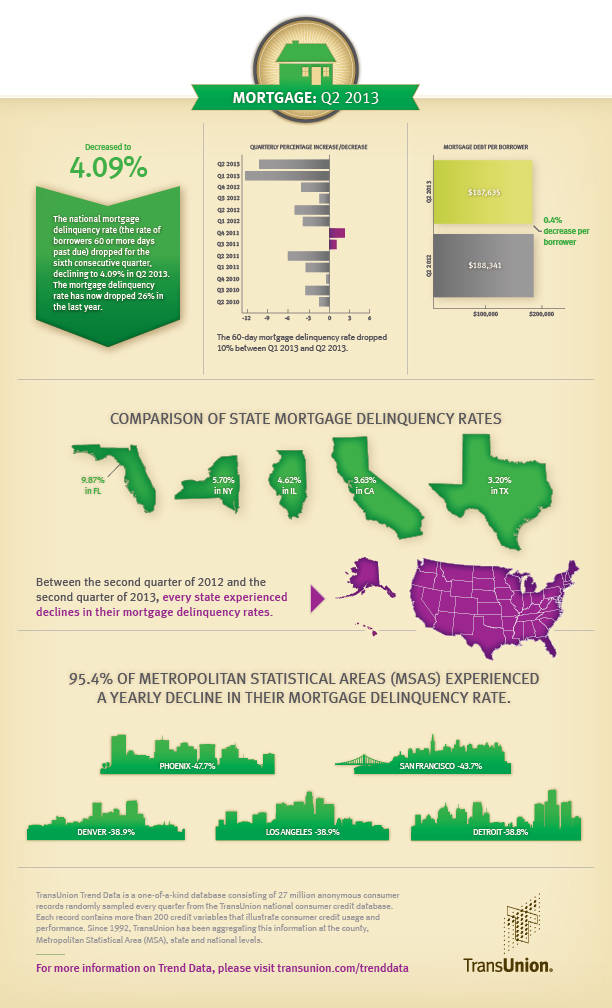

CHICAGO, IL--(Marketwired - Aug 6, 2013) - The national mortgage delinquency rate (the rate of borrowers 60 or more days past due) continued its unprecedented decline in 2013, dropping to 4.09% in Q2 2013, nearly 26% lower versus the same time last year. Since last quarter, the mortgage delinquency rate has declined 10%.

"This marks the third quarter in a row where we have posted all-time highs in terms of delinquency improvement and that is very welcome news for both borrowers and their lenders," said Tim Martin group vice president of U.S. Housing in TransUnion's financial services business unit. "Many of the delinquent mortgages we have been tracking have been delinquent for a very long time, so it is encouraging to see this number is coming down so significantly."

Every state and the District of Columbia experienced improvement in their mortgage delinquency rates from last year. As in the past several quarters, Arizona (-41.7%) and California (-40.8%) experienced the largest yearly mortgage delinquency declines. The two states with the highest mortgage delinquency rates in the nation -- Florida and Nevada -- also had encouraging yearly drops of (-26.8%) and (-28.7%), respectively.

At a more granular level, 95.4% of MSAs experienced a yearly drop in their mortgage delinquency rate. This percentage was an improvement over the previous quarter of 91.0%. Several major markets saw the largest declines, including Phoenix (-47.7%), San Francisco (-43.7%), Denver (-38.9%), Los Angeles (-38.9%) and Detroit (-38.8%).

"Improving house prices and low interest rates have helped some homeowners across the country refinance or sell their way out of mortgage payments they were having difficulty affording," said Martin. "While we expect these positive factors to continue reducing the mortgage delinquency rate throughout 2013, the recent and sizable increase in mortgage interest rates may eventually slow the progress."

TransUnion expects the mortgage delinquency rate to continue its downward trend in the third quarter of 2013, finishing below 4% for the first time since 2008.

This information is reported by TransUnion and is part of its ongoing series of quarterly analyses of credit-active U.S. consumers and how they are managing credit related to mortgages, credit cards and auto loans.

TransUnion's forecast is based on various economic assumptions, such as gross state product, consumer sentiment, unemployment rates, real personal income, and real estate values. The forecast would change if there are unanticipated shocks to the economy affecting recovery in the housing market or if home prices fall more than expected.

Q2 2013 Mortgage Statistics - Delinquency Rates

| Quarter over Quarter | Q1 2013 | Q2 2013 | Pct. Change | |||

| USA | 4.56% | 4.09% | (10.3%) | |||

| Year over year | Q2 2012 | Q2 2013 | Pct. Change | |||

| USA | 5.49% | 4.09% | (25.5%) | |||

| Highest Mortgage Delinquency States | Q2 2013 | |||||

| Florida | 9.87% | |||||

| Nevada | 7.74% | |||||

| New Jersey | 7.21% | |||||

| New York | 5.70% | |||||

| Lowest Mortgage Delinquency States | Q2 2013 | |||||

| North Dakota | 1.15% | |||||

| South Dakota | 1.53% | |||||

| Nebraska | 1.81% | |||||

| Alaska | 1.88% | |||||

| Top 3 Year-over-Year Increases | Q2 2012 | Q2 2013 | Pct. Change | |||

| *No states experienced increases | ||||||

| Top 3 Year-over-Year Declines | Q2 2012 | Q2 2013 | Pct. Change | |||

| Arizona | 6.14% | 3.58% | (41.7%) | |||

| California | 6.13% | 3.63% | (40.8%) | |||

| Colorado | 3.49% | 2.27% | (35.0%) | |||

Q2 2013 Mortgage Statistics - Mortgage Debt Per Borrower

| Quarter over Quarter | Q1 2013 | Q2 2013 | Pct. Change | |||

| USA | $186.018 | $187,635 | 0.9% | |||

| Year over Year | Q2 2012 | Q2 2013 | Pct. Change | |||

| USA | $188,341 | $187,635 | (0.4%) | |||

| Highest Mortgage Debt States | Q2 2013 | |||||

| District of Columbia | $374,446 | |||||

| California | $324,197 | |||||

| Hawaii | $315,837 | |||||

| Maryland | $249,661 | |||||

| Lowest Mortgage Debt States | Q2 2013 | |||||

| West Virginia | $102,829 | |||||

| Mississippi | $110,845 | |||||

| Oklahoma | $116,228 | |||||

| Arkansas | $116,573 | |||||

| Top 3 Year-over-Year Increases | Q2 2012 | Q2 2013 | Pct. Change | |||

| North Dakota | $120,241 | $128,260 | 6.7% | |||

| Montana | $155,409 | $162,446 | 4.5% | |||

| Texas | $137,290 | $140,928 | 2.6% | |||

| Top 3 Year-over-Year Declines | Q2 2012 | Q2 2013 | Pct. Change | |||

| Ohio | $131,701 | $125,707 | (4.6%) | |||

| Iowa | $125,285 | $120,557 | (3.8%) | |||

| Nevada | $214,262 | $206,362 | (3.7%) | |||

Supporting Resources/Links

TransUnion Trend Data Interactive U.S. Map

TransUnion 1Q13 Mortgage Statistics

TransUnion Mortgage Loan Modification Study

TransUnion Payment Hierarchy Study

TransUnion Life After Foreclosure Study

TransUnion on Twitter

TransUnion's Trend Data database

TransUnion's Trend Data is a one-of-a-kind database consisting of 27 million anonymous consumer records randomly sampled every quarter from TransUnion's national consumer credit database. Each record contains more than 200 credit variables that illustrate consumer credit usage and performance. Since 1992, TransUnion has been aggregating this information at the county, Metropolitan Statistical Area (MSA), state and national levels. For the purpose of this analysis, the term "credit card" refers to those issued by banks.

About TransUnion

As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion reaches businesses and consumers in 33 countries around the world on five continents. www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail

Telephone (312) 972-6646