installment loan borrower debt (defined as the aggregate balance on all installment loans for an individual installment loan borrower) decreased 1.0% year over year and 0.6% quarter over quarter.

- Canadian auto borrower debt (defined as the aggregate balance on all auto captive loans for an individual auto captive borrower) increased more than 10% year over year and 3.0% quarter over quarter.

"On the debt front, it appears that the slowdown cuts across multiple product categories, excluding the auto sector and lines of credit," said Higgins. "The recent warnings of interest rate hikes may have started to have an impact, but it may be short lived with the growing economic uncertainty and shelving of interest rate moves by the Bank of Canada."

| Q2 2010 | Q3 2010 | Q4 2010 | Q1 2011 | Q2 2011 | ||||||

| Credit Cards | $3,614 | $3,709 | $3,688 | $3,539 | $3,599 | |||||

| Lines of Credit | $32,113 | $32,649 | $33,981 | $33,762 | $33,855 | |||||

| Installment Loans | $22,499 | $22,731 | $22,976 | $22,431 | $22,281 | |||||

| Auto Captives | $15,135 | $16,183 | $16,189 | $16,181 | $16,671 |

Consumer Delinquencies -- Quarterly/Yearly

Delinquency levels continued to decline across all credit products on a yearly basis. "Canadians appear to have a handle on their delinquency levels as compared to just a few years ago," said Higgins. "Delinquencies have been on a consistent downward trend for two years now, but seem to be settling in."

| Q2 2010 | Q1 2011 | Q2 2011 | Q/Q Chg | Y/Y Chg | ||||||

| Credit Cards | 0.36% | 0.38% | 0.33% | -13.2% | -8.3% | |||||

| Lines of Credit | 0.22% | 0.22% | 0.20% | -10.0% | -10.0% | |||||

| Installment Loans | 1.53% | 1.28% | 1.27% | -0.8% | -17.0% | |||||

| Auto Captives | 0.11% | 0.11% | 0.10% | -9.1% | -9.1% |

Three Highest Delinquency Provinces

| Credit Cards | Lines of Credit | Installment Loans | Auto Captives | |||

| PEI 0.61% | BC 0.25% | ON 1.96% | MB 0.45% | |||

| NFLD 0.56% | ON 0.24% | PEI 1.86% | NB 0.18% | |||

| NB & NS 0.52% | AB 0.21% | NS 1.80% | NS 0.14% |

Three Lowest Delinquency Provinces

| Credit Cards | Lines of Credit | Installment Loans | Auto Captives | |||

| QC 0.21% | NL 0.10% | QC 0.47% | QC 0.06% | |||

| BC 0.30% | QC 0.13% | SK 1.15% | AB 0.07% | |||

| SK 0.30% | NB 0.15% | NL 1.19% | BC 0.08% |

TransUnion's Market Trends

TransUnion's Market Trends is an in-depth, full sample solution that provides statistical information every quarter from TransUnion's national consumer credit database, culled from anonymous credit files. Each Canadian consumer record contains hundreds of credit variables that illustrate consumer credit usage and performance. By leveraging Market Trends, customers from a variety of industries can analyze industry trends over an entire business cycle, helping to understand consumer behaviour in different geographic locations throughout Canada.

About TransUnion

As a global leader in information and risk management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering high quality data, and integrating advanced analytics and enhanced decision-making capabilities. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Based in Burlington, Ontario, with global headquarters located in Chicago, Illinois, TransUnion provides local service and support throughout Canada. Visit www.transunion.ca to learn more.

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail:

Telephone: 1 312 972 6646