Urges Shareholders to Vote for All of Whitestone’s Highly Qualified Trustees on the WHITE Proxy Card

Since CEO Change in 2022, Whitestone Has Executed on a Successful Strategy for Value Creation and Delivered Among the Highest REIT Performing Shareholder Returns

Erez Waging Unnecessary, Self-Serving and Misguided Proxy Contest

HOUSTON, April 05, 2024 (GLOBE NEWSWIRE) -- Whitestone REIT (NYSE: WSR) (“Whitestone” or the “Company”) today announced that it has filed its definitive proxy materials with the Securities and Exchange Commission (“SEC”) in connection with its 2024 Annual Meeting of Stockholders scheduled to be held on May 14th, 2024. Shareholders of record as of February 21, 2024, will be entitled to vote at the meeting.

In conjunction with the definitive proxy filing, Whitestone has mailed a letter to the Company’s shareholders. Highlights from the letter include:

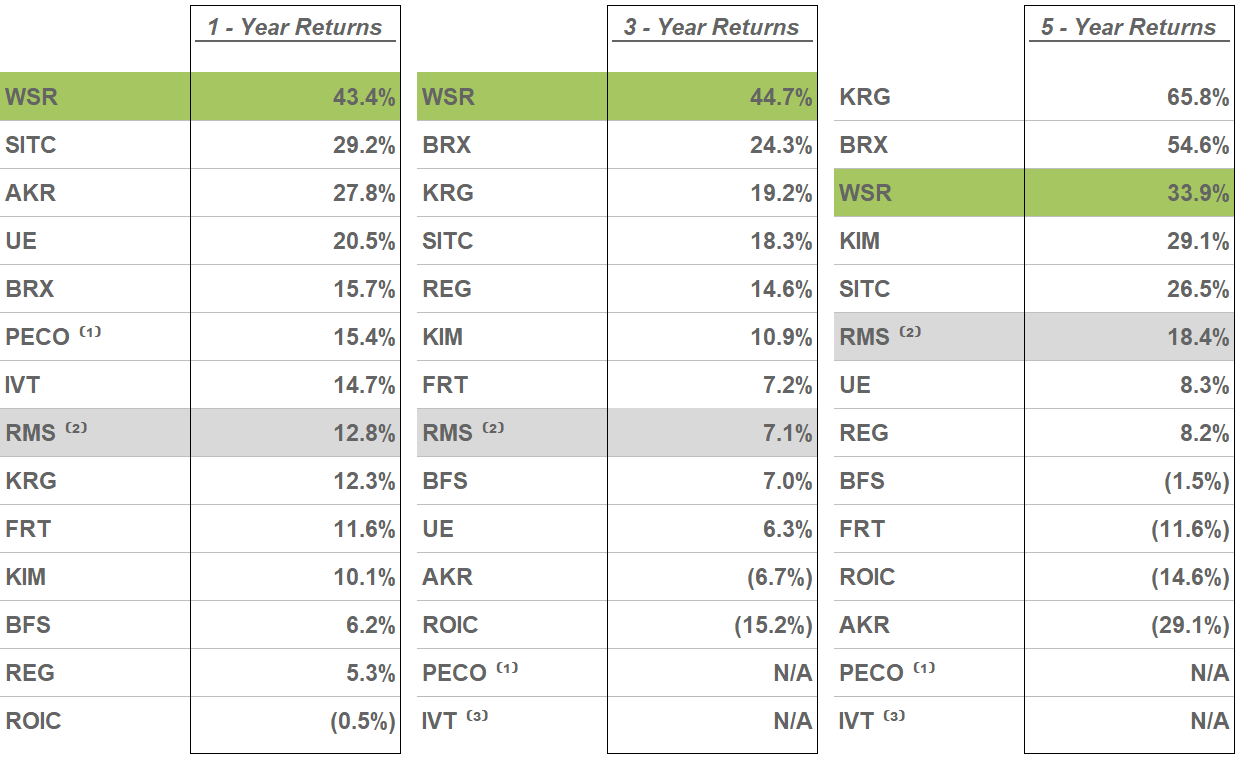

- Stock Outperformance. Whitestone’s stock has continued to outperform its peers and the MSCI US REIT Index. Since changing CEOs in 2022, Whitestone has the #1 performing stock on a 1-year and 3-year Total Shareholder Return basis and has outperformed on a 5-year basis when compared to peers and the MSCI US REIT Index

- High Same Store NOI. Whitestone has achieved some of the highest Same Store Net Operating Income (NOI) growth among peers since 2022, driven by a high-quality portfolio and a management team that is laser-focused on delivering consistent results

- Strong Core FFO Outlook. Whitestone is positioned to continue delivering strong results with the midpoint of 2024 guidance indicating 11% year over year Core Funds From Operations (FFO) per share growth; and

- No Value Added from Erez. We have concerns regarding Erez Asset Management’s short-term focus, failure to bring forward any new, value-enhancing ideas for Whitestone and we believe the election of Erez’s nominees would disrupt Whitestone’s substantial business momentum to-date and diminish the quality and strength of the Board of Trustees

Whitestone’s definitive proxy materials and other materials regarding the Board’s recommendation for the 2024 Annual Meeting can be found at: https://ir.whitestonereit.com/financial-reporting/documents/default.aspx

The full text of the letter being mailed to shareholders follows:

Dear Fellow Shareholder,

Led by Whitestone’s revised strategy and the leadership of our CEO David Holeman since January 2022, we are pleased to share that our Company has been consistently executing on a strategy that is driving value and delivering superior shareholder returns. Today, Whitestone’s Total Shareholder Return performance is the #1 stock amongst our peers on a 1-year and 3-year basis and has outperformed on a 5-year basis. Our Revenue, Same Store NOI, Occupancy Rate, Annual Net Effective Average Base Rent and Leasing metrics are all up while our leverage is down. We’ve also successfully resolved recent litigation, which provides the Company an additional tailwind to improve its balance sheet. Simply put, the plan outlined by Mr. Holeman when he took over as CEO and overseen by our Board is working and our objective is to continue executing on our current plan to deliver shareholder value.

However, this wasn’t always the case before 2022. Our prior CEO was putting his own interest ahead of shareholders, unable to lead effectively and his impact on our Company’s performance was detrimental. Accordingly, your Board took action in a deliberate and decisive manner and terminated the prior CEO for cause. Under our new plan, we have paved the path forward to maximize value for Whitestone shareholders. Since appointing Mr. Holeman as CEO, the Board has been better aligned with our shareholders through governance improvements and has undergone extensive refreshment with three new trustees, each bringing unique and differentiated perspectives into our boardroom. The management team has been focused on improving operational and financial performance, strengthening our balance sheet to reduce leverage and monetizing our equity investment in the Pillarstone Partnership.

Despite our superior performance, Erez Asset Management (“Erez”), a new opportunistic asset manager with a very limited track record, is attempting to disrupt our progress. Instead of proposing constructive ideas to build on our progress and further enhance value for all shareholders, Erez has demanded a change in Whitestone’s Board with the sole purpose of embarking on an immediate sale or liquidation of our Company without offering any substantive operational, financial or strategic ideas for improvement. While the Whitestone Board is open to all avenues to drive shareholder value, including evaluating a sale of the Company, given the current financial market conditions and in light of the momentum our Company is realizing, we believe that Erez is prioritizing short term gains at the expense of long-term value creation. Erez has nominated two individuals, Bruce Schanzer and Catherine Clark. Our Board thoroughly evaluated and interviewed each candidate and concluded that they lacked additive skills and have no history of creating shareholder value at other companies they have been affiliated with. The facts could not be clearer: Erez’s campaign is not in the best interest of all shareholders.

Under the leadership of your Board and experienced management team, the Company was its own change agent, implementing a deliberate and long-term strategy that has delivered industry leading total shareholder returns and positioned Whitestone for an even brighter future. Our results confirm that this is the right strategy for Whitestone, and the financial results are the product of our clearly defined strategy and relentless execution.

Erez’s campaign unnecessarily risks derailing our trajectory, stalling our momentum and potentially destroying the value we have created for you.

A vote for Whitestone’s trustees is a vote for the right strategy, the right execution and the right Board. Voting for each of Whitestone’s nominees on the WHITE proxy card is in the best interests of all shareholders.

IN 2022, WHITESTONE APPOINTED NEW LEADERSHIP TO DRIVE OUR NEW STRATEGY

FOR THE BENEFIT OF ALL SHAREHOLDERS

CEO David Holeman began 2022 by assembling the right team to lead Whitestone, and ensuring that all employees were focused on the Company’s core strategy:

By focusing on community and convenience with service-oriented tenants in high-income, sun belt-located shopping centers, Whitestone can achieve earnings growth at or near the top of its peer set.

A number of specific actions were taken in order to drive greater performance:

- Increased accountability

- Streamlined and strengthened the regional leasing and property management teams with clear goals and priorities

- Eliminated micro-management, allowing for faster and better execution

- Restored key relationships within the real estate community, especially with the brokers, dramatically increasing transaction flow

- Focused on the right talent that ultimately resulted in reducing headcount by over 25% versus 2019

These actions resulted in higher morale throughout the organization with employees having more ownership and effective tools for success, and clear objectives that were aligned with the management team, resulting in greater productivity.

These actions have produced substantial results:

- Occupancy has increased 290 basis points (year-end 2021 to year-end 2023), bringing occupancy up to a record 94.2%

- Straight line leasing spreads have now exceeded 17% for seven consecutive quarters

- Same Store Net Operating Income grew 7.9% in 2022, followed by 2.7% in 2023, amongst the highest within the peer group

In addition to operational improvements, management aggressively strengthened the Company’s balance sheet by:

- Amending and extending the Company’s $515 million credit facility, ensuring that the bulk of the Company maturities extended to 2027 and beyond

- Obtaining the Company’s first investment grade credit rating

- Utilizing earnings growth and free cash flow to rapidly improve the Company’s Debt/EBITDAre ratio from 10.2x (2020) to 7.8x (2023)

At the beginning of 2022, Whitestone also was saddled with an investment in Pillarstone Capital REIT Operating Partnership, an entity controlled by our former CEO that was riddled with conflict and dilutive to Whitestone shareholders. The new management team immediately moved to exit this troubled investment. Our multiple litigation wins include a favorable court ruling, which has resulted in a multi-million dollar damage award. We are currently in the process of collecting on that award.

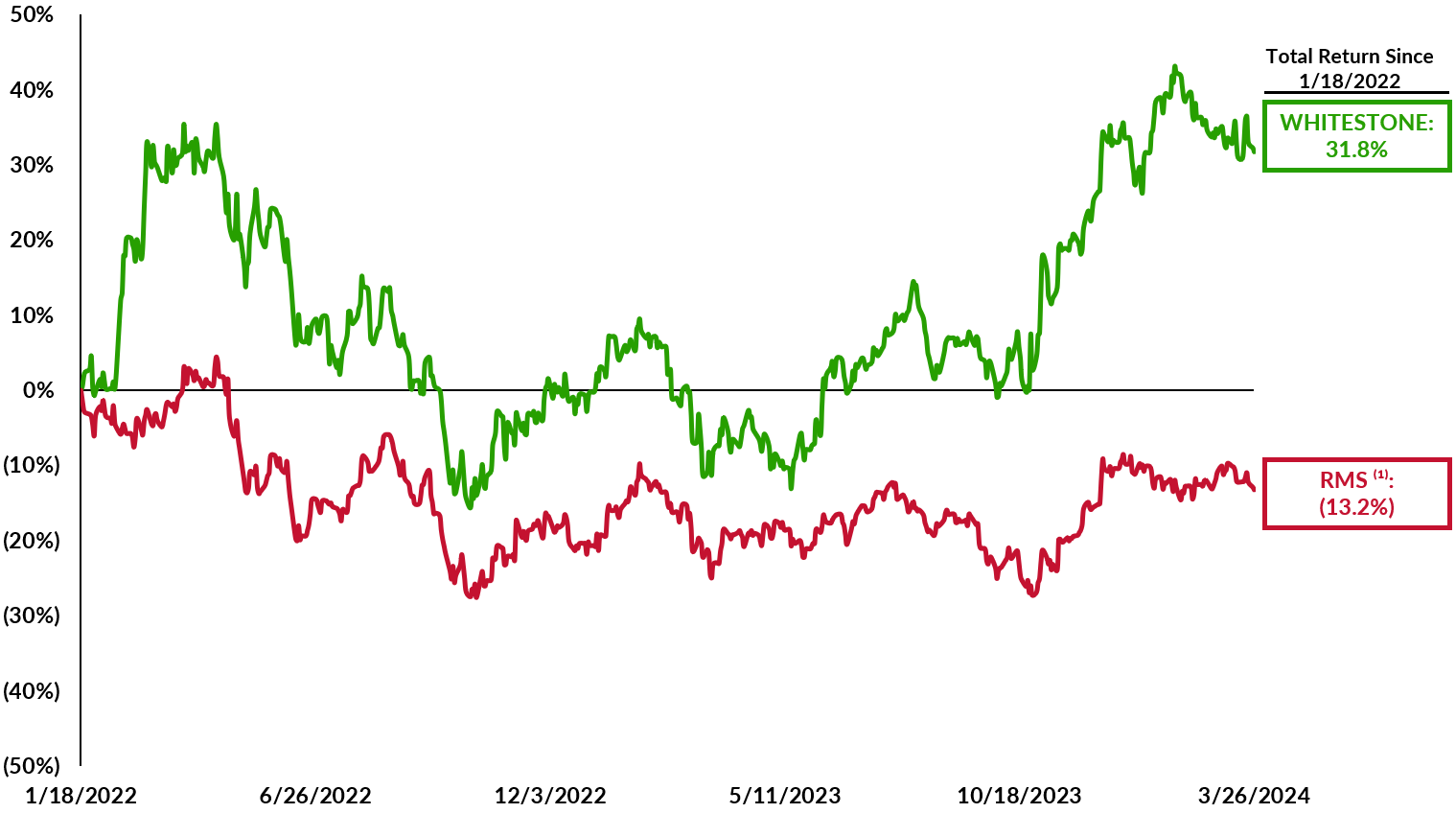

SINCE OUR CEO CHANGE, WHITESTONE REIT HAS A TRACK RECORD OF SUPERIOR PERFORMANCE

Total Shareholder Returns v MSCI US REIT Index

Source: FactSet as of March 26, 2024.

Note: Total returns include the reinvestment of dividends on the ex-date.

(1) RMS represents the total return performance of the MSCI US REIT Index.

Total Shareholder Returns v Peers

Source: FactSet as of March 26, 2024.

Note: Total returns include the reinvestment of dividends on the ex-date.

(1) PECO began trading on the NASDAQ on July 15, 2021.

(2) RMS represents the total return performance of the MSCI US REIT Index.

(3) IVT began trading on the NYSE on October 12, 2021.

OUR STRONG, THOUGHTFULLY REFRESHED BOARD HAS OVERSEEN A STRATEGY DRIVING SUSTAINABLE VALUE

The Whitestone Board of Trustees brings strong real estate, capital markets, legal, financial and investor relations experience. The majority of the Trustees’ real estate experience is specific to Whitestone’s markets, which is vital to understanding ongoing investments and Company operations. All of our board members have met with shareholders and are committed to translating shareholder feedback into shareholder value.

The board has undergone significant refreshment with 3 of 6 trustees added over the past 2 years. Each of our Board nominees are members added over the last 7 years. This refreshment has:

- Achieved a balance of deep institutional knowledge, diversity and fresh perspectives that complement our long term growth strategy

- Created the right mix of relevant expertise and experience to drive Whitestone forward

Whitestone’s independent board members also have a track record of taking action to protect shareholders, reflected by recent corporate governance and management changes and naming David Holeman as CEO in January 2022.

Most importantly, the Board is overseeing a strategy that is driving value and producing results.

MAKE NO MISTAKE, EREZ’S CAMPAIGN IS DETRIMENTAL TO ALL SHAREHOLDERS

As previously mentioned, Erez’s mission seems to be to establish Bruce Schanzer’s credibility in the REIT activism arena and use Whitestone REIT as proof-of-concept. To date, Erez has accumulated approximately 1% of our shares outstanding and is seeking to deploy its one tactic on all shareholders. Erez’s single purpose is to sell the Company – an ill-advised and potentially value destructive action against the current macro backdrop.

In short, Erez’s founder, Mr. Bruce Schanzer, only has one page in his playbook from his days at CEO of Cedar Realty Trust. Through numerous communications (including his initial letter to us), Erez offered no concrete, actionable, outside-in strategies to deliver value to Whitestone shareholders other than advocating for a sale or liquidation of the Company.

Mr. Schanzer has stated he has no intention of considering differences in current market conditions, interest rates, valuation levels, transaction activity and debt financing that are dramatically different versus when the Cedar transaction was launched in late 2021 and signed in early 2022.

The Whitestone Board reviews all avenues to drive shareholder value. Erez seems detached from the reality of 2024: with interest rates at multi-year highs, a slow transaction market and a wide bid-ask spread between buyers and sellers. To set the record straight, we carefully evaluate and consider all offers for our Company and are committed to our fiduciary duties to maximize shareholder value. But we do question why Erez is so fixated on effecting an immediate sale or monetization of assets under sub-optimal market conditions and chooses to completely ignore the embedded upside within our portfolio.

THE CHOICE IS CLEAR, WHITESTONE REIT HAS THE RIGHT TEAM AND PLAN TO DRIVE SHAREHOLDER VALUE

Whitestone has led the MSCI US REIT index with over 30% total shareholder return since the management change in January 2022. This performance has been driven by outstanding operational results:

- Occupancy up 290 basis points over two years to a record 94.2%

- Straight line leasing spreads in excess of 17% for seven consecutive quarters

- Strong Same Store Net Operating Income

Whitestone has a laser-focused strategy that is clearly working. Your vote is critical to ensure the Company’s momentum is not interrupted and shareholder value destroyed.

Vote on the WHITE proxy card for Whitestone’s proposals:

- Elect all 6 of our trustee nominees

- Approve Say on Pay

- Ratify Auditors

Sincerely,

The Whitestone Board of Trustees:

David T. Taylor

Nandita V. Berry

Julia B. Buthman

Amy S. Feng

David K. Holeman

Jeffrey A. Jones

About Whitestone REIT

Whitestone REIT (NYSE: WSR) is a community-centered real estate investment trust (REIT) that acquires, owns, operates, and develops open-air, retail centers located in some of the fastest growing markets in the country: Phoenix, Austin, Dallas-Fort Worth, Houston and San Antonio.

Our centers are convenience focused: merchandised with a mix of service-oriented tenants providing food (restaurants and grocers), self-care (health and fitness), services (financial and logistics), education and entertainment to the surrounding communities. The Company believes its strong community connections and deep tenant relationships are key to the success of its current centers and its acquisition strategy. For additional information, please visit www.whitestonereit.com.

Important Additional Information and Where to Find It

Whitestone REIT has filed a definitive proxy statement on Schedule 14A (the “2024 Proxy Statement”) and a WHITE proxy card with the U.S. Securities and Exchange Commission (the “SEC”) in connection with the solicitation of proxies for its 2024 Annual Meeting of Shareholders (the “2024 Annual Meeting”). SHAREHOLDERS ARE STRONGLY ENCOURAGED TO READ THE 2024 PROXY STATEMENT (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO), THE WHITE PROXY CARD, AND ANY OTHER DOCUMENTS FILED WITH THE SEC WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Shareholders may obtain a free copy of the 2024 Proxy Statement, any amendments or supplements to the 2024 Proxy Statement and other documents that the Company files with the SEC from the SEC’s website at www.sec.gov or the Company’s website at https://ir.whitestonereit.com/corporate-profile/default.aspx as soon as reasonably practicable after such materials are electronically filed with, or furnished to, the SEC.

Certain Information Regarding Participants in Solicitation

Whitestone REIT, its trustees and certain of its executive officers may be deemed to be participants in the solicitation of proxies from Company shareholders in connection with the matters to be considered at the 2024 Annual Meeting Information regarding the direct and indirect interests, by security holdings or otherwise, of the persons who may, under the rules of the SEC, be considered participants in the solicitation of shareholders in connection with the 2024 Annual Meeting is included in the 2024 Proxy Statement of the, which was filed with the SEC on April 4, 2024. To the extent securities holdings by the Company’s trustees and executive officers as reported in the 2024 Proxy Statement have changed, such changes have been or will be reflected on Statements of Change in Ownership on Forms 3, 4 or 5 filed with the SEC, which can also be found through the Company’s website (https://ir.whitestonereit.com/corporate-profile/default.aspx) in the section “Investor Relations” or through the SEC’s website. These documents are available free of charge as described above.

Forward-Looking Statements

This Report contains forward-looking statements within the meaning of the federal securities laws, including discussion and analysis of our financial condition and results of operations, statements related to our expectations regarding the performance of our business, and other matters. These forward-looking statements are not historical facts but are the intent, belief or current expectations of our management based on its knowledge and understanding of our business and industry. Forward-looking statements are typically identified by the use of terms such as “may,” “will,” “should,” “potential,” “predicts,” “anticipates,” “expects,” “intends,” “plans,” “believes,” “seeks,” “estimates” or the negative of such terms and variations of these words and similar expressions, although not all forward-looking statements include these words. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control, are difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements.

Factors that could cause actual results to differ materially from any forward-looking statements made in this Report include: the imposition of federal income taxes if we fail to qualify as a real estate investment trust (“REIT”) in any taxable year or forego an opportunity to ensure REIT status; uncertainties related to the national economy, the real estate industry in general and in our specific markets; legislative or regulatory changes, including changes to laws governing REITs; adverse economic or real estate developments or conditions in Texas or Arizona, Houston and Phoenix in particular, including the potential impact of public health emergencies, such as COVID-19, on our tenants’ ability to pay their rent, which could result in bad debt allowances or straight-line rent reserve adjustments; increases in interest rates, including as a result of inflation operating costs or general and administrative expenses; our current geographic concentration in the Houston and Phoenix metropolitan area makes us susceptible to local economic downturns and natural disasters, such as floods and hurricanes, which may increase as a result of climate change, increasing focus by stakeholders on environmental, social, and governance matters, financial institution disruption; availability and terms of capital and financing, both to fund our operations and to refinance our indebtedness as it matures; decreases in rental rates or increases in vacancy rates; harm to our reputation, ability to do business and results of operations as a result of improper conduct by our employees, agents or business partners; litigation risks; lease-up risks, including leasing risks arising from exclusivity and consent provisions in leases with significant tenants; our inability to renew tenant leases or obtain new tenant leases upon the expiration of existing leases; risks related to generative artificial intelligence tools and language models, along with the potential interpretations and conclusions they might make regarding our business and prospects, particularly concerning the spread of misinformation; our inability to generate sufficient cash flows due to market conditions, competition, uninsured losses, changes in tax or other applicable laws; geopolitical conflicts, such as the ongoing conflict between Russia and Ukraine, the conflict in the Gaza Strip and unrest in the Middle East; the need to fund tenant improvements or other capital expenditures out of operating cash flow; the extent to which our estimates regarding Pillarstone REIT Operating Partnership LP's financial condition and results of operations differ from actual results; and the risk that we are unable to raise capital for working capital, acquisitions or other uses on attractive terms or at all and other factors detailed in the Company's most recent Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and other documents the Company files with the Securities and Exchange Commission from time to time.

Non-GAAP Financial Measures

This release contains supplemental financial measures that are not calculated pursuant to U.S. generally accepted accounting principles (“GAAP”) including EBITDAre, FFO, NOI and net debt. Following are explanations and reconciliations of these metrics to their most comparable GAAP metric.

EBITDAre: The National Association of Real Estate Investment Trusts (“NAREIT”) defines EBITDAre as net income computed in accordance with GAAP, plus interest expense, income tax expense, depreciation and amortization and impairment write-downs of depreciable property and of investments in unconsolidated affiliates caused by a decrease in value of depreciable property in the affiliate, plus or minus losses and gains on the disposition of depreciable property, including losses/gains on change in control and adjustments to reflect the entity’s share of EBITDAre of the unconsolidated affiliates and consolidated affiliates with non-controlling interests. The Company calculates EBITDAre in a manner consistent with the NAREIT definition. Management believes that EBITDAre represents a supplemental non-GAAP performance measure that provides investors with a relevant basis for comparing REITs. There can be no assurance the EBITDAre as presented by the Company is comparable to similarly titled measures of other REITs. EBITDAre should not be considered as an alternative to net income or other measurements under GAAP as indicators of operating performance or to cash flows from operating, investing or financing activities as measures of liquidity. EBITDAre does not reflect working capital changes, cash expenditures for capital improvements or principal payments on indebtedness.

FFO: Funds From Operations: The National Association of Real Estate Investment Trusts (“NAREIT”) defines FFO as net income (loss) (calculated in accordance with GAAP), excluding depreciation and amortization related to real estate, gains or losses from the sale of certain real estate assets, gains and losses from change in control, and impairment write-downs of certain real estate assets and investments in entities when the impairment is directly attributable to decreases in the value of depreciable real estate held by the entity. We calculate FFO in a manner consistent with the NAREIT definition and also include adjustments for our unconsolidated real estate partnership.

Core Funds from Operations (“Core FFO”) is a non-GAAP measure. From time to time, we report or provide guidance with respect to “Core FFO” which removes the impact of certain non-recurring and non-operating transactions or other items we do not consider to be representative of our core operating results including, without limitation, default interest on debt of real estate partnership, extinguishment of debt cost, gains or losses associated with litigation involving the Company that is not in the normal course of business, and proxy contest professional fees.

Management uses FFO and Core FFO as a supplemental measure to conduct and evaluate our business because there are certain limitations associated with using GAAP net income (loss) alone as the primary measure of our operating performance. Historical cost accounting for real estate assets in accordance with GAAP implicitly assumes that the value of real estate assets diminishes predictably over time. Because real estate values instead have historically risen or fallen with market conditions, management believes that the presentation of operating results for real estate companies that use historical cost accounting is insufficient by itself. In addition, securities analysts, investors and other interested parties use FFO and Core FFO as the primary metric for comparing the relative performance of equity REITs. FFO and Core FFO should not be considered as an alternative to net income or other measurements under GAAP, as an indicator of our operating performance or to cash flows from operating, investing or financing activities as a measure of liquidity. FFO and Core FFO do not reflect working capital changes, cash expenditures for capital improvements or principal payments on indebtedness. Although our calculation of FFO is consistent with that of NAREIT, there can be no assurance that FFO and Core FFO presented by us is comparable to similarly titled measures of other REITs.

NOI: Net Operating Income: Management believes that NOI is a useful measure of our property operating performance. We define NOI as operating revenues (rental and other revenues) less property and related expenses (property operation and maintenance and real estate taxes). Other REITs may use different methodologies for calculating NOI and, accordingly, our NOI may not be comparable to other REITs. Because NOI excludes general and administrative expenses, depreciation and amortization, equity or deficit in earnings of real estate partnership, interest expense, interest, dividend and other investment income, provision for income taxes, gain on sale of property from discontinued operations, management fee (net of related expenses) and gain or loss on sale or disposition of assets, and includes NOI of real estate partnership (pro rata) and net income attributable to noncontrolling interest, it provides a performance measure that, when compared year-over-year, reflects the revenues and expenses directly associated with owning and operating commercial real estate properties and the impact to operations from trends in occupancy rates, rental rates and operating costs, providing perspective not immediately apparent from net income. We use NOI to evaluate our operating performance since NOI allows us to evaluate the impact that factors such as occupancy levels, lease structure, lease rates and tenant base have on our results, margins and returns. In addition, management believes that NOI provides useful information to the investment community about our property and operating performance when compared to other REITs since NOI is generally recognized as a standard measure of property performance in the real estate industry. However, NOI should not be viewed as a measure of our overall financial performance since it does not reflect the level of capital expenditure and leasing costs necessary to maintain the operating performance of our properties, including general and administrative expenses, depreciation and amortization, equity or deficit in earnings of real estate partnership, interest expense, interest, dividend and other investment income, provision for income taxes, gain on sale of property from discontinued operations, management fee (net of related expenses) and gain or loss on sale or disposition of assets.

Same Store NOI: Management believes that Same Store NOI is a useful measure of the Company’s property operating performance because it includes only the properties that have been owned for the entire period being compared, and it is frequently used by the investment community. Same Store NOI assists in eliminating differences in NOI due to the acquisition or disposition of properties during the period being presented, providing a more consistent measure of the Company’s performance. The Company defines Same Store NOI as operating revenues (rental and other revenues, excluding straight-line rent adjustments, amortization of above/below market rents, and lease termination fees) less property and related expenses (property operation and maintenance and real estate taxes), Non-Same Store NOI, and NOI of our investment in Pillarstone OP (pro rata). We define “Non-Same Stores” as properties that have been acquired since the beginning of the period being compared and properties that have been sold, but not classified as discontinued operations. Other REITs may use different methodologies for calculating Same Store NOI, and accordingly, the Company's Same Store NOI may not be comparable to that of other REITs.

Net debt: We present net debt, which we define as total debt net of insurance financing less cash plus our proportional share of net debt of real estate partnership, and net debt to pro forma EBITDAre, which we define as net debt divided by EBITDAre because we believe they are helpful as supplemental measures in assessing our ability to service our financing obligations and in evaluating balance sheet leverage against that of other REITs. However, net debt and net debt to pro forma EBITDAre should not be viewed as a stand-alone measure of our overall liquidity and leverage. In addition, other REITs may use different methodologies for calculating net debt and net debt to pro forma EBITDAre, and accordingly our net debt and net debt to pro forma EBITDAre may not be comparable to that of other REITs.

| Whitestone REIT and Subsidiaries | ||||||

| RECONCILIATION OF NON-GAAP MEASURES | ||||||

| Initial Full Year Guidance for 2024 | ||||||

| (in thousands, except per share and per unit data) | ||||||

| Projected Range Full Year 2024 | ||||||

| Low | High | |||||

| FFO (NAREIT) and Core FFO per diluted share and OP unit | ||||||

| Net income attributable to Whitestone REIT | $ | 16,600 | $ | 19,600 | ||

| Adjustments to reconcile to FFO (NAREIT) | ||||||

| Depreciation and amortization of real estate assets | 34,252 | 34,252 | ||||

| Depreciation and amortization of real estate assets of real estate partnership (pro rata) | 133 | 133 | ||||

| FFO (NAREIT) | $ | 50,985 | $ | 53,985 | ||

| Adjustments to reconcile to Core FFO | ||||||

| Adjustments | — | — | ||||

| Core FFO | $ | 50,985 | $ | 53,985 | ||

| Dilutive shares | 51,262 | 51,262 | ||||

| OP Units | 695 | 695 | ||||

| Dilutive share and OP Units | 51,957 | 51,957 | ||||

| Net income attributable to Whitestone REIT per diluted share | $ | 0.32 | $ | 0.38 | ||

| FFO (NAREIT) per diluted share and OP Unit | $ | 0.98 | $ | 1.04 | ||

| Net income attributable to Whitestone REIT per diluted share | $ | 0.32 | $ | 0.38 | ||

| Core FFO per diluted share and OP Unit | $ | 0.98 | $ | 1.04 | ||

| Whitestone REIT and Subsidiaries | ||||||||

| RECONCILIATION OF NON-GAAP MEASURES | ||||||||

| (continued) | ||||||||

| (in thousands) | ||||||||

| Year Ended December 31, | ||||||||

| 2023 | 2022 | |||||||

| PROPERTY NET OPERATING INCOME | ||||||||

| Net income attributable to Whitestone REIT | $ | 19,180 | $ | 35,270 | ||||

| General and administrative expenses | 20,653 | 18,066 | ||||||

| Depreciation and amortization | 32,966 | 31,707 | ||||||

| (Equity) deficit in earnings of real estate partnership (1) | 3,155 | (239 | ) | |||||

| Interest expense | 32,866 | 27,193 | ||||||

| Interest, dividend and other investment income | (51 | ) | (65 | ) | ||||

| Provision for income taxes | 450 | 422 | ||||||

| (Gain) loss on sale of properties, net | (9,006 | ) | (16,950 | ) | ||||

| Management fee, net of related expenses | 16 | 112 | ||||||

| Loss on disposal of assets, net | 522 | 192 | ||||||

| NOI of real estate partnership (pro rata)(1) | 2,553 | 3,023 | ||||||

| Net income attributable to noncontrolling interests | 270 | 530 | ||||||

| NOI | $ | 103,574 | $ | 99,261 | ||||

| Non-Same Store NOI (2) | (4,370 | ) | (3,322 | ) | ||||

| NOI of real estate partnership (pro rata) (1) | (2,553 | ) | (3,023 | ) | ||||

| NOI less Non-Same Store NOI and NOI of real estate partnership (pro rata) | 96,651 | 92,916 | ||||||

| Same Store straight-line rent adjustments | (2,284 | ) | (1,466 | ) | ||||

| Same Store amortization of above/below market rents | (862 | ) | (933 | ) | ||||

| Same Store lease termination fees | (698 | ) | (135 | ) | ||||

| Same Store NOI (3) | $ | 92,807 | $ | 90,382 | ||||

| Whitestone REIT and Subsidiaries | |||||||

| RECONCILIATION OF NON-GAAP MEASURES | |||||||

| (continued) | |||||||

| (in thousands) | |||||||

| Year Ended December 31, | |||||||

| 2023 | 2020 | ||||||

| EARNINGS BEFORE INTEREST, TAX, DEPRECIATION AND AMORTIZATION FOR REAL ESTATE (EBITDAre) | |||||||

| Net income attributable to Whitestone REIT | $ | 19,180 | $ | 6,034 | |||

| Depreciation and amortization | 32,966 | 28,303 | |||||

| Interest expense | 32,866 | 25,770 | |||||

| Provision for income taxes | 450 | 379 | |||||

| Net income attributable to noncontrolling interests | 270 | 117 | |||||

| (Equity) deficit in earnings of real estate partnership (1) | 3,155 | (921 | ) | ||||

| EBITDAre adjustments for real estate partnership (1) | 617 | 3,484 | |||||

| Loss (gain) loss on sale or disposal of assets, net | (8,484 | ) | 364 | ||||

| Gain on loan forgiveness | — | (1,734 | ) | ||||

| EBITDAre | 81,020 | 61,796 | |||||

| Year Ended December 31, | |||||||

| Debt/EBITDAre Ratio | 2023 | 2020 | |||||

| Outstanding debt | $ | 640,549 | $ | 645,163 | |||

| Less: Cash | (4,572 | ) | (25,777 | ) | |||

| Deposit due to real estate partnership debt default | (13,633 | ) | - | ||||

| Add: Proportional share of net debt of unconsolidated real estate partnership (1) | 8,685 | 8,912 | |||||

| Total Net Debt | $ | 631,029 | $ | 628,298 | |||

| EBITDAre | $ | 81,020 | $ | 61,796 | |||

| Ratio of debt to pro forma EBITDAre | 7.8 | 10.2 | |||||

(1) We rely on reporting provided to us by our third-party partners for financial information regarding the Company's investment in Pillarstone OP. Because Pillarstone OP financial statements as of December 31, 2023 and 2022 have not been made available to us, we have estimated proportional share of net deb based on the information available to us at the time.

Investor and Media Contact:

David Mordy

Director of Investor Relations

Whitestone REIT

(713) 435-2219

ir@whitestonereit.com

Photos accompanying this announcement are available at:

https://www.globenewswire.com/NewsRoom/AttachmentNg/be5fbb20-d9af-476a-86cf-22a945ed1e44

https://www.globenewswire.com/NewsRoom/AttachmentNg/68364c3c-4fc0-4b3e-a041-b69e81ffbac8

https://www.globenewswire.com/NewsRoom/AttachmentNg/c90fbed0-f978-47e9-9de2-feb6358e28c3