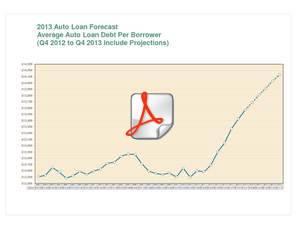

CHICAGO, IL--(Marketwire - Dec 18, 2012) - TransUnion released its annual national auto loan delinquency forecast today indicating that the ratio of borrowers 60 or more days past due will remain near record-low levels throughout 2013. TransUnion also forecasts that auto debt per borrower will continue its uptrend next year, jumping from an expected $13,689 in Q4 2012 to $14,133 at the end of 2013, a sign that auto financing will continue to grow as new and used car sales increase.

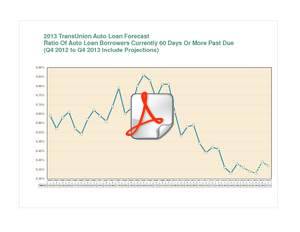

Though the national auto loan delinquency rate is expected to rise slightly from 0.36% at the end of 2012 to 0.37% in Q4 2013, the level has dropped more than 50% since reaching its peak in Q4 2008 at 0.86%.

| 60-Day National Auto Loan Delinquency Rate (Q4 2012 and Q4 2013 include projections) | |||||

| Q4 2008 | Q4 2009 | Q4 2010 | Q4 2011 | Q4 2012 | Q4 2013 |

| 0.86% | 0.81% | 0.59% | 0.46% | 0.36% | 0.37% |

"The national auto loan delinquency rate should stay relatively low throughout 2013 as the economy continues to improve," said Peter Turek, automotive vice president in TransUnion's financial services business unit. "Macroeconomic factors such as the improving unemployment rate, median household income and housing prices are some of the primary drivers that lead us to a favorable forecast."

Seventeen states are expected to see delinquencies drop or remain the same during 2013. However, 21 of the states are forecasted to experience auto loan delinquency increases of only 1 or 2 basis points. The largest yearly percentage auto delinquency declines are expected in Georgia (-13.04%), California (-7.50%) and Alaska (-5.56%). The largest percentage increases are expected in Hawaii (17.24%), Virginia (11.54%) and Nevada (11.11%).

The low auto loan delinquency environment has persisted even as more non-prime, higher-risk consumers carry auto loan balances. In Q3 2011, TransUnion's Industry Insights database found approximately 19.97 million borrowers with a VantageScore® credit score lower than 700 (on a scale of 501-990) carried auto loan balances. This number increased to 20.66 million in Q3 2012.

"It's a real sign that the automobile market is on solid footing that even with more non-prime consumers carrying auto loan balances, we've continued to maintain a low national auto loan delinquency rate," said Turek. "We believe this is happening partly because consumers are now valuing their auto loans even more than their credit card and mortgage loans; also lenders and dealers are putting even more emphasis on placing buyers in vehicles and loans that best fit their financial situation."

The total number of consumers carrying auto loan balances also has increased in the last year, rising from 59.27 million in Q3 2011 to 61.68 million in Q3 2012. With this rise, auto loan debt per borrower jumped from $12,902 to $13,571 in those same periods. If TransUnion's 2013 forecast holds true, auto loan debt will have increased 11 straight quarters since Q1 2011. In the 11 quarters prior to Q1 2011, auto loan debt experienced only three quarterly increases.

TransUnion's forecast is based on various economic assumptions, such as unemployment rates, consumer sentiment, disposable income and interest rates. The forecast changes as the economy deviates from a conservative economic forecast or if there are unanticipated shocks to the economy affecting recovery.

60-Day Auto Loan Delinquency Projections for 2013

| 2011-2013 | Q4 2011 | Q4 2012 | Q4 2013 | |

| USA | 0.46% | 0.36% | 0.37% | |

| Highest Auto Loan Delinquency States | Q4 2013 | |

| Mississippi | 0.88% | |

| Louisiana | 0.88% | |

| West Virginia | 0.70% | |

| Lowest Auto Loan Delinquency States | Q4 2013 | |

| Montana | 0.13% | |

| Alaska | 0.17% | |

| Minnesota | 0.23% | |

Note: Q4 2012 also is a projected number as the quarter has not yet ended.

The most current auto loan delinquency data for the nation and every state can be found at www.transunion.com/trenddata.

TransUnion's Trend Data database

TransUnion's Trend Data is a one-of-a-kind database consisting of 27 million anonymous consumer records randomly sampled every quarter from TransUnion's national consumer credit database. Each record contains more than 200 credit variables that illustrate consumer credit usage and performance. Since 1992, TransUnion has been aggregating this information at the county, Metropolitan Statistical Area (MSA), state and national levels. For the purpose of this analysis, the term "credit card" refers to those issued by banks.

About TransUnion

As a global leader in information and risk management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering high quality data, and integrating advanced analytics and enhanced decision-making capabilities. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion reaches businesses and consumers in 33 countries around the world. www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail

Telephone 312 972 6646