Dublin, May 03, 2024 (GLOBE NEWSWIRE) -- The "Open Banking Global Market Opportunities and Strategies to 2033" report has been added to ResearchAndMarkets.com's offering.

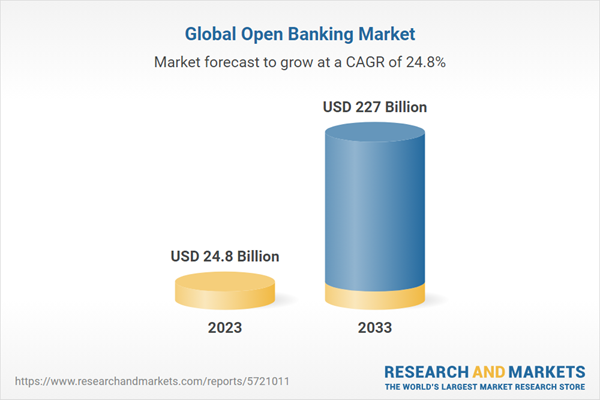

In an enlightening analysis of the open banking sector, recent findings highlight a substantial growth trajectory with a take-off value nearing $24.78 billion as of 2023. This propulsion is testament to the sector's robust compound annual growth rate of 33.3% since 2018, showcasing the dynamic nature of open banking. The forecast period indicates a continuance of this trend, with expectations set for the market to rise to an estimable $77.45 billion by 2028, followed by further acceleration to reach approximately $227.01 billion by 2033.

The historic period's growth is attributed to an upsurge in online platform usage, burgeoning demands for real-time fund transfers, a growth spurt in the younger demographic, and a pivot towards financial technology for payment systems. However, this forward march was not without its hindrances, faced notably in the form of stringent regulations. Looking ahead, digital banking platforms, smartphone proliferation, a flourishing e-commerce segment, and reduced transaction costs are set to steer the open banking juggernaut. Nevertheless, potential roadblocks such as security concerns, reputational hazards, and dependencies may present challenges in the coming era.

Sector Dissections

The market segments into various services, with transactional services taking the lead by commanding 68.5% of the market share in 2023. Yet, communicative and informative services are predicted to witness the fastest growth rate going forward. Similarly, when delineated by financial services, the bank and capital markets dominate the space, although the payments segment is poised for expedited growth. Deployment types also see varying degrees of traction, with on-premises solutions historically leading in market share. As the landscape evolves, cloud solutions anticipate the quickest expansion. Distribution channels, meanwhile, are mainly bank channels and app markets, with the latter expected to accelerate at the highest rate in the future.

Regional Insights

Geographically, Western Europe held the lion's share in 2023, closely tailed by North America and the Asia-Pacific regions. Prospectively, Africa and the Asia-Pacific regions are earmarked for the swiftest growth, while North America and Eastern Europe follow suit with impressive CAGRs. This sector is characterized by its competitive diversity, with the ten leading entities together not surpassing one-quarter of the market share in 2022, signifying a market rich with opportunity.

Strategies and Recommendations

Forecasts advise that the most lucrative opportunities will materialize in transactional services, bank and capital markets, on-premises deployment, and amongst app market distribution channels. The United States, in particular, is anticipated to benefit significantly from these trends. Strategically, stakeholders are encouraged to hone in on payment innovations, leverage variable recurring payment technologies, and invest in advanced digital platforms to stay ahead. Partnerships and robust investments emerge as key tactics for cementing market stature.

To seize these opportunities in the dynamic sphere of open banking, industry participants are advised to innovate payment solutions, seek strategic alliances, and invigorate their offerings through communicative and informative services. It's crucial to maintain a focus on both burgeoning markets and established economies and to remain competitive through strategic pricing and a robust narrative. This comprehensive market analysis unveils the transformational growth prospective of open banking, alongside actionable insights for industry leaders to sustain and bolster their market presence into the future.

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 257 |

| Forecast Period | 2023 - 2033 |

| Estimated Market Value (USD) in 2023 | $24.8 Billion |

| Forecasted Market Value (USD) by 2033 | $227 Billion |

| Compound Annual Growth Rate | 24.8% |

| Regions Covered | Global |

A selection of companies mentioned in this report includes, but is not limited to:

- Banco Bilbao Vizcaya Argentaria, S.A.

- Banco Santander S.A.

- HSBC Holdings Plc

- Crédit Agricole S.A.

- Citigroup Inc.

- NatWest Group Plc

- Capital One Financial Corporation

- DBS Group Holdings Ltd

- Lloyds Banking Group

- Barclays PLC

- Axis Bank

- Bank Of Baroda

- BNL

- FamPay

- Federal Bank

- Finin

- HDFC Bank

- Airwallex

- American Express

- ANZ (Australia and New Zealand Banking Group Limited)

- China Construction Bank (CCB)

- DBS Bank

- ICBC Bank

- WeBank

- ChiantiBanca

- Ant Financial

- Commonwealth Bank of Australia (CBA)

- Westpac Banking Corporation

- National Australia Bank (NAB)

- Macquarie Bank

- Allied Irish Bank

- Bank of Ireland

- Barclays

- Danske

- HSBC

- Nationwide

- RBS Group

- ING

- Caixa Geral De Depositos

- La Banque Postale

- Cofidis

- Hello bank!

- bunq

- BNP Paribas

- Citi

- OTP Bank

- Ikano Bank

- Oneggo Bank

- Tinkoff Bank

- Wise

- Raiffeisen Bank

- Microsoft Corporation

- IBM

- Amazon Web Services

- Hewlett Packard Enterprise

- Intel

- Oracle Corporation

- JPMorgan Chase & Co

- BBVA SA

- Credit Agricole

- Deposit Solutions

- Finestra

- Jack Henry & Associates Inc

- Nordigen Solutions

- AlphaPoint

- Axway

- Santander

- TecBan

- Spire Technologies

- Tarabut Gateway

- Dapi

- Lean Technologies

- Standard Bank Group

- FirstRand Bank (First National Bank)

- Absa Group Limited

- Nedbank Group

- Capitec Bank

For more information about this report visit https://www.researchandmarkets.com/r/sc6s4x

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment