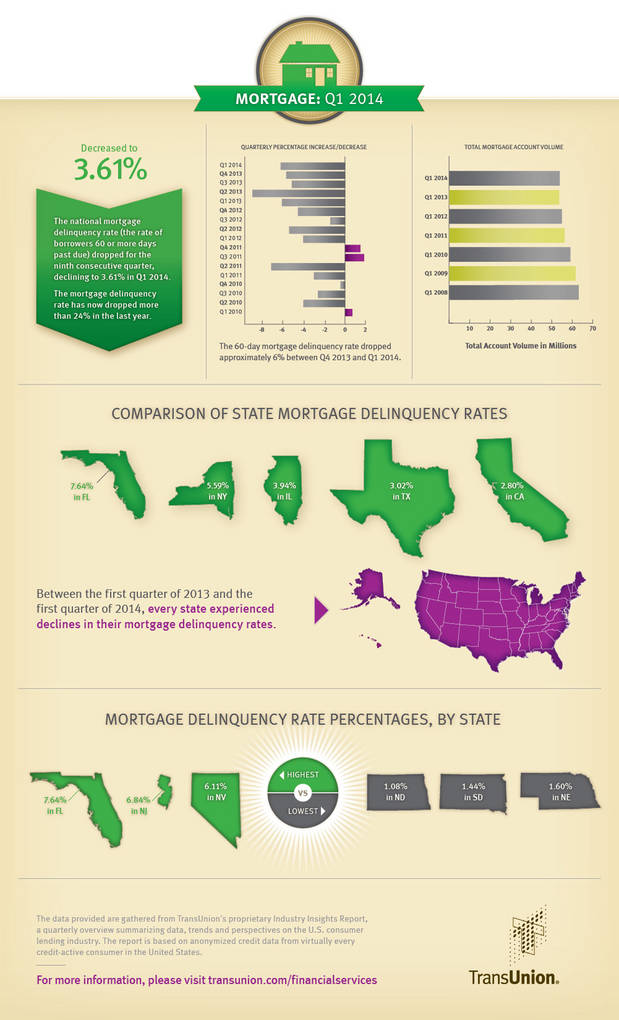

CHICAGO, IL--(Marketwired - May 7, 2014) - The mortgage delinquency rate (the rate of borrowers 60 days or more delinquent on their mortgages) declined for the ninth consecutive quarter to 3.61% at the end of Q1 2014, according to TransUnion's latest mortgage report. The mortgage delinquency rate has declined more than 24% in the last year (down from 4.76% in Q1 2013), and it is now at the exact same level as it stood in Q2 2008.

"It's encouraging to see mortgage delinquencies drop once again, especially during a period when mortgage originations slowed considerably," said Steve Chaouki, head of financial services for TransUnion. "This trend in improved performance is driven in part by lenders working their way through the foreclosure backlog, along with continued conservatism in underwriting new mortgages."

All 50 states and the District of Columbia experienced declines in their mortgage delinquency rates between Q1 2013 and Q1 2014. The largest percentage declines continued to occur in states most impacted by the mortgage crisis -- Arizona (down 37.8%), California (down 36.9%) and Nevada (down 34.0%). Both Arizona (2.81%) and California (2.80%), which just five years earlier had delinquency rates nearly double the national average, are now significantly lower than the rest of the nation.

TransUnion recorded 53.47 million mortgage accounts as of Q1 2014, up from 53.06 million in Q1 2013. However, there are more than 9.91 million fewer accounts as compared to the same period in 2008 (63.38 million).

Viewed one quarter in arrears (to ensure all accounts are reported and included in the data), new account originations dropped from 2.33 million in Q4 2012 to 1.39 million in Q4 2013. Interestingly, the non-prime population (those consumers with a VantageScore® 2.0 credit score lower than 700) did see an increase in their share of originations, rising from 4.98% in Q4 2012 to 7.21% in Q4 2013. The decline in refinance activity may have contributed to this outcome. Despite the increase, the percentage of non-prime account originations remains well below those observed just six years ago (15.97% in Q4 2007).

"While still far from levels seen six years ago, non-prime borrowers are taking a larger share of new originations," said Chaouki. "We have not seen this in quite some time. Even so, mortgage underwriting remains conservative relative to the other primary credit products in the marketplace."

TransUnion is forecasting that the downward consumer delinquency trend will continue into the second quarter of 2014, with mortgage delinquencies falling to approximately 3.40% by the end of June.

TransUnion's forecast is based on various economic assumptions, such as gross state product, consumer sentiment, unemployment rates, real personal income, and real estate values. The forecast would change if there are unanticipated shocks to the economy affecting recovery in the housing market or if home prices begin to depreciate once again.

"We expect mortgage originations will once again pick up steam, and with continued tight lending standards, this should only help further bring down the mortgage delinquency rate," added Chaouki.

This information is reported by TransUnion and is part of its ongoing series of quarterly analyses of credit-active U.S. consumers and how they are managing credit related to mortgages, credit cards and auto loans. To subscribe to TransUnion news releases, please click here.

Q1 2014 Mortgage Statistics - Delinquency Rates

| Quarter over Quarter | Q4 2013 | Q1 2014 | Pct. Change | |||

| USA | 3.85% | 3.61% | (6.2%) | |||

| Year over year | Q1 2013 | Q1 2014 | Pct. Change | |||

| USA | 4.76% | 3.61% | (24.2%) | |||

| Mortgage Delinquency Rate for Select States | Q1 2014 | |

| California | 2.80% | |

| Florida | 7.64% | |

| Illinois | 3.94% | |

| New York | 5.59% | |

| Texas | 3.02% | |

| Largest Year-over-Year Declines | Q1 2013 | Q1 2014 | Pct. Change | |||

| Arizona | 4.52% | 2.81% | (37.8%) | |||

| California | 4.44% | 2.80% | (36.9%) | |||

| Nevada | 9.26% | 6.11% | (34.0%) | |||

| Smallest Year-over-Year Declines | Q1 2013 | Q1 2014 | Pct. Change | |||

| New York | 6.07% | 5.59% | (7.9%) | |||

| New Jersey | 7.44% | 6.84% | (8.1%) | |||

| Vermont | 2.83% | 2.59% | (8.5%) | |||

About TransUnion

As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion reaches businesses and consumers in 33 countries around the world on five continents. www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail:

Telephone: (312) 985 3059