MINNEAPOLIS, MN--(Marketwired - Mar 26, 2015) - Groveland Capital, LLC. (the "Groveland Group") announced today that it has filed a letter with the U.S. Securities and Exchange Commission ("SEC"), saying that shareholders of Biglari Holdings Inc. (

The Groveland Group has nominated six independent professionals for the Board of Directors of Biglari Holdings (the "Company" or "BH") and is soliciting votes from fellow Biglari Holdings' shareholders for the election of these individuals at Biglari Holdings' annual meeting, which is scheduled for Thursday, April 9, 2015. The Groveland Group's six highly qualified and experienced nominees include: Nicholas J. Swenson, James W. Stryker, Thomas R. Lujan, Stephen J. Lombardo, III, Ryan P. Buckley and Seth G. Barkett.

Nick Swenson, Principal and Founder of Groveland Capital, stated: "We believe Biglari Holdings has significant potential if corporate governance is reformed and the right operational focus is achieved. We are committed to driving shareholder value for you, our fellow shareholders. We believe the current board has failed BH shareholders in its corporate governance responsibilities. In our view, new board members are needed to check the power of BH's CEO Mr. Biglari and the Company's board."

Added Mr. Swenson, "We are seeking your support to change and reform Biglari Holdings Inc. for the better. We believe BH shareholders are primed for change and deserve a choice. We believe if nothing is done, indications point to continued financial underperformance, continued poor corporate governance, continued wasteful spending and egregious CEO compensation. Change may seem difficult, but the greatest risk to BH shareholders is the status quo."

WE URGE YOU TO CHECK THE POWER OF BIGLARI HOLDINGS CEO MR. SARDAR BIGLARI BY VOTING THE WHITE PROXY CARD.

Key excerpts of today's Groveland Group letter filed with the SEC include:

1. Mr. Biglari's application of conglomerate accounting has made it very difficult for us at the Groveland Group to validate significant claims made by the Company regarding its operating performance. This is critically important because consolidated operating cash flows are declining at a concerning rate. We believe shareholders are at risk of seeing continuing declines in operating performance. Based on the public record, the simple truth is that Mr. Biglari's franchising initiatives have generated significant operating losses for years! And, of course, Maxim's cash burn has been $21.5 million over the first 10.5 months of BH ownership. Repeated references to same-store-sales growth at Steak n Shake are no comfort in the face of these disconcerting and persistent losses.

2. Mr. Biglari seems to steadfastly refuse to respond directly to the operating issues and corporate governance problems that concern shareholders, which we have described in our definitive proxy statement, instead repeating assertions that seem to imply that shareholders have nothing to worry about.

3. Franchising Initiative Is Glamorous Yet Unprofitable

- We question the business case for the Company's global footprint and franchising initiatives that correspond with some of the most glamorous and expensive cities in the world: Monte Carlo, Ibiza, Dubai, Cannes, and Santa Monica. Is franchising initiative driven by business logic that generates shareholder value or is it driven by a desire for lavish corporate travel and entertainment? The BH stock price has had a decidedly unglamorous five years of underperformance.

- According Mr. Biglari's Letter to Shareholders from 2013, "Thus, we began allocating sizable capital to franchising efforts in fiscal 2011 as direct franchising costs represented 10.4% of G&A. In fiscal 2012, these costs increased to 14.8% of G&A. We have steadily intensified our investment, upping it to 24.8% of G&A in fiscal 2013." In his 2014 Shareholder Letter Mr. Biglari stops reporting the percentage of G&A that the Company is spending on the franchising initiative. We fear that the percentage has continued to increase. If we assume, however, that 24.8% of G&A was again spent on franchising in fiscal 2014, then Mr. Biglari spent $21.1 million on franchising. Based on public filings, total franchising royalties and fees were only $15.0 million in fiscal 2014. Therefore, we estimate that the Company's franchising initiative lost $6.1 million in fiscal 2014.

- Using Mr. Biglari's Letters and SEC reports for BH, we conclude that in fiscal 2013, the Company spent $19.0 million on franchising and generated franchising royalties and fees of $11.7 million, resulting in a franchising loss of $7.3 million. In fiscal 2012, the Company spent $9.5 million on franchising and generated franchising royalties and fees of $9.6 million, resulting in a franchising gain of a mere $100,000. With this history, it appears the Company's best years in the franchising business were before Mr. Biglari became CEO. Steak n Shake was generating approximately $4 million annually in franchising royalties and fees with nominal expenses. Based on our research and analysis, an efficient and well-run franchising program the size of Steak n Shake's should only cost $1 million to $2 million annually.

4. Maxim Is Generating Significant Operating Losses

- In regards to Maxim, based on public filings, Mr. Biglari's February 2014 acquisition of Maxim has resulted in an operating loss of $21.5 million to BH through December 31, 2014, including a $5.5 million operating loss in the latest quarter. We note that this amount is significantly greater than the Company's operating income of $12.6 million over the last twelve months. Maxim's operating loss of $21.5 million over the past ten months plus the $15.0 million that BH spent to acquire Maxim totals a cash outflow of $36.5 million; these numbers do not support the Company's repeated claim that Maxim is an immaterial bet!

- We believe that Maxim may be challenged by the fact that the traditional 'lad mags' category is in decline, based on industry data, and that it is up against better capitalized and well-established incumbents. How will Maxim differentiate itself? What is clear is that Maxim is currently generating significant operating losses for Biglari Holdings.

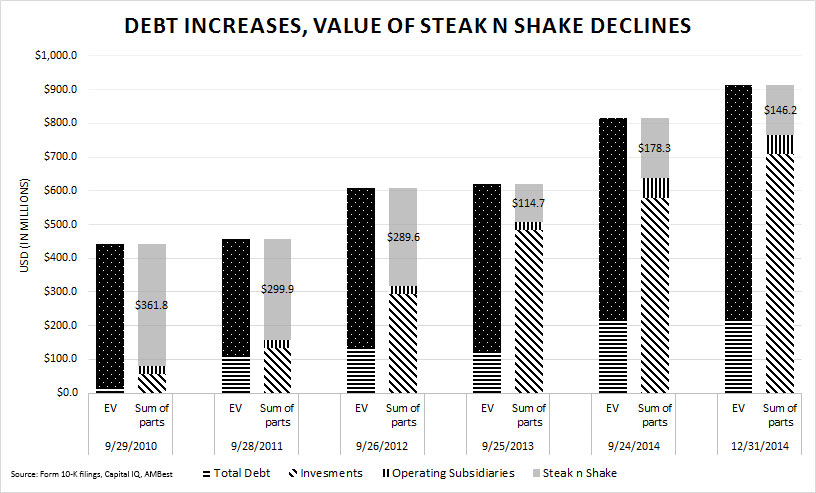

5. Expanding Debt and Shrinking Market Value of Steak n Shake

- While we found it entertaining to listen to Mr. Biglari's chest pounding account of his turnaround at Steak n Shake, it appears that the market simply disagrees with him. If we perform a sum of the parts analysis, the implied value of Steak n Shake as of September 29, 2010 was $361.8 million. We performed the same analysis for December 31, 2014, and the implied value of Steak n Shake is $146.2 million.

- So, using the attached chart entitled "DEBT INCREASES, VALUE OF STEAK N SHAKE DECLINES" and the below analysis, the implied value of Steak n Shake has declined 59.6% since 2010. Does Mr. Biglari 'hear the market'?

| Enterprise Value (in millions) | 9/29/2010 | 9/28/2011 | 9/26/2012 | 9/25/2013 | 9/24/2014 | 12/31/2014 | |||||||||||||

| Market Capitalization | $ | 470.4 | $ | 443.4 | $ | 535.7 | $ | 595.3 | $ | 721.0 | $ | 825.4 | |||||||

| Long-term Debt | 17.8 | 101.4 | 120.3 | 110.5 | 215.5 | 214.5 | |||||||||||||

| Current Debt | 0.2 | 11.1 | 12.1 | 9.8 | 2.9 | 2.9 | |||||||||||||

| Cash | 47.6 | 99.0 | 60.4 | 94.6 | 124.3 | 129.7 | |||||||||||||

| Enterprise Value | $ | 440.8 | $ | 457.0 | $ | 607.8 | $ | 620.9 | $ | 815.1 | $ | 913.1 | |||||||

| Operating Subsidiaries | |||||||||||||||||||

| MAXIM (1) | $ | 15.0 | $ | 15.0 | |||||||||||||||

| First Guard (2) | 20.0 | 20.0 | |||||||||||||||||

| Western (3) | $ | 23.0 | $ | 23.0 | $ | 23.0 | $ | 23.0 | 23.0 | 23.0 | |||||||||

| Total Value of Operating Subsidiaries | $ | 23.0 | $ | 23.0 | $ | 23.0 | $ | 23.0 | $ | 58.0 | $ | 58.0 | |||||||

| Investments | |||||||||||||||||||

| Investments | $ | 32.5 | $ | 115.3 | $ | 269.9 | $ | 85.5 | $ | 21.5 | $ | 10.8 | |||||||

| Investment Partnerships | 23.5 | 18.8 | 25.3 | 397.7 | 557.2 | 698.0 | |||||||||||||

| Total Investments | $ | 56.0 | $ | 134.1 | $ | 295.1 | $ | 483.2 | $ | 578.8 | $ | 708.8 | |||||||

| Implied Value of Steak n Shake (4) | $ | 361.8 | $ | 299.9 | $ | 289.6 | $ | 114.7 | $ | 178.3 | $ | 146.2 | |||||||

| Implied Value of Steak n Shake per share | $ | 252.35 | $ | 209.25 | $ | 202.02 | $ | 66.67 | $ | 86.33 | $ | 70.80 | |||||||

| Note: | ||

| (1) | Maxim is valued at its purchase price of $15.0 million. | |

| (2) | First Guard Insurance is valued at its last reported Policyholder Surplus by AMBest. | |

| (3) | Western Sizzlin is valued at its purchase price of $23.0 million. | |

| (4) | Implied Value of Steak n Shake equals Enterprise Value less Total Value of Operating Subsidiaries less Total Investments | |

| Source: Form 10-K filings, Capital IQ, AMBest | ||

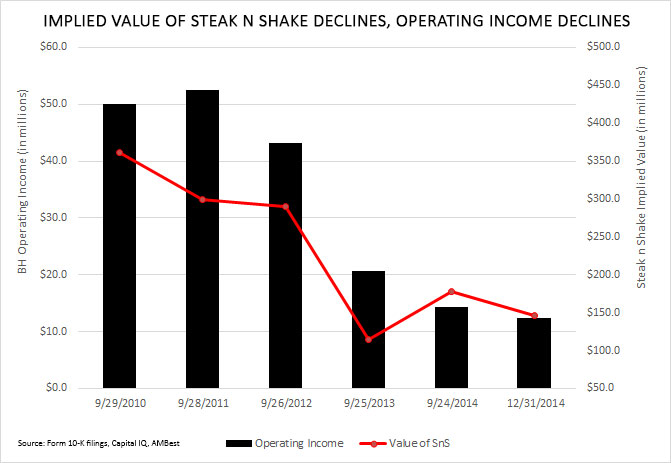

- Why has the implied market value of Steak n Shake shrunk by 59.6% since 2010? The answer becomes obvious when comparing the loss in value to BH's deterioration in operating income. The market seems to be implying that Mr. Biglari's "turnaround" of Steak n Shake has resulted in the company heading off in the wrong direction.

- Please see attached chart entitled "IMPLIED VALUE OF STEAK N SHAKE DECLINES, OPERATING INCOME DECLINES" for details.

- Alongside deteriorating operating income, we can see that the implied value of Steak n Shake is declining and has been in decline for the last 5 years.

6. We Believe The Board Has Failed In Its Corporate Governance Responsibilities

- In our opinion, Biglari Holdings' sale of Biglari Capital to Mr. Biglari in July 2013 clearly demonstrates that the board is not looking out for the best interests of shareholders. As a result of selling Biglari Capital back to Mr. Biglari in 2013, which was done without shareholder input, Mr. Biglari now has the opportunity to continue to receive his compensation from Biglari, while also receiving incentive fees for managing the assets of the Lion Funds, with a full 86.5% of those assets being made up of BH's assets that Mr. Biglari himself allocated to the Lion Funds. So, one end result of the sale of Biglari Capital back to Mr. Biglari is increased compensation to Mr. Biglari, and shareholder approval (input) was not solicited for this increase.

- This, despite the fact that when Mr. Biglari's Incentive Agreement was put in place, the Governance, Compensation and Nominating Committee capped the payments that Mr. Biglari could receive under the Incentive Agreement, and the Committee promised that it would look out for shareholders' interests in connection with the Incentive Agreement: "Any amendment that would materially increase the benefits to Mr. Biglari, including any amendment that would reasonably be expected to increase his incentive compensation, must be approved by shareholder vote." (Source: BH Schedule 14A filed 9/29/2010)

- The current board has also presided over Biglari while the overwhelming majority of the Company's assets ($776.7 million or 94.1% of the Company's market capitalization as of 12/31/14) have been transferred by Mr. Biglari into entities beyond the board's direct governance oversight and controlling influence and allowed Steak n Shake to incur significant bank debt in the process ($218.4 million as of December 31, 2014).

- We also believe that the board has entrenched itself and the Company's CEO as well as disenfranchised BH's shareholders with the approval of Mr. Biglari's Trademark Licensing Agreement in January 2013 between Mr. Biglari and the Company. Commenting on the licensing arrangement, Bernard Black, Chabraja Professor at Northwestern University Law School and Kellogg School of Management has stated, "The [Biglari] license agreement has no business justification, and is equivalent to a super golden parachute, on top of the rich parachute that BH has already granted to Biglari"..."The license agreement is a form of asset tunneling in; the payment on a change of control grossly exceeds any plausible value of the Biglari name to the BH restaurants." (Source: Case 1:13-cv-00891-SEB-MJD, Southern District of Indiana 9/6/2013)

If Groveland Group's director nominees are elected by the shareholders of Biglari Holdings, we plan to expeditiously implement the following KEY INITIATIVES:

1. Immediately appoint Gene Baldwin as interim CEO of Biglari Holdings. Mr. Baldwin has more than 35 years of accounting, finance, senior management and advisory experience. He is a proven business leader with a well-established reputation in the restaurant industry for his ability to assess, develop, and implement operational and financial improvement initiatives that enhance enterprise value for all stakeholders.

2. Review and reduce consolidated SG&A expenses throughout BH; Evaluate global restaurant footprint, real estate values, and lease costs

3. Repair employee and franchisee relations by re-establishing open lines of communication

4. Hire an executive search firm to find a permanent CEO (likely to take 4-6 months)

5. Reform corporate governance policies and procedures

6. Remove "by Biglari" moniker from restaurant signage

7. Assert shareholder rights with respect to BH's investment in the Lion Funds and any shared services agreements between BH and BCC

8. Assert shareholder rights with respect to change of control payments

9. Perform a financial, operational, and strategic review of Maxim, First Guard Insurance and Western Sizzlin

10. Further engage with BH's shareholders to better understand the consensus viewpoint surrounding capital allocation initiatives and strategic options to maximize shareholder value

The entirety of Groveland Group letter, along with other materials related to the Biglari Holdings proxy contest, is available on the website www.ReformBH.com and on the SEC's website www.sec.gov.

VOTE THE WHITE PROXY CARD TO REFORM BIGLARI HOLDINGS.

Your Vote Is Important -- No Matter How Many Or How Few Shares You Own

If you have questions about how to vote your shares, or need additional assistance, please contact the firm assisting us in the solicitation of proxies:

D.F. KING & CO., INC.

Shareholders Call Toll-Free: 877-283-0325

Banks and Brokers May Call Collect: 212-269-5550

REMEMBER:

We urge you NOT to sign any Blue proxy card sent to you by the Company. If you have already done so, you have every right to change your vote by signing, dating and returning the enclosed WHITE proxy card TODAY in the postage-paid envelope provided. If you hold your shares in Street-name, your custodian may also enable voting by telephone or by Internet -- please follow the simple instructions provided on your WHITE proxy card.

About Groveland Capital, LLC

Groveland Capital, LLC. is an Investment Advisor based in Minneapolis, MN. Groveland Capital is nimble advisory focused on unearthing unique investment opportunities. Our insight and global network is complemented by our billion dollar+ fund experience and expertise. Groveland Capital is led by a seasoned team of investment professionals who have continuity, vision and over a decade of experience executing key elements of our investment strategy. Groveland Capital founder and Principal, Nick Swenson, also has significant capital invested in the portfolio, aligning his interests with investors. Our investment strategy is to acquire stakes in undervalued and/or underperforming companies. When necessary, we seek board representation and advocate for improvements in financial performance, capital allocation, and corporate governance for the benefit of all shareholders.

Important Information

The Groveland Group (whose members are identified below) has nominated Nicholas J. Swenson, James W. Stryker, Stephen J. Lombardo III, Thomas R. Lujan, Ryan P. Buckley, and Seth G. Barkett as nominees to the board of directors of Biglari Holdings Inc. (the "Company"), and is soliciting votes for the election of Nicholas J. Swenson, James W. Stryker, Stephen J. Lombardo III, Thomas R. Lujan, Ryan P. Buckley, and Seth G. Barkett as members of the Company's board of directors (the "Groveland Nominees"). The Groveland Group has sent a definitive proxy statement, WHITE proxy card and related proxy materials to shareholders of the Company seeking their support of the Groveland Nominees at the Company's 2015 Annual Meeting of Shareholders. Shareholders are urged to read the definitive proxy statement and WHITE proxy card because they contain important information about the Groveland Group, the Groveland Nominees, the Company and related matters. Shareholders may obtain a free copy of the definitive proxy statement and WHITE proxy card and other documents filed by the Groveland Group with the Securities and Exchange Commission ("SEC") at the SEC's web site at www.sec.gov. The definitive proxy statement and other related SEC documents filed by the Groveland Group with the SEC may also be obtained free of charge from the Groveland Group.

Participants in Solicitation

The "Groveland Group" currently consists of the following persons who are participants in the solicitation from the Company's shareholders of proxies in favor of the Groveland Nominees: Groveland Master Fund Ltd. (formerly known as Groveland Hedged Credit Master Fund Ltd.), Groveland Hedged Credit Fund LLC, Groveland Capital LLC, Nicholas J. Swenson, and Seth G. Barkett. Along with the Groveland Group, the following are also participants in the solicitation: James W. Stryker, Stephen J. Lombardo III, Thomas R. Lujan, and Ryan P. Buckley. The participants may have interests in the solicitation, including as a result of holding shares of the Company's common stock. Information regarding the participants and their interests may be found in the Groveland Group's definitive proxy statement, as filed with the SEC on March 11, 2015. These materials may be accessed from the SEC's website free of charge.

Contact Information:

Contacts

Investors:

Nick Swenson

Groveland Capital

612-843-4302

D.F. King & Co., Inc.

212-269-5550

Media:

Anthony Giombetti

Gio Public Relations

818-821-7530