VANCOUVER, BRITISH COLUMBIA and JOHANNESBURG, SOUTH AFRICA--(Marketwired - Oct. 19, 2016) - Platinum Group Metals Ltd. (TSX:PTM)(NYSE MKT:PLG) ("Platinum Group" or the "Company") announces positive results from an Independent Pre-Feasibility Study ("PFS") on the Waterberg PGM Project completed by international and South African engineering firm WorleyParsons RSA (Pty) Ltd. trading as Advisian. Platinum Group holds a 58.62% effective interest in the Waterberg Project with the Japan, Oil, Gas and Metals National Corporation ("JOGMEC") holding a 28.35% interest. Empowerment partner Mnombo Wethu Consultants (Pty) Ltd. ("Mnombo") holds the balance of the joint venture. JOGMEC funding is in place to advance the project through completion of a Feasibility Study ("FS").

Platinum Group Metals plans to continue drilling the deposit and to advance the project to completion of a FS and a construction decision. The Company also plans to file a mining right application, with Joint Venture approval, based substantially on the results of the PFS.

Highlights of the PFS include:

- Validation of the 2014 Waterberg Preliminary Economic Assessment ("PEA") results for a large scale, shallow, decline accessible, mechanized platinum, palladium, rhodium and gold ("4E") mine.

- Annual steady state production rate of 744,000 4E ounces in concentrate.

- A 3.5 year construction period.

- On site life-of-mine average cash cost of US$248 per 4E ounce including by-product credits and exclusive of smelter discounts.

- After-tax Net Present Value ("NPV") of US$320 million, at an 8% discount rate, using three-year trailing average metal prices.

- After-tax NPV of US$507 million, at an 8% discount rate, using investment bank consensus average metal prices.

- Estimated capital to full production of approximately US$1.06 billion including US$67 million in contingencies. Peak project funding estimated at US$914 million.

- After-tax Internal Rate of Return ("IRR") of 13.5% using three-year trailing average price deck.

- After-tax IRR of 16.3% at investment bank consensus average metal prices.

- Probable reserves of 12.3 million 4E ounces.

- Indicated resources updated to 24.9 million 4E ounces (2.5 g/t 4E cut-off) and deposit remains open on strike to the north and below a 1,250 meter arbitrary depth cut-off.

R. Michael Jones, CEO and co-founder of Platinum Group said, "The completion of the PFS significantly increases the Company's attributable 4E reserves and is an important milestone for the project and the Company. The PFS has a similar approach, similar peak funding in US dollar terms with increased production, compared to the PEA.

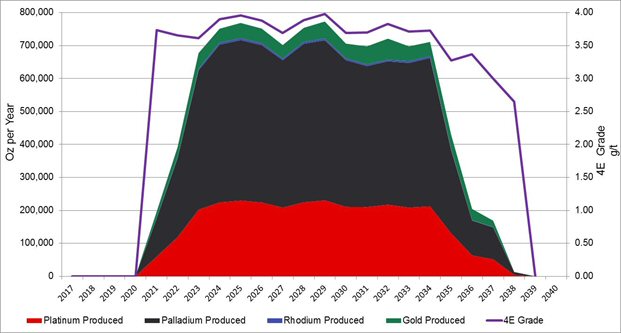

Waterberg is designed to be a low cost, multi-decline, fully mechanized, mining complex along an initial 13 km deposit strike length with two 300,000 tonne per month mills built in close sequence. At 744,000 ounces annual steady state production and a modelled 18 year mine life, Waterberg is very large and offers excellent exposure to the essential metals of platinum, palladium, rhodium and gold. Amazingly, the deposit is still open. The PFS covers only the first 218 million tonnes in Indicated resources to date.

With the full support of our joint venture partners JOGMEC and Mnombo, we look forward to advancing Waterberg during the remainder of 2016 and 2017 with more drilling, a FS on the initial complex, and the submission of a mining right application. From an original US$20 million commitment by JOGMEC in 2015, approximately US$8 million of further project funding remains to be spent. We are very appreciative of JOGMEC's continued commitment and support.

We look forward to growing and advancing Waterberg so that we may fully understand this new part of the Bushveld complex that we and our joint venture partners have discovered. We will work hard to maximize the value of the resource for all stakeholders including shareholders, employees, the Government of South Africa and the local communities."

This press release has been prepared by the qualified persons named herein. This press release is qualified in its entirety by reference to the PFS, which is expected to be filed shortly on SEDAR at www.sedar.com and the SEC's EDGAR site at www.sec.gov. Investors should refer to the PFS for further information.

SCALE AND PGM INDUSTRY POSITION

As a result of the shallow depth, good grades and a fully mechanized mining approach, the Waterberg Project has the opportunity to be a safe mine within the lowest quartile of the industry cost curve. The project resources consist of 60% palladium and the PFS estimates that Waterberg will produce 472,000 ounces of palladium annually; more palladium than the Stillwater Mine produced in 2015, or about 6% of the world's palladium production in 2015. Producing approximately 744,000 4E ounces per year, Waterberg would be one of the largest platinum group metals mine complexes in South Africa based on 2015 production numbers.

It is estimated that Waterberg will create approximately 3,361 new primary highly trained jobs with transferable skills. The increased safety, improved working conditions, low costs and decline access for rapid development all provide attractive features compared to traditional platinum and palladium mines in South Africa. The project is in an area prioritized for economic development. Relations with the small rural community in the area have been business like and positive.

Total Ounces Produced - Life of Mine: http://media3.marketwire.com/docs/1073217a.jpg

{kind=link}

KEY RESULTS

Resource Update

Additional drilling since the April 2016 Resource Report has updated the resources as follows:

| T-Zone 2.5 g/t Cut-off | |||||||||||

| Resource Category |

Cut-off | Tonnage | Grade | Metal | |||||||

| 4E | Pt | Pd | Au | Rh | 4E | Cu | Ni | 4E | |||

| g/t | Mt | g/t | g/t | g/t | g/t | g/t | % | % | Kg | Moz | |

| Indicated | 2.5 | 31.540 | 1.13 | 1.90 | 0.81 | 0.04 | 3.88 | 0.16 | 0.08 | 122,375 | 3.934 |

| Inferred | 2.5 | 19.917 | 1.10 | 1.86 | 0.80 | 0.03 | 3.79 | 0.16 | 0.08 | 75,485 | 2.427 |

| F-Zone 2.5 g/t Cut-off | |||||||||||

| Resource Category |

Cut-off | Tonnage | Grade | Metal | |||||||

| 4E | Pt | Pd | Au | Rh | 4E | Cu | Ni | 4E | |||

| g/t | Mt | g/t | g/t | g/t | g/t | g/t | % | % | Kg | Moz | |

| Indicated | 2.5 | 186.725 | 1.05 | 2.23 | 0.17 | 0.04 | 3.49 | 0.07 | 0.16 | 651,670 | 20.952 |

| Inferred | 2.5 | 77.295 | 1.01 | 2.16 | 0.17 | 0.03 | 3.37 | 0.04 | 0.12 | 260,484 | 8.375 |

The Total Mineral Resource is summarized below:

| Waterberg Total 2.5 g/t Cut-off | |||||||||||

| Resource Category |

Cut-off | Tonnage | Grade | Metal | |||||||

| 4E | Pt | Pd | Au | Rh | 4E | Cu | Ni | 4E | |||

| g/t | Mt | g/t | g/t | g/t | g/t | g/t | % | % | Kg | Moz | |

| Indicated | 2.5 | 218.265 | 1.06 | 2.18 | 0.26 | 0.04 | 3.55 | 0.08 | 0.15 | 774,045 | 24.886 |

| Inferred | 2.5 | 97.212 | 1.03 | 2.10 | 0.30 | 0.03 | 3.46 | 0.06 | 0.11 | 335,969 | 10.802 |

4E = Platinum Group Elements (Pt+Pd+Rh+Au). The cut-offs for mineral resources have been established by a qualified person after a review of potential operating costs and other factors. The mineral resources stated above are shown on a 100% basis, that is, for the Waterberg Project as a whole entity. Conversion Factor used - kg to oz = 32.15076. Numbers may not add due to rounding. Resources do not have demonstrated economic viability. A 5% and 7% geological loss has been applied to the Indicated and Inferred categories respectively. Effective Date Oct 17, 2016. Metal prices used in the reserve estimate are as follows based on a 3-year trailing average (as at July 31/2016) in accordance with U.S. Securities and Exchange Commission ("SEC") guidance for the assessment of resources; US$1,212/oz Pt, US$710/oz Pd, US$1229/oz Au, US$984/oz Rh, US$6.10/lb Ni, US$2.56/lb Cu, US$/ZAR15.

Total aggregate mineral resources at Waterberg on a 100% project basis have increased slightly since those reported in April 2016. Inferred category resources have decreased to an estimated 10.8 million 4E ounces from 11.71 million ounces 4E Inferred in April, 2016. Indicated category resources have increased to an estimated 24.9 million 4E ounces, from 23.9 million 4E ounces Indicated in April 2016:

- The mineral resources are classified in accordance with the SAMREC standards. There are certain differences with the "CIM Standards on Mineral Resources and Reserves"; however, in this case the QP believes the differences are not material and the standards may be considered the same. Mineral resources that are not mineral reserves do not have demonstrated economic viability and Inferred resources have a high degree of uncertainty.

- The mineral resources are provided on a 100% project basis and Inferred and Indicated categories are separate and the estimates have an effective date of 17 October 2016.

- A cut-off grade of 2.5 g/t 4E for both the T and the F-Zones is applied to the selected base case mineral resources.

- Cut off for the T and the F-Zones considered costs, smelter discounts, concentrator recoveries from previous engineering work completed on the property by the Company. The resource model was cut-off at an arbitrary depth of 1,250 meters, although intercepts of the deposit do occur below this depth.

- Mineral resources were completed by Mr. CJ Muller of CJM Consulting.

- Mineral resources were estimated using kriging methods for geological domains created in Datamine from 303 original holes and 483 deflections. A process of geological modelling and creation of grade shells using indicating kriging was completed in the estimation process.

- The estimation of mineral resources has taken into account environmental, permitting and legal, title, and taxation, socio-economic, marketing and political factors.

- The mineral resources may be materially affected by metals prices, exchange rates, labor costs, electricity supply issues or many other factors detailed in the Company's Annual Information Form.

- The data that formed the basis of the estimate are the drill holes drilled by Platinum Group, which consist of geological logs, the drill hole collars surveys, the downhole surveys and the assay data. The area where each layer was present was delineated after examination of the intersections in the various drill holes.

- There is no guarantee that all or any part of the mineral resource not included in the current reserves will be upgraded and converted to a mineral reserve.

Reserves

Reserves are stated on a 100% Project Basis. Reserves are a subset of the Indicated resources and the mine plan was developed from the October 2016 resource model above and includes mine modifying factors such as geological losses, dilution, development overbreak, mine design factors, in stope losses and the extraction ratio from the mining methods applied to the T and F-Zones.

The independent Qualified Person for the Statement of Reserves is Mr. RL Goosen (WorleyParsons RSA (Pty) Ltd Trading as Advisian). The table below shows the prill splits, which are calculated using the individual metal grades reported as a percentage of the total 4E grade. There are no Inferred mineral resources included in the reserves.

Prill Splits

| Prill Split | Grade | |||||

| Zone | Pt | Pd | Au | Rh | Cu | Ni |

| % | % | % | % | % | % | |

| T-Zone | 29 | 49 | 21 | 1 | 0.16 | 0.08 |

| F-Zone | 30 | 64 | 5 | 1 | 0.07 | 0.16 |

Probable Mineral Reserve at 2.5 g/t 4E Cut-off- Tonnage and Grades

| Waterberg Probable Mineral Reserve - Tonnage and Grades | |||||||||

| Zone | Mt | Cut-off grade (g/t) |

Pt (g/t) |

Pd (g/t) |

Au (g/t) |

Rh (g/t) |

4E (g/t) |

Cu (%) |

Ni (%) |

| T-Zone | 16.5 | 2.5 | 1.14 | 1.93 | 0.83 | 0.04 | 3.94 | 0.16 | 0.08 |

| F-Zone | 86.2 | 2.5 | 1.11 | 2.36 | 0.18 | 0.04 | 3.69 | 0.07 | 0.16 |

| Total | 102.7 | 2.5 | 1.11 | 2.29 | 0.29 | 0.04 | 3.73 | 0.08 | 0.15 |

Probable Mineral Reserve at 2.5 g/t 4E Cut-off- Contained Metal

| Waterberg Probable Mineral Reserve - Contained Metal | |||||||||

| Zone | Mt | Pt (Moz) |

Pd (Moz) |

Au (Moz) |

Rh (Moz) |

4E (Moz) |

4E content (kg) |

Cu (Mlb) |

Ni (Mlb) |

| T-Zone | 16.5 | 0.61 | 1.03 | 0.44 | 0.02 | 2.09 | 65,097 | 58.21 | 29.10 |

| F-Zone | 86.2 | 3.07 | 6.54 | 0.51 | 0.10 | 10.22 | 318,007 | 132.97 | 303.94 |

| Total | 102.7 | 3.67 | 7.57 | 0.95 | 0.12 | 12.32 | 383,103 | 191.18 | 333.04 |

Reasonable prospects of economic extraction were determined with the following assumptions: Metal prices used in the reserve estimate are as follows based on a 3-year trailing average (as at July 31/2016) in accordance with U.S. Securities and Exchange Commission ("SEC") guidance for the assessment of resources and reserves; US$1,212/oz Pt, US$710/oz Pd, US$1229/oz Au, US$984/oz Rh, US$6.10/lb Ni, US$2.56/lb Cu, US$/ZAR15. Smelter payability of 85% was estimated for 4E and 73% for Cu and 68% for Ni. The effective date is October 17, 2016. A 2.5 g/t Cut-off was used and checked against a pay-limit calculation. Independent Qualified Person for the Statement of Reserves is Mr. RL Goosen (WorleyParsons RSA (Pty) Ltd Trading as Advisian). The mineral reserves may be materially affected by changes in metals prices, exchange rates, labor costs, electricity supply issues or many other factors. See Risk Factors in 43-101 report on www.sedar.com and the Company's Annual Information Form. The reserves are estimated under SAMREC with no material difference to the CIM 2014 definitions in this case.

The estimation of mineral reserves has taken into account environmental, permitting and legal, title, taxation, socio-economic, marketing and political factors. Based on the cut-off grade and a maximum depth cut-off of 1,250 meters the Probable reserve will support an 18 year mine life.

PROJECT PFS RESULTS

The PFS results validate the PEA with similar capital costs in USD, increased production profile (from 655,000 3E ounces/yr PEA to 744,000/yr 4E ounces PFS) and an increase in sustaining capital. Optimization of the mine plan and working on reducing underground sustaining development capital will be part of the upcoming Feasibility Study.

PROJECT MODEL TIMELINE

The project time line includes a construction decision following the completion of a FS and first production 3 years later. Under the PFS model, first production is estimated as mid-2021, if the FS is completed at the end of 2017 and a mining right and other permits are granted as planned. Final reef tonnes are scheduled to be mined in 2038.

CAPITAL COSTS

Capital costs to full production and peak funding of the project are estimated in Rand 2016 terms. Peak Funding is estimated at US$914 million. The costs are estimated in USD at 15R/1USD with a flat exchange rate. Escalation of costs in Rand terms are estimated to be mostly offset over time by future Rand devaluation.

TOTAL CAPITAL

| Facility Code |

Facility Description | To Full Production ZAR (M) |

Sustaining Capital ZAR (M) |

To Full Production USD (M) |

Sustaining Capital USD (M) |

| 2000 | Underground Mining | 6,092 | 9,766 | 406 | 651 |

| 3000 | Concentrator | 2,850 | 159 | 190 | 11 |

| 4000 | Shared Services & Infrastructure | 1,063 | 43 | 71 | 03 |

| 5000 | Regional Infrastructure | 2,566 | 0 | 171 | 0 |

| 6000 | Site Support Services | 691 | 67 | 46 | 04 |

| 7000 | Project Delivery Management | 1,399 | 147 | 93 | 10 |

| 8000 | Other Capitalised Costs | 246 | 83 | 16 | 06 |

| 9000 | Contingency | 999 | 1,202 | 67 | 80 |

| Total Capital | 15,906 | 11,468 | 1,060 | 765 | |

The estimates for the scope of work, within the given battery limits, and subject to the qualifications, assumptions and exclusions contained in the PFS, are considered to be within the accuracy range required for a PFS of +25%. Monte Carlo simulation was used to provide a 12% contingency that was used in the estimates.

Waterberg 2016 PFS Results Details

| Item | Units | Total |

| Mined and Processed | Mtpa | 7.20 |

| Platinum | g/t | 1.11 |

| Palladium | g/t | 2.29 |

| Gold | g/t | 0.29 |

| Rhodium | g/t | 0.04 |

| 4E | g/t | 3.73 |

| Copper | % | 0.08 |

| Nickel | % | 0.15 |

| Recoveries | ||

| Platinum | % | 82.5% |

| Palladium | % | 83.2% |

| Gold | % | 75.3% |

| Rhodium | % | 59.4% |

| 4E | % | 82.1% |

| Copper | % | 87.9% |

| Nickel | % | 48.8% |

| Produced in Concentrate | ||

| Concentrate | ktpa | 285 |

| Platinum | g/t | 24.2 |

| Palladium | g/t | 51.5 |

| Gold | g/t | 4.9 |

| Rhodium | g/t | 0.6 |

| 4E | g/t | 81 |

| Copper | % | 1.9 |

| Nickel | % | 1.8 |

| Recovered Metal in Concentrate | ||

| Platinum | kozpa | 222 |

| Palladium | kozpa | 472 |

| Gold | kozpa | 45 |

| Rhodium | kozpa | 6 |

| 4E | kozpa | 744 |

| Copper | Mlbpa | 11 |

| Nickel | Mlbpa | 12 |

KEY ASSUMPTIONS

Economic Assumptions

| Parameter | Unit | 3 Year Trailing Average |

Investment Bank Consensus Price |

| Platinum Palladium Gold Rhodium T and F Combined Basket (4E) Nickel Copper |

USD/oz USD/oz USD/oz USD/oz USD/oz USD/lb USD/lb |

1,212 710 1,229 984 899 6.10 2.56 |

1,213 800 1,300 1,000 960 7.50 2.90 |

| Base Metals Refining Charge Copper Refining Charge Nickel Refinery Charge |

% Gross Sales Pay % Gross Sales Pay % Gross Sales Pay |

85% 73% 68% |

|

FINANCIAL RESULTS

Average Life of Mine ("LOM") Operating Cost Rates and Totals per Area in ZAR and USD

| Average LOM (ZAR/t) |

Total LOM (ZAR M) |

Average LOM (USD/t) |

Total LOM (USD M) |

|

| Mining | R 271.90 | R 27,915 | $ 18.13 | $ 1,861 |

| Engineering & Infrastructure | R 107.49 | R 11,036 | $ 7.17 | $ 736 |

| General & Admin | R 40.71 | R 4,180 | $ 2.71 | $ 279 |

| Process | R 154.52 | R 15,864 | $ 10.30 | $ 1,058 |

| Total OPEX Cost | R 574.62 | R 58,994 | $ 38.31 | $ 3,933 |

4E Cash Costs before and after Credits and Costs

| Item | US$/oz 4E in Concentrate | ||

| Life-of-Mine Average |

5-Year Average 2022 - 2026 |

10-Year Average 2022 - 2031 |

|

| Mine Site Cash Cost | 389 | 390 | 374 |

| Nickel Credits Copper Credits |

98 42 |

97 40 |

98 40 |

| Total Mine Cash Costs After Credits | 248 | 253 | 236 |

| Realisation cost (smelter "cost", transport) | 232 | 224 | 231 |

| Total Cash Costs After Credits | 481 | 477 | 467 |

Financial Results Three Year Trailing Average Price Deck 15R/1USD Flat

| Item | Discount Rate |

ZAR Millions (Before Tax) |

ZAR Millions (After Tax) |

USD Millions (Before Tax) |

USD Millions (After Tax) |

| Net Present Value | Undiscounted 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% |

36,096 18,213 12,666 8,565 5,519 3,249 1,555 |

25,042 11,883 7,808 4,805 2,584 939 -278 |

2,406 1,214 844 571 368 217 104 |

1,669 792 520 320 172 62 -19 |

| Internal Rate of Return Project Payback Period (Years) from 2017 |

16.6% 10 |

13.5% 10 |

16.6% 10 |

13.5% 10 |

|

Investment Bank Consensus Price Deck

| Item | Discount Rate |

Before Tax (ZAR M) |

After Tax (ZAR M) |

Before Tax (USD M) |

After Tax (USD M) |

| Net Present Value | Undiscounted 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% |

45,781 24,180 17,426 12,402 8,641 5,812 3,676 |

31,946 16,184 11,263 7,610 4,884 2,842 1,311 |

3,052 1,612 1,162 827 576 387 245 |

2,130 1,079 750 507 325 189 87 |

| Internal Rate of Return Project Payback Period (Years) from 2017 |

19.8% 9 |

16.3% 9 |

19.8% 9 |

16.3% 9 |

|

Sensitivity Analysis - Post Tax Three Year Trailing Average Price Deck 15R/1USD Flat

| Parameter | Change in Parameter |

Change in Parameter |

Change in Parameter |

Change in Parameter |

Change in Parameter |

| Metal Prices IRR (post-tax) NPV (8% Discount) (R000) NPV (8% Discount) ($000) |

-20% 5% -2,467 -164 |

-10% 10% 1,211 67 |

0% 13.5% 4,805 320 |

10% 17% 8,344 556 |

20% 20% 11,854 790 |

| Head Grade IRR (post-tax) NPV (8% Discount) (R000) NPV (8% Discount) ($000) |

-20% 6% -1,513 -101 |

-10% 10% 1,562 104 |

0% 13.5% 4,805 320 |

10% 16% 7,562 504 |

20% 19% 10,505 700 |

| Capex IRR (post-tax) NPV (8% Discount) (R000) NPV (8% Discount) ($000) |

-20% 17% 8,161 544 |

-10% 15% 6,484 432 |

0% 13.5% 4,805 320 |

10% 12% 3,109 207 |

20% 10% 1,395 93 |

| Opex IRR (post-tax) NPV (8% Discount) (R000) NPV (8% Discount) ($000) |

-20% 18% 7,435 496 |

-10% 16% 6,121 408 |

0% 13.5% 4,805 320 |

10% 12% 3,246 216 |

20% 10% 2,124 142 |

CONSTRUCTION AND DEVELOPMENT METHODOLOGY

The immediate next steps for the Waterberg Project are the development of a mining right application and working towards a FS. The PFS specifies that the project will utilize an EPCM contractor and a mining contractor for the development of the mine, overseen by an experienced in-house Platinum Group owners' team. Initial development is planned with contractors with a later takeover for mining by an owners' team. Equipment operators will be trained at an existing MQA certified training center developed and owned by Platinum Group.

PLANNED MINING METHODS

The mining blocks of the Waterberg deposits occur at depths from 140 meters to 1,250 meters along 8,000 meters of strike length of reserves. The deposit is known from drill intercepts to continue below 1,250 meters and to extend for over 13,000 meters of strike length.

Access to the mining complex is planned by three decline ramp clusters. Decline ramps have advantages over vertical shafts in terms of capital cost, and importantly, time. Declines to the depths of the top of the Waterberg deposit can be developed over 24-36 months whereas vertical shafts, shaft infrastructure and equipping can take six to seven years.

Mining will be completed by safe, efficient fully mechanized methods and the dip and thickness of the zones are driving the mining method selection. A fleet of approximately 400 trackless machines including drill rigs, loaders, dump trucks and other trackless machines will be used for mining and development. A minimum mining width has been set at three meters so that all mining can be fully mechanized, safe and efficient.

| Mining Method | Vertical Mining Height |

Dip of the Reef |

Key Advantages | |

| Blind Longitudinal Retreat | 3 - 15m | ≤35° | On reef development. Good grade, extraction. | |

| Sub-level Open Stoping - Longitudinal | 3 - 15m | >35° | On reef development. Good extraction. Bulk and low cost. | |

| Sub-level Open Stoping - Transverse | >15m | >35° | Bulk method. High efficiency, large tonnage, good extraction, ultra-low cost. | |

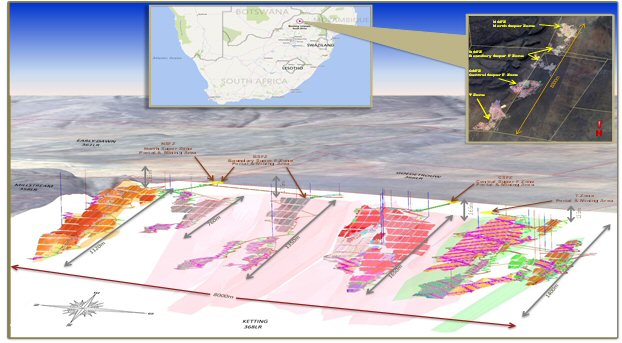

Portal and Underground Layouts (October 17, 2016): http://media3.marketwire.com/docs/1073217b.jpg

{kind=link}

The mine utilizes a large supply of new mechanized trackless mobile equipment for mining and feed ore onto large conveyors from underground to the processing plant. The mine will rely on both the T and the F reef from more than one portal to make the tonnage profile steady state of 600,000 tonnes per month.

METALLURGICAL RECOVERY AND PROCESSING

The flotation test work indicated that the Waterberg ores are amenable to treatment by conventional flotation without the need for re-grinding. A standard flotation concentrator can be used to produce a saleable concentrate, at a 4E grade of no less than 80 g/t, with no deleterious products. A 4E recovery rate in excess of 80% is expected at the proposed mill feed grades.

Metallurgical test work on the Waterberg ores by SGS, Mintek and DRA has focused on recovery of 4E platinum group elements and copper-nickel sulphides with the objective of producing a high grade concentrate attractive for smelting in South Africa.

The processing plant is designed in two 300,000 tonne/month Mill-Float in two cycles "MF-2" standard platinum industry modules for ramp-up and operational flexibility. A JOGMEC reagent circuit with some opportunity for increased recovery has also been tested. The plant modules are designed to accept T reef, F reef or a blended combination. The ore types can be co-mingled without negatively affecting recoveries.

INFRASTRUCTURE

The main infrastructure requirements for the Waterberg Project are access roads, tailings storage, water management, power supply and process plant to service and treat the targeted mine production.

The Waterberg Project is situated in a remote area and will require approximately 32 km of existing unpaved roads to be surfaced.

BULK WATER SUPPLY

A combination of sewage effluent together with groundwater is considered the most viable solution to meet the proposed mining schedule. Several available options were considered including a pipeline to be developed for several users to the south, including for other proposed and active mines. This option was not chosen as it is considered to have greater risk due to the large number of parties involved. Sufficient water sources for the project were identified and early discussions for the preferred arrangements were positive.

BULK POWER SUPPLY

The updated electricity supply plan compiled by Eskom provides for the establishment of two 77 km long 132kV overhead lines from the Eskom Burotho 400/132kV main transmission substation.

The development of the abovementioned infrastructure will be done in conjunction with Eskom on a self-build basis and this work is already in an advanced stage including the application for permits for the proposed power line.

METALS MARKETS AND OFFTAKE

The Waterberg Project will produce a flotation concentrate from the processing plant which is assumed to be sold or toll treated into the local South African market.

Production of up to 285,000 tonnes of concentrate per annum will be available at peak production. The concentrate will contain approximately 80 g/t 4E's plus copper at between 1% and 9.2% and nickel at between 1.1% and 5% copper.

The concentrate does not contain any penalty elements such as chrome and is rich in sulphur, thus making it a desirable concentrate to blend with other high chrome concentrates.

No formal marketing studies have been conducted for this study nor have the local smelter and refinery operators been formally contacted to understand the appetite in the local industry to treat the concentrate to be produced from the project. Informal indications from smelters are that the concentrate is attractive.

Based on the large volume of concentrate and the significantly lower operating cost of the metal without the smelter discount, the consideration of production of an onsite smelter matte or combination with other Northern Limb material for further critical mass is recommended. The company will consider this recommendation with its partners JOGMEC and Mnombo.

LABOUR, SOCIAL AND PERMITTING

The Waterberg Project will create safe long term jobs with transferable mechanized equipment operations skills for a large part of the work force. The increased safety and ability to create good paying well trained jobs is an attractive community benefit. The social license to operate has been a focus of the company with ongoing positive meetings and interactions. The next stage of the project will involve the development of a Social and Labour Plan as part of the mining right application. The project involves normal measures for the protection of the environment similar to other platinum mining operations.

2016 AND 2017 PROGRAMS FUNDED

During 2015, JOGMEC committed to fund US$20 million of project work at Waterberg. Approximately US$8 million of that commitment remains to be completed and will fund 100% of the costs for the balance of 2016 and into 2017.

QUALIFIED PERSONS

The following Qualified Persons have completed work in preparation of the PFS and are responsible for the contents:

- Independent Engineering Qualified Person:

Mr. Robert L Goosen

(B.Eng. (Mining Engineering)) Pr. Eng. (ECSA)

Advisian/WorleyParsons Group - Independent Geological Qualified Person:

Mr. Charles J Muller

(B.Sc. (Hons) Geology) Pr. Sci. Nat.

CJM Consulting (Pty) Ltd - Independent Engineering Qualified Person:

Mr. Gordon I. Cunningham

B. Eng. (Chemical), Pr. Eng. (ECSA), Professional association to FSAIMM

Turnberry Projects (Pty) Ltd.

This press release has been reviewed and approved by R. Michael Jones, P.Eng., a non-independent Qualified Person and the CEO of the Company. He has verified the technical information for disclosure in this press release by reviewing the work of the QPs on a test basis, visiting the site and meeting with the project QPs through the development of the PFS.

DATA VERIFICATION, QUALITY ASSURANCE AND CONTROL

Scientific and Technical Information in this Press Release related to mineral resources has been reviewed and approved by Charles J Muller, (BScHons) Pr Sci Nat (Reg. No 400201/04), an independent consulting geologist and resource estimator of CJM Consulting, an independent qualified person as defined in National Instrument 43-101 -Standards of Disclosure for Mineral Projects ("NI 43-101"). He has verified the data by reviewing the detailed assay and geological information and metallurgical work on the Waterberg deposit. He is satisfied that the data is appropriate for the resource estimate by reviewing the core, assay certificates and quality control information as well as reviewing the procedures on sampling, chain of custody and data base records of the Platinum Group exploration team.

Base metals and other major elements were determined by multi acid digestion with Inductively Coupled Plasma ("ICP") finish and PGEs were determined by conventional fire assay and ICP finish. Setpoint Laboratories is an experienced ISO 17025 SANAS accredited laboratory in assaying and have utilized a standard quality control system including the use of standards. Bureau Veritas South Africa and Genalysis of Australia with similar standards and approaches have been used for assays and umpire checks. Platinum Group utilized a well-documented system of inserting blanks and standards into the assay stream and has a strict chain of custody and independent lab re-check system for quality control. Details are available in the NI 43 101 reports on the project at www.sedar.com and www.platinumgroupmetals.net.

The independent QPs for the PFS (CJ Muller, GI Cunningham and RL Goosen) have visited the Waterberg property for personal inspection during 2016. Mr. RL Goosen last visited the site on 13 October 2016, Mr. GI Cunningham on 13 October 2016 and Mr. CJ Muller on 29 March 2016. They all have undertaken due diligence with respect to the PTM data. Other than as specified below they jointly take responsibility for the report.

- Charles J Muller - Geology and Mineral Resource Estimation

- Robert L Goosen - Reserve Estimation, Mining and Infrastructure

- Gordon I Cunningham - Metallurgy, Metals Markets, Offtake, Capital cost and financial model

The QPs have verified the data sufficiently for the reporting of resources, reserves and this Pre-Feasibility Study. The QPs have reviewed and approved their relevant section of this press release.

OPPORTUNITIES

- The company plans to work towards optimization of the mine plan, development plan and waste development plan for ventilation with the objective of reducing sustaining capital in the FS stage.

- Further drilling will be completed with the objective to upgrade some of the resources and the deposit remains open. A longer mine life will also be targeted in the high grade T reef areas. High grade thickness areas in the F reef will also receive targeted drilling with the objective of increasing definition for the FS mine plan.

- Further metallurgical work will be completed in the FS including the potential for increased recoveries using the JOGMEC circuit.

- The Waterberg concentrate is attractive for smelting and is of large strategic scale importance to the industry.

RISKS

- The project at a PFS stage has all of the normal mining projects risks including but not limited to, estimation risk for the resources and reserves, recovery risks, capital cost and operating cost estimation risks, permitting and community and surface rights access risk.

- Government regulation stability and amendments of the fiscal regime is an additional risk.

- Waterberg is a large green-fields project and final off-take of the proposed metal is yet to be negotiated for a large volume of concentrate.

ABOUT PLATINUM GROUP METALS LTD.

Platinum Group, based in Johannesburg, South Africa and Vancouver, Canada, has a successful track record with more than 20 years of experience in exploration, mine discovery, mine construction and mine operations.

Formed in 2002, Platinum Group holds significant mineral rights in the Bushveld Igneous Complex of South Africa, which is host to over 70% of the world's primary platinum production. The Company is currently focused on ramping up the Maseve Mine, its first near-surface platinum mine, to commercial production.

Platinum Group has expanded its exploration and development efforts on the North Limb of the Bushveld Complex on the Waterberg Project. Waterberg represents a new bulk type of platinum, palladium and gold deposit.

On behalf of the Board of Platinum Group Metals Ltd.

"R. Michael Jones"

President and CEO

Disclosure

The Toronto Stock Exchange and the NYSE MKT LLC have not reviewed and do not accept responsibility for the accuracy or adequacy of this news release, which has been prepared by management.

This press release contains forward-looking information within the meaning of Canadian securities laws and forward-looking statements within the meaning of U.S. securities laws (collectively "forward-looking statements"). Forward-looking statements are typically identified by words such as: believe, expect, anticipate, intend, estimate, plans, postulate and similar expressions, or are those, which, by their nature, refer to future events. All statements that are not statements of historical fact are forward-looking statements. Forward-looking statements in this press release include, without limitation, the projections and assumptions relating to future events that are contained in the PFS, including, without limitation NPV, IRR, costs, potential production of the Waterberg Project and other operational and economic projections with respect to the Waterberg Project; future activities at Waterberg and the funding of such activities; trends in metal prices; potential future market conditions; the Company's overall capital requirements and future capital raising activities, plans and estimates regarding exploration, studies, development, construction and production on the Company's properties, other economic projections and the Company's outlook. Statements of mineral resources and mineral reserves also constitute forward-looking statements to the extent they represent estimates of mineralization that will be encountered on a property and/or estimates regarding future costs, revenues and other matters. Although the Company believes the forward-looking statements in this press release are reasonable, it can give no assurance that the expectations and assumptions in such statements will prove to be correct. The Company cautions investors that any forward-looking statements by the Company are not guarantees of future results or performance, and that actual results may differ materially from those in forward-looking statements as a result of various factors, including; the Company's capital requirements may exceed its current expectations; the uncertainty of cost, operational and economic projections; the ability of the Company to negotiate and complete future funding transactions; variations in market conditions; the nature, quality and quantity of any mineral deposits that may be located; metal prices; other prices and costs; currency exchange rates; the Company's ability to obtain any necessary permits, consents or authorizations required for its activities; the Company's ability to produce minerals from its properties successfully or profitably, to continue its projected growth, or to be fully able to implement its business strategies; and other risk factors described in the Company's shelf prospectus and registration statement, Form 40-F annual report, annual information form and other filings with the Securities and Exchange Commission and Canadian securities regulators, which may be viewed at www.sec.gov and www.sedar.com, respectively.

This press release also includes a reference to mineral resources and mineral reserves. The estimation of resources and reserves is inherently uncertain and involves judgement. Mineral resources that are not reserves do not have demonstrated economic viability. Judgements associated with geology, tonnage grades in place and that can be mined may prove to be unreliable and inaccurate. Fluctuations in metals prices, exchange rates, labour costs and government regulations among other things may materially affect resources and reserves. The company does not yet have a right to mine the reported resources and reserves and there can be no assurance that the company will convert its prospecting permits to a mining right.

Cautionary Note to U.S. and other Investors

Estimates of mineralization and other technical information included or referenced in this press release have been prepared in accordance with NI 43-101. The definitions of proven and probable reserves used in NI 43-101 differ from the definitions in SEC Industry Guide 7. Under SEC Industry Guide 7 standards, a "final" or "bankable" feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority. As a result, the reserves reported by the Company in accordance with NI 43-101 may not qualify as "reserves" under SEC standards. In addition, the terms "mineral resource", "measured mineral resource", "indicated mineral resource" and "inferred mineral resource" are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and normally are not permitted to be used in reports and registration statements filed with the SEC. Mineral resources that are not mineral reserves do not have demonstrated economic viability. Investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into reserves. "inferred mineral resources" have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian securities laws, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Additionally, disclosure of "contained ounces" in a resource is permitted disclosure under Canadian securities laws; however, the SEC normally only permits issuers to report mineralization that does not constitute "reserves" by SEC standards as in place tonnage and grade without reference to unit measurements. Accordingly, information contained or referenced in this press release containing descriptions of the Company's mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements of United States federal securities laws and the rules and regulations thereunder.

Contact Information:

or Kris Begic, VP Corporate Development

Platinum Group Metals Ltd., Vancouver

Tel: (604) 899-5450 / Toll Free: (866) 899-5450

www.platinumgroupmetals.net